What next for price of gold?

Is now the time to be investing in gold? With inflation on the rise and political risk high opinion is divided. Here, we explain the basics on gold pricing and ask fund managers who specialise in the commodity to share their views.

Gold, one of the oldest known metals, was revered by all the great ancient civilisations and the first gold coins were minted as far back as 550BC.

Relatively scarce and notoriously difficult to produce, gold has been widely used both as a store of value and as an adornment throughout history. Today, however, it often divides opinion – at least among investors.

One reason for this is that it is difficult to value.

Compared to valuing a company or a bond, with gold there is relatively little to work with. Analysing the “fundamentals” of it is tough, when some investors argue there are none: it has no true intrinsic value, no cashflow, no earnings, no coupon payments and no yield, say gold sceptics.

But gold is undeniably affected by global economic factors. Although the prospects of rising interest rates is normally bad for gold, as it is a non-yielding asset, with inflation picking up and the focus on political risk increasing, gold bugs (investors who are bullish on gold) are back.

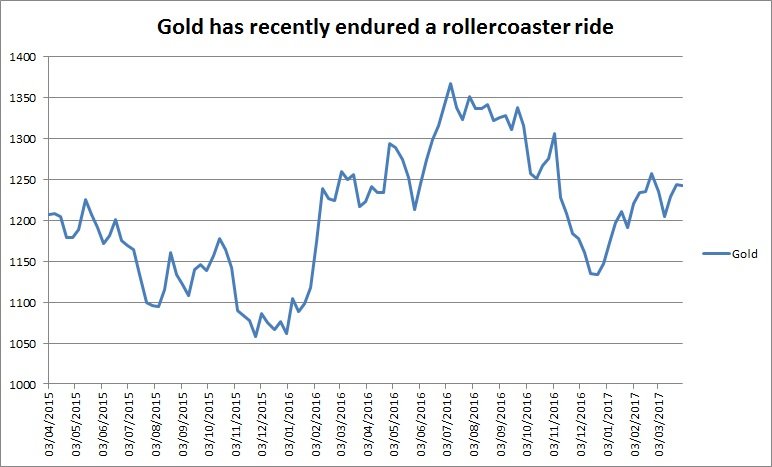

What’s happened to the gold price recently?

It had been a pleasant 2016 for gold investors until August. After a steep climb from around $1050 to $1360, the price of the precious metal started to fall and by December was back at around $1130.

For gold bugs this was a chance to top up their holdings. Since then gold has been on the rise once again and at the time of writing is back at $1259 (source: Bloomberg, 27 March 2017).

So, what next for this most divisive of investments? We spoke to some Schroders fund managers to find out more and found that instead of just investing in gold itself, equities from gold mining companies are also finding favour.

James Luke, fund manager (commodities) at Schroders, said: “The primary reason for investing in commodities, and especially gold and silver, should always be as an inflation hedge. Given the printing of money by the world’s central banks through quantitative easing, there is every reason to argue that higher inflation is coming in the future.

“Gold and silver investments in particular remain very under-owned. Some investors fear the prospect of an increasing base interest rate in the US is reason alone to avoid these types of investments.

"However, although past performance is not a reliable indicator of future results, the gold price has tended to rise from the beginning to the end of Federal Reserve (Fed) hiking cycles. In the last four instances when the Fed embarked on a hiking cycle, in three of the four instances gold saw +10% to +20% returns from beginning to end.”

“The environment for gold investments remains positive. In the background, global record debt burdens have not magically vanished. These make global growth highly sensitive to any real increase in interest rates and the cost of servicing these debts.

"This is a key reason to expect that central banks will be highly weary of raising interest rates too quickly and that real interest rates (a key driver of gold prices) should continue to remain very low and have the possibility of being negative as inflation accelerates.

“Given investors’ high exposure to the traditional asset classes, there is an urgent need to find uncorrelated and attractive alternative investments. Liquid and tangible portfolio diversification options are limited, making gold and gold related investments unique and of use to many investors.

“Although there will be some good tactical opportunities to invest in gold in the coming years, we think the best gold-related opportunities are in gold mining stocks. Valuations are very attractive and miners have also become more disciplined than in the past, with better management focusing on free cashflow and controlling costs.”

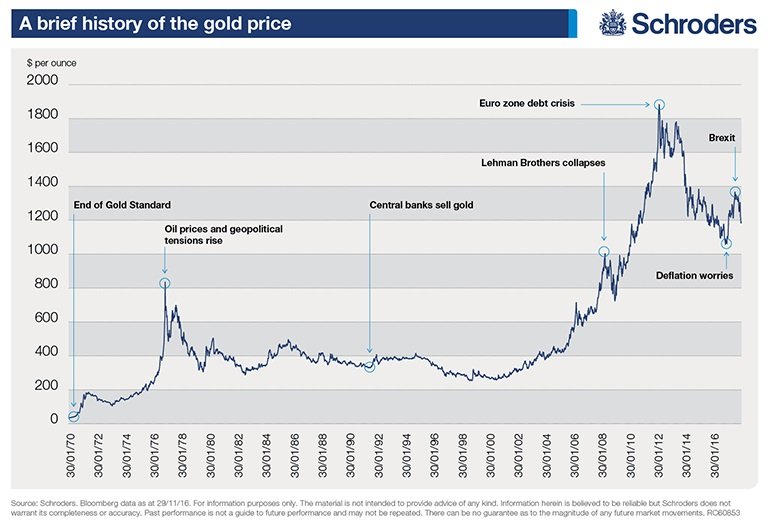

– We explain the history of the gold price (below) – click here

Marcus Brookes, head of multi-manager at Schroders, was vocal on gold when he expected inflation to gather pace. He said: "We began to get more positive on gold-related equities in the third quarter to 2015, driven by the significant bear market that many of these companies had experienced from 2010 and what looked like an attractive entry point at the time. As a result we added to our position in a gold equity fund.

“We then added further to the position over the summer. This is because we believed that many investors had taken a significantly skewed position for a deflationary backdrop (where prices in an economy fall) as the “secular stagnation” argument, that we were entering a period of negligible or no economic growth, was so widespread.

"This meant they moved away from the more 'value' (undervalued and economically sensitive) areas of markets such as gold equity. In our eyes, inflation expectations were too low and any signs of inflation were due to benefit the more value-orientated areas of markets.

“While there was something of a correction in gold in the latter part of this year, our view of it as a valuable asset to hold in an inflationary backdrop remained.

"Inflation expectations are now relatively well-established and whilst there are various factors to unravel over the course of 2017 (how the US dollar fares and the extent of Donald Trump's fiscal measures to name a couple), we expect it to remain an important part of our portfolios in what could prove to be a tricky year."

Important Information: The views and opinions contained herein are those of Philip Haddon, Head of Investment Communication and others mentioned in this article, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.