Investor relief at Dutch election: what next for stock markets?

European stock markets have expressed relief at the Dutch election result.

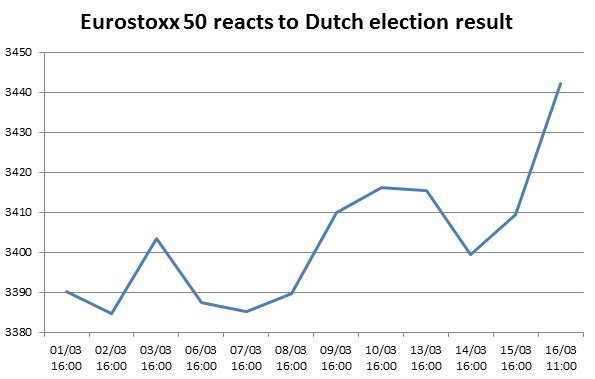

Traders had been anxious and share prices put under pressure in the run up to polling day yesterday. But centre-right Prime Minister Mark Rutte saw off a challenge from the Party for Freedom (PVV), led by anti-immigration nationalist Geert Wilders.

The election had been closely watched, offering a litmus test for populism in Europe.

By midday, the Eurostoxx 50 was around 2% higher than its level of late yesterday afternoon, when speculation began that Rutte’s People’s Party for Freedom and Democracy (VVD) would win.

The FTSE 100 also rose sharply reaching 7,410 by midday, a fresh all-time high.

Below, two experts explain the wider context and look at what next for markets.

Sam Twidale, a European fund manager, explains why he believes European shares are at a 40% discount. This is based on a cyclically-adjusted price-earning measure, known as CAPE. Prices are compared with earnings but smoothed over a decade to iron out anomalies.

Economist Azad Zangana looks ahead to what it means for the French elections.

Source: Schroders. Bloomberg data as at 16/03/2017. For information purposes only. The material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Past performance is not a guide to future performance and may not be repeated. There can be no guarantee as to the magnitude of any future market movements.

Sam Twidale, European equities fund manager at Schroders, said:

“The strong support for the current VVD government should be taken as a positive outcome for European markets, with the country turning against the more populist measures proposed by the PVV.

“This included the risk of a potential exit from the European Union (EU), euro and greater restrictions on immigration, all of which could have resulted in a significant increase in risk aversion across European equity markets.

“Although the market had been relaxed about the outcome of the Dutch election and the risk of the PVV gaining power, ongoing political uncertainty is a key risk we've been highlighting for Europe this year.

“Investors are concerned about upcoming elections, in particular for the largest eurozone economies France and Germany which go to the polls in April/May and September.

“After the recent Brexit referendum in the UK, and the election of the Donald Trumpadministration in the US, the increasing risk of more populist governments gaining power in Europe has been a concern. The future of the EU and the stability of the euro were perceived to be potentially at stake. Although we see the risk of this as low, this uncertainty is likely to persist until the outcomes of these elections are known.”

Is the anti-EU agenda losing momentum?

“The market should take some confidence from the outcome of the Dutch election, as it's the first sign that mainland European economies may turn against the political parties with more anti-EU policies.

“Encouragingly the election saw very high turn-out at around 80%, with the majority vote clearly favouring mainstream political ideology. We will see how the other elections play out, but this result could reflect a stronger European economy i.e. greater optimism around personal circumstances. It also shows that centre-right political parties are willing to take a more robust approach towards immigration which appeases more of the popular vote.”

The outlook for European stock markets

“Putting aside the political uncertainty, we believe there are strong arguments to be positive on the outlook for European equities. The cyclical recovery across Europe is clearly gaining momentum, with lead indicators remaining positive and signs of improving confidence amongst companies and consumers.

“Eurozone unemployment continues to fall, supporting the recovery being seen by the domestic consumer, which in turn should lead to a greater willingness among companies to raise investment. This is being aided by easier borrowing conditions, helped by a European banking system which is finally becoming better capitalised and willing to extend credit.

“The threat of deflation also appears to have been avoided, with inflation now approaching the European Central Bank’s (ECB) 2% target.

“Along with a healthier domestic environment, the global backdrop may also support European exports. Growth in the US economy continues to look robust, helped by the more growth-friendly agenda promoted by the Trump administration.

“China has started the year with good economic momentum, with a combination of economic stimulus and environmental reform also contributing to the improving outlook for global commodity prices. There are also signs that other emerging market economies such as Brazil and Russia are slowly turning a corner after several challenging years.

“For European equities, this strengthening economic backdrop is finally translating into improving earnings prospects. In 2017 expectations are for high single digit earnings growth, with further improvement in 2018.

“This follows several years of moderate or no growth, which has been one of the key reasons for the material underperformance of European equities versus the US. European companies have been suffering from the recent deflationary environment, the limited recovery in domestic demand, and a general lack of pricing power.

“With earnings expectations now being revised up, there are signs these issues are now slowly reversing. The weaker euro is also helping corporates stay internationally competitive, especially versus the US dollar.”

Attractive stock market valuations in Europe

“Given the recovery potential for profit margins and earnings, valuations in Europe look compelling, especially when compared to other developed markets such as the US.

“The European market is trading on 15x price-to-earnings rate and a 3.5% dividend yield, with profit margins still depressed in many of the more cyclical sectors. On our favoured valuation metric – the cyclically-adjusted price-to-earnings ratio – the market offers 40% upside to its long-term average.”

Where to find value in Europe

“We have been looking to take advantage of the recent political uncertainty and resulting volatility, by adding to holdings where we believe the market has been too slow in reacting to the potential for earnings to recover.

“We have also been taking profits in some of the more defensive sectors, many of which have been driving the market higher this year. It is interesting to note that despite the improving economic indicators, value has actually been underperforming growth so far this year. This likely reflects the caution in the market and concerns around the upcoming elections.

“We have been finding attractive value opportunities in the materials sector, for example, with returns for some companies potentially set to improve substantially as demand recovers and overcapacity concerns are addressed.

“We also see opportunities in the consumer discretionary sector, where companies look poised to benefit from the domestic recovery underway in Europe, as well as the improvement being seen in emerging markets.”

Azad Zangana, senior European economist and strategist at Schroders, said:

“The PVV, which had campaigned on an anti-EU, anti-immigrant ticket, had led in opinion polls for the best part of the last year and only slipped behind the VVD in the last two weeks. However, the results show that while the PVV has gained seats, it has significantly underperformed expectations, and only barely finished as the second largest party.

“Rutte will now commence work to form a coalition government, but this will not be a straight-forward task. The Labour Party (PvdA), which was the previous junior coalition partner, has suffered a severe loss in seats, and so the VVD will have to form a broader coalition, perhaps with three or more parties. This is not unusual as the Dutch parliament has always been fragmented (with 13 parties winning seats this election).

“The election results will come as a relief for investors as it is the first notable underperformance of a populist party for some time. Given the Dutch constitution rules, Wilders probably would not have been able to gather enough support to actually hold a binding referendum to leave the EU, but notwithstanding this, the results are a positive surprise.”

Attention turns to France

“Investors will now turn their attention to the upcoming French presidential election, which arguably has a lower probability to disappoint, but could have bigger consequences for the EU should Marine Le Pen’s Front National win.

“Le Pen’s party has the most support of any single party, but the two stage electoral system in France means that top two candidates face each other in a run-off. This is when Le Pen is then expected to lose by quite some margin, regardless of whether she faces Francois Fillon or Emmanuel Macron (the next two leading candidates).

“Of course, opinion polls have been less reliable of late, and so investors are likely to remain cautious on Europe until political risk dies down.”

Important Information: The views and opinions contained herein are those of Azad Zangana and Sam Twidale, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.