How a World Cup run might turn £1 into £65,000 – the power of investment compounding

The World Cup is underway, so what better way to explain the miracle effects of compounding than via a football analogy?

We recently attended a meeting of company pension fund trustees where the chairman felt the need to clarify one observation with the line: “And, of course, because of compounding, a 10% increase in performance every year for five years means a total increase of not 50% but 61%.”

A valid point, no question – but an odd one to be making, we felt, to a group of professional custodians of a sizable amount of money.

Clearly the concept of compounding – the interest or growth earned not only on a loan or investment but also on the interest or growth previously earned – is not one everybody finds easy to grasp.

As we have illustrated in articles such as How realistic is a £1m pension pot? and indeed Compound interest is an extremely powerful thing, however, it is well worth making the effort to do so.

Given the 2018 World Cup is underway, it seemed appropriate this time to emphasise the power of compounding with a football example.

In our original post on The Value Perspective, we focused on the current holders Germany, who qualified with a 100% record of 10 group wins out of 10.

Unfortunately, they let us down at the first hurdle, losing to Mexico. Undaunted, we're ploughing ahead with our version of this analogy. Stick with us…

If Germany, who were second favourites, had won all their group and knock-out matches en route to lifting the trophy in Moscow on 15 July that would make 17 in a row this campaign.

- Odd investment lessons: when a Quarter Pounder is better value than a Third Pounder

- What Alan Shearer can teach us about inflation

- Shares vs property: which has performed best?

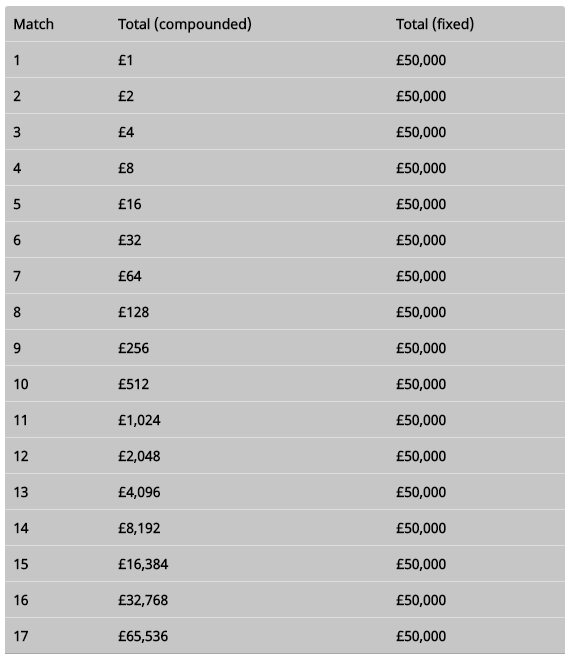

So, here’s the question – if, when Germany kicked off their first match on 4 September 2016, we had offered you £1 and doubled your total pot each time they won or a £50,000 lump sum upfront, which option would you have picked?

Most people would instinctively take the £50,000 but compound interest does not work on instinct but maths.

Doubling up from £1 after Match 1, it would only have been Match 8 before you had more than £100.

By the end of qualifying (Match 10), however, you would be up beyond £500 and after the World Cup final (Match 17), you would have more than £65,000.

Source: Schroders

Extend that idea over the course of a full Premier League season (whichever team you like – winning all 38 games really is in the realms of fantasy football) and how do you feel about a choice between the same £1 doubled each time or, say, a cool £10bn upfront?

If you picked the compounding pound this time, you were right to do so and have theoretically pocketed some £140bn – or £137,438,953,472 to be precise.

Almost enough to buy an entire back four for Manchester City, as the wags might say – but certainly clear evidence of why, away from the realms of theory, investors should give their assets as much time as possible to reap the very real benefits of the power of compounding.

- Kevin Murphy is an author on The Value Perspective, a blog about value investing. It is a long-term investing approach which focuses on exploiting swings in stock market sentiment, targeting companies which are valued at less than their true worth and waiting for a correction.

Important Information: The views and opinions contained herein are of those named in the article and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schrodersdoes not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.