The only question you need to ask yourself before investing in an ISA

Nick Kirrage, author on The Value Perspective blog, questions whether savers are really making the most of ISAs…

There is no doubt the individual savings account – or ‘ISA’ for short – has proved a huge hit among the UK’s savers and investors. In the 2015/16 tax year (the most recent for which official figures are available), more than 12 million people subscribed for one – hardly surprising given you do not have to pay any tax on the interest, income or capital gains generated by whatever assets you hold within these tiny tax havens.

Clearly, the larger your gains from the assets held within your ISA, the bigger the tax break you enjoy, which begs the question as to how you can look to increase your gains. Obviously you can invest as much as you are allowed – £20,000 per adult in the current tax year – but, after that, it comes down to what you invest in and for how long.

How long will you invest? That's the main question

In other words, you give yourself the best chance of boosting your gains and thus the associated tax breaks by investing in potentially higher-returning assets and over a longer timeframe. And while those may look like two choices, they both stem from considering the same question – for how long do you want to invest? For not only will your answer directly address the timeframe issue, it will also dictate what sort of asset you buy.

The prices of of most investments – shares, bonds, property and so forth – rarely stay still for long. Sometimes the prices will go up, sometimes down and this volatility, as it is known, tends to be more pronounced over shorter-time periods. The longer you invest for, however, the less worried you tend to be about volatility because, over longer time periods – 20 years, say – investments tend to move back to a long-term average.

-

Seatbelt laws created a new danger – and a lesson for investors

-

Cash vs shares: did Isa savers return to cash at the wrong time?

Data going back to 1964, for example, shows the average real return on stocks – that is, once the erosive effects of inflation are taken into consideration – is about 7% a year while the equivalent for cash is roughly 2% a year. Which begs one important question – why does HM Revenue & Customs data for the 2015/16 tax year reveal four times as many people subscribing to cash ISAs as to stock and shares ones?

Is there a benefit to a cash ISA?

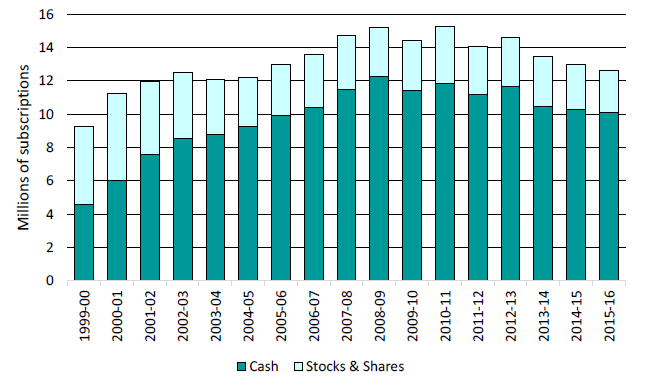

That 80% of all ISAs taken out in that tax year were of the cash variety (see the chart below) is a remarkable enough statistic on its own but it becomes even more so when you consider the derisory returns available on cash these days. Even the best-paying cash ISAs offer interest rates that are well below the current 2.3% rate of inflation. So just how many people will need the tax break that was presumably a big factor in their opening a cash ISA?

Source: HMRC

Clearly there will be plenty of people who, while understanding the attractions of an ISA, may be put off by the volatility associated with a stocks and shares one. Long-term stock market returns are, as we said, very attractive but, over the last decade, they have proved lower than average while price volatility has been unusually high.

As we also said, the longer you are prepared to hold your investment, the less of an issue this becomes. Nevertheless, for anyone who might want access to their investments over the next couple of years, this presents a significant risk – after all, nobody wants to be in a position where they are converting an equity investment back into cash just as stockmarkets are having a bad time.

The important difference with Junior ISAs

There is one group of ISA investors, for whom this is simply not an issue, however – and this is anyone who invests in a Junior ISA, which is the government’s way of encouraging people to save on behalf of children. Any fortunate beneficiary of a Junior ISA is unable to redeem their investments until they reach 18 or, in the case of the cash version, 16.

By definition – indeed, by regulation – a significant percentage of money flowing into Junior ISAs therefore has to adopt the sort of long-term time horizon that suits stockmarket investment so well. And yet, according to HM Revenue & Customs, two-thirds of all Junior ISAs subscribed for in 2015/16 were for cash. That makes absolutely no sense at all.

The question of how long you are willing to tie up your money is one of the most fundamental ones for any investor to address. Patterns of behaviour in the ISA market suggest, however, that players at every level – government and fund managers, advisers and investment platforms – need to work harder at engaging consumers and encouraging them to think hard about what they want to achieve from their ISA.

In an uncertain world, it is all too easy to become paralysed by fear and let short-term risk unduly affect long-term investment choices. The impact of this sort of thinking on the long-term financial security of UK consumers is, however, potentially disastrous.

- Nick Kirrage is an author on The Value Perspective, a blog about value investing. It is a long-term investing approach which focuses on exploiting swings in stock market sentiment, targeting companies which are valued at less than their true worth and waiting for a correction. Click here and enter your email to receive a weekly round-up of investment ideas.