Merrill Lynch and Citi bearish on gold prices and equities as US monetary policy normalisation approaches

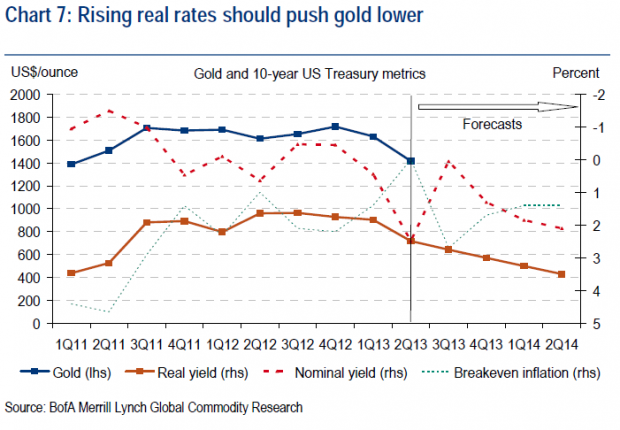

Gold will fall by 18 per cent to $1,291/oz in real terms in 2015, according to Bank of America Merrill Lynch. That's a downgrade to their outlook for gold prices, and is based on the view that while US fiscal squabbles will stabilise prices, the focus of investors will still be the "gradual normalisaiton of US monetary policy".

They've also knocked down their 2014 estimate by 17 per cent to $1,294/oz. As a result of that forecast, they've downgraded miner Petropavlovsk from Neutral to Buy "due to significant earnings downgrades and the risk now that they could breach covenants next year".

Bank of America maintains is Buy ratings for Randgold and African Barrick and says that "on a global basis, significant changes include Barrick and Kinross to Neutral, and Gold Fields to Underperform."

A separate note sees Citi group maintain a bearish view with regard to gold equities. Citi research estimates that 98 per cent of the gold industry is cash-burning, due to rising unit costs and the inability of producers to cut the cost of capital expenditure, exploration and other costs to keep up with the 12 per cent price decline.

Citi believe are best places to handle such challenges include Medusa, Yamana, Barrick, Buenaventura, Goldcorp, Oceana and Centamin.

Johann Steyn, Citi Research:

Global gold capex has increased 10-fold over the past 12-years, yet production has fallen 5% during this period. Unit costs have risen at a CAGR of 16% during this period. It is our view, that unit costs would have risen far quicker had it not been for the vast increase in capital expenditure.

It is because of this that we caution that a slow-down in capex will invariably result in a fall in production, which in turn will lead to a faster rise in unit costs. Whether or not capex is cut, we see both scenarios as bad for shareholders. There seems to be no easy way out.

The dramatic expansion of margins in the gold industry seen between 2009 and 2012 were a short lived period and that the current trend is a return to normality according to Citi.

It is expected that that the industry will react to the sharp drop in gold prices by through lowering capital budgets and expenditure on exploration and move to recapitalize balance sheets.