Italy a ticking timebomb for the fragile Eurozone

Improvements elsewhere in the periphery contrast with the worryingly slow progress in Rome

In parts of the Eurozone periphery, there are signs that struggling economies are finally turning a corner. Spain, for example, has returned to growth – albeit at the slow pace of 0.1 per cent in the third quarter – and Portuguese unemployment fell from 16.4 to 15.6 per cent over the same period. Moreover, Irish, Portuguese and Spanish 10-year bond yields have all fallen over the past month, reaching as low as 3.54 per cent in the case of Ireland.

But Italy, the Eurozone’s third largest economy, is languishing. Industrial output figures released yesterday showed a marked fall of 1 per cent in the third quarter, boding poorly for the country’s third quarter GDP results due on Thursday. If consensus forecasts of a 0.2 per cent contraction prove correct, Italy’s economy will have shrunk for nine consecutive quarters. And some fear that a combination of the country’s 127 per cent debt-to-GDP ratio, lagging productivity, and dysfunctional political system, could act as a drag on the Eurozone’s recovery, or – in the worst case scenario – tip the region back into crisis.

SLOW REFORM

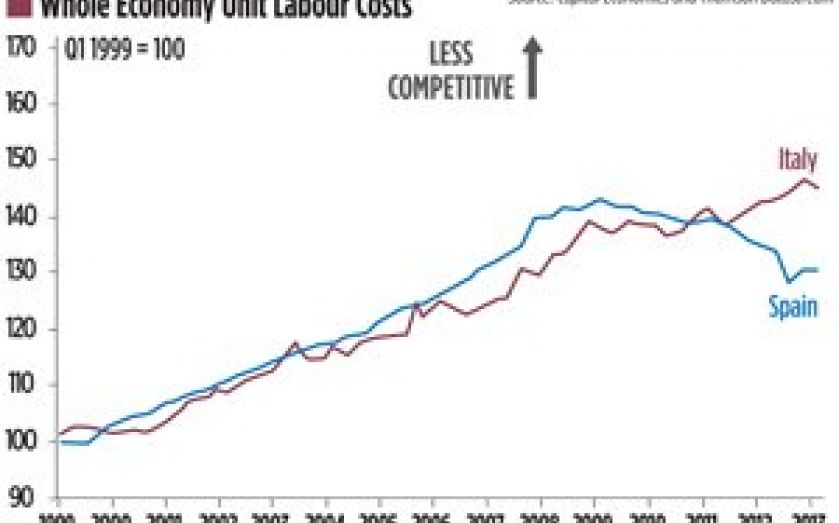

“Italy has lagged behind Spain in implementing structural reforms to boost competitiveness and raise the economy’s long-run potential growth rate,” says Ben May of Capital Economics. “And we have argued for some time that the country is Europe’s ticking time bomb.” Italian productivity has declined since 2009 (see chart), with unit labour costs rising 5 per cent, compared to a 9 per cent fall over the same period in Spain. And May says that there are few signs of Enrico Letta’s coalition acting to remedy this. “Even if we did see the government get it together, these issues take years to sort out.”

Alongside this, figures released by the Bank of Italy yesterday have added to worries over the strength of Italian banks, says Brenda Kelly of IG. The number of non-performing loans in the sector rose by 22.8 per cent year-on-year in September, following a similar year-on-year rise of 22.3 per cent in August. Bank lending to the private sector, meanwhile, fell by 3.5 per cent in September compared to a year earlier. “The heavily-indebted banking sector may act as a further drag on growth,” Kelly says.

CRISIS SCENARIO

And according to Ricky Nelson of Halo Financial, failing to return to growth quickly could lead Italy’s fiscal position to become untenable. Italy is on course for a relatively low budget deficit of 3 per cent this year, but this is against the backdrop of an enormous debt-to-GDP ratio of almost 127 per cent – well above the EU average of 92.2 per cent. Given this, says Simon Smith of FxPro, “it would not take a lot for the situation to deteriorate rapidly.” Smith says that, if Italy’s primary surplus was seen as heading towards negative territory, investors would quickly begin to see the situation as unsustainable. The resolve of the European Central Bank (ECB) would be tested in such a scenario, he says, given that it has made the Outright Monetary Transactions programme conditional on fiscal soundness.

Thursday’s GDP number will be key, and Joe Rundle of ETX Capital expects a sharp spike in bond yields and a hit to the euro if it disappoints. “We could also see some falls to Italy’s FTSE MIB stock index,” he says. The economy’s sheer size means its problems will effect the bloc as a whole. As ECB board member Joerg Asmussen said last month, “the future of the euro area will be decided in Rome.”