Investing in firms that ‘do good’: too good to be true?

BlackRock is aggressively launching products with high environmental, social, and governance (ESG) ratings. The New York City-headquartered global investment management corporation’s CEO, Larry Fink, recently predicted that assets under management in the ESG category will grow from the current $25bn to $400bn in 2028.

Investing in good corporates is intuitively appealing: who doesn’t want to make money while doing good? But do stocks that rank high on ESG metrics actually outperform? After all, so-called ‘sin’ stocks – think gambling, alcohol, tobacco and firearms – generate above-average returns, according to research. It would be a bit paradoxical if ESG and more-virtue-challenged factors both outperformed.

For insight into these questions, we explored ESG factor performance in the US stock market.

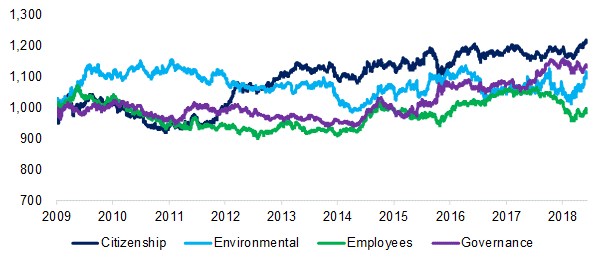

We explored ESG data from a US provider that aggregates ESG scores from multiple sources. Using data dating back to 2009, we divided ESG stocks into four main groups: Citizenship, Environmental, Employees and Governance. Next, we created beta-neutral long-short portfolios composed of the top and bottom 10% of US stocks as ranked according to these four factors. We only included companies with market capitalisations in excess of $1bn. The resulting portfolios are rebalanced monthly and include 10 basis points (bps) of cost per transaction.

Except for the Employees factor, all ESG categories generated positive returns from 2009 to 2018 (see chart). Based on these results, being a good corporate would seem to pay off.

ESG Factor Performance (Long-Short) in the US Stock Market (Source: FactorResearch)

But ESG factor performance shares some common trends, so the underlying portfolios likely have overlapping stocks. This is fairly logical. Companies that care about the environment, for example, may show similar regard for corporate governance and their employees.

For more insight into the drivers of ESG factor performance, we conducted a factor exposure analysis. We found that ESG factors are biased towards common equity factors. Of particular note are the negative exposures to both the ‘Value’ and ‘Size’ factors as well as positive exposures to the ‘Low Volatility’ and ‘Quality’ factors. R-squared calculations of the regression analysis from which the factor betas are derived average 0.5, implying that the common equity factors explain the performance of the ESG factors reasonably well.

The negative exposure to the Value factor suggests that stocks with high ESG scores have higher valuations than their less-conscientious counterparts. One possible explanation for this is that cheap stocks face temporary or structural issues that make achieving high ESG scores less of a priority for the companies.

Smaller companies also have fewer resources. Indeed, the average market capitalisation of the top 10% of the highest-ranking ESG stocks is almost twice that of the bottom 10% (see chart).

Average Market Capitalisations (US Billions), 2009–2018 (Source: FactorResearch)

Stocks with high ESG scores also display strong positive exposure to the Low Volatility factor. So lower-ranked stocks may be more volatile. There doesn’t seem to be an easy explanation for this, though it may reflect biases to certain sectors of the stock market.

The positive exposure to the Quality factor, which we define as a combination of debt-over-equity and return-on-equity, has a simpler explanation: less-levered companies tend to have management with a more long-term perspective, and highly profitable firms have more resources with which to achieve high ESG scores.

According to the analysis thus far, ESG factors generate positive excess returns. Good corporates pay off, in other words, which would seem to be good news for all investors.

However, this performance may be a product of exposure to common equity factors. The ESG factors exhibited negative exposure to the Value and Size factors, which both generated negative returns since 2009.

More importantly, ESG factors had large positive exposures to the Low Volatility and Quality factors. The Low Volatility factor was the best-performing factor since 2009 and accounts for much of the positive excess returns derived from ESG factors.

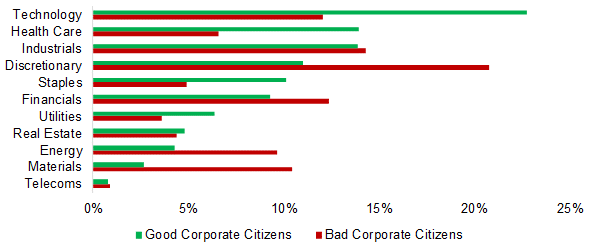

The factor lens is just one way through which to view the ESG factor puzzle. What does a sector analysis of companies that rank high and low on citizenship look like?

It turns out there are large sectoral biases. This is hardly a surprise. Energy stocks tend to have low citizenship scores (see chart). After all, oil-fracking companies in the US are more associated with earthquakes than friendly community engagement.

How does the breakdown by sectors reconcile with the factor exposure analysis?

The negative exposure to the Value factor is reflected in the significant overweight in technology stocks, which trade at higher valuations. Tech companies also tend to have less debt and high profit margins, which explains the positive exposure to the Quality factor. Finally, the positive exposure to the Low Volatility factor can be reconciled with an underweight in sectors such as Energy and Materials, which are more volatile than the average stock.

Citizenship ESG Factor: Breakdown by Sectors (Source: FactorResearch)

In conclusion, the notion that companies that care about the environment, look after their employees, and exhibit good governance outperform is likely too good to be true.

The drivers of performance since 2009 were common equity factors, especially the Low Volatility factor. ESG had significant positive exposure to this factor, which was the best performing factor over this period. While factor exposure might change over time, ESG investors currently run the risk of missing out on generating alpha if small and cheap stocks start outperforming low-risk and high-quality stocks.

ESG investing is one of the largest trends in the investment industry, as evidenced in the steady launch of ESG-compliant ETFs and funds by asset managers. However, given the focus on meeting the demands of multiple stakeholders, it implies that there are less resources available for shareholders. Investing in good corporates should be regarded as an alignment of interests, not as means to generate alpha.

If you liked this post, don’t forget to subscribe to the Enterprising Investor, where this post first appeared. It was written by Nicolas Rabener, MD of FactorResearch.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.