How the FTSE 100 returned 94 per cent without moving

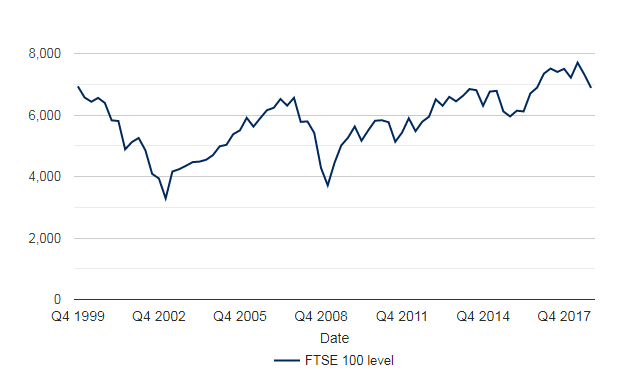

On New Year’s Eve 1999, the FTSE 100 closed at a then-record high of 6930. Few could have envisaged then that, 19 years on, the index would be lower. It stood at 6845 as at 14 December 2018. A negative return for investors over that long a period can be concerning, but it doesn’t tell the whole story of index returns.

While price-wise the FTSE 100 has fallen since 31 December 1999, if you include dividends the index has actually returned 93.5 per cent over the same period (or 3.54 per cent a year), according to Schroders’ calculations.

Dividends are a form of income paid out by companies to investors.

Dividend payments make up an important part of an investment’s total return, which includes capital growth.

Dividends can be taken as a cash payment or reinvested to buy more shares. If you opt for the latter, it enables you to benefit from the effects of compounding or what Einstein called the “eighth wonder of the world”.

Compounding enables you to earn returns on returns and can help your money grow faster.

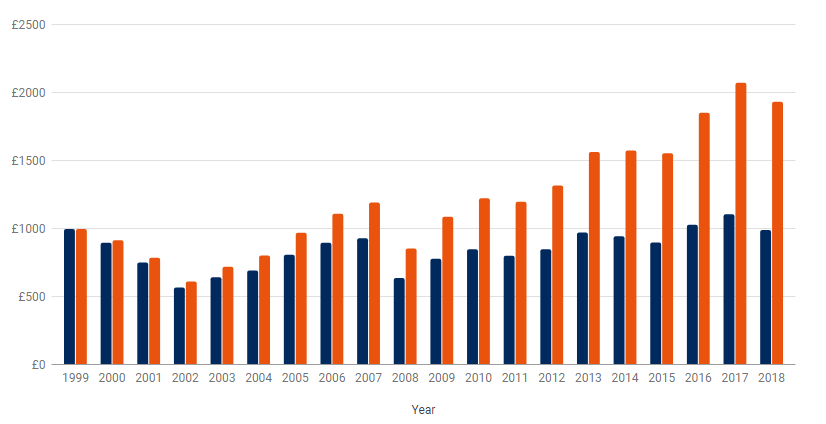

The dividend reinvestment effect

We have crunched the numbers. As the chart below shows, if you invested £1,000 into the FTSE 100 on 31 December 1999 and left it alone, it would be worth £993 without reinvesting dividends. That’s not adjusting for the effects of inflation or charges. It also does not include the value of taking dividends as a cash payment.

However, the picture changes dramatically if you had invested in the FTSE 100 and opted to revinvest the dividends its listed companies pay.

In this scenario, if you had invested £1,000 in the FTSE 100 on New Year’s Eve 1999, your investment would now be worth £1,935. That’s an annual return of 3.54 per cent, not adjusted for inflation or charges, compared with -0.04 per cent if you had invested in the index alone.

Ideally, stock prices should rise too, so your capital grows along with your income. But as the data shows, even when the actual price of the index has gone nowhere, you can still earn a return on your investment if you reinvest company dividends.

The orange bars in the chart below show the theoretical investment return had you reinvested your dividends. The blue bars show the return without dividends reinvested.

The power of reinvesting your dividend income

This material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Past performance is not a guide to future returns and may not be repeated.

Source: Schroders. Refinitiv data for FTSE 100 correct at 13 December 2018. Returns not adjusted for inflation or charges.

Sue Noffke, UK Equities Fund Manager, said:

“As the data shows, reinvesting the dividends companies pay can make a significant difference to the value of your investment. Of course, there’s no guarantee that your investment will rise in value over time.

“Dividend payouts are an increasingly important part of an investor’s portfolio, especially with bond yields near historic lows. The UK stock market currently pays out an average of around 4 per cent in dividends, compared with around 1.3 per cent for UK government bonds.

“It is one of the reasons we always advocate a long-run approach to investing. It’s also why dividends are often said to account for the majority of returns from the stock market over the long-run.”

“Dividend reinvestment is a simple technique. Over time, those seemingly small amounts reinvested can grow into much bigger sums if you use them to buy even more shares that pay dividends in turn.

“Investors need to do their research and make sure the company they are investing in can afford to pay their dividends on a sustainable basis. Your original capital is also at risk, so it pays to be picky.”

A poor run for the FTSE 100 explained

Like many stock markets around the world the FTSE 100 has suffered in the second-half of 2018, erasing most of the gains it made over the last two years.

Concerns over global economic growth, the potentially damaging effects of a trade war between the US and China and the uncertainty over the outcome of Brexit has hit investors’ confidence.

Read more:

- How Q4 2018 ranked among the worst quarters in history

- Financial markets in 2018: A year in review

- Which stock markets are cheap?

The FTSE 100’s travails also have some similarities to the events of 1999. In recent years, technology stocks such as Apple and Facebook in the US and Sage in the UK have helped propel stock markets to record highs.

These so-called “growth” stocks have been chased higher by investors who were willing to pay more and more for their potential earnings growth. The problem is that when it looks like the economy is about to slow, these growth stocks start looking expensive, as their projected earnings will become harder to achieve.

The sell-off in technology stocks is just part of the reason why the FTSE 100 and global stock markets have begun to retreat in 2018.

It was a similar story nearly 20 years ago at the height of the "dotcom" boom. Internet companies, or anything with ".com" in its name, were the most wanted stocks in town. When the bubble burst, the stock market began to fall, more than halving in value from top to bottom, as the chart below shows.

It is of course unwise to draw firm conclusions from stock market history and past performance is not a guide to future returns.

The FTSE 100’s rollercoaster ride since 1999

This material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Past performance is not a guide to future returns and may not be repeated.

Source: Schroders. Refinitiv data for FTSE 100 price index correct at 13 December 2018.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.