FTSE 100 history: how the index has changed over 33 years

The FTSE 100 index has just seen one of its quarterly changes with security firm G4S and real estate investment trust Segro promoted to the top 100.

Although perhaps small in themselves, these regular events have changed the face of the UK’s leading index since it was formed in 1984.

For the many investors whose savings are tied to the fortunes of this barometer of the stock market, these changes are crucial as they have fundamentally altered the risks and returns to which their investments are exposed.

The FTSE 100 now looks vastly different from the 1980s. Just 28 of the original 100 remain listed on the index. UK-focused businesses and conglomerates have been replaced by international juggernauts.

Unlike the US Dow Jones index, which has seen fewer changes over the past 100 years, the FTSE 100 has evolved to reflect the global economic revolution. This creates issues for investors to consider.

Through mergers, failures, promotions, demotions, new listings and globalisation the FTSE 100 has evolved to become a less UK-centric index and instead more closely reflecting the fortunes of the global economy.

To be fair, the index has never been a very good reflection of the UK economy – with key industries like motor manufacturing and technology either unrepresented or barely evident – but it has become even less of a bellwether for our leading industries.

What did the FTSE look like in 1984?

When the FTSE 100 launched in 1984 it was full of home-grown talent.

The index bulged with household names, such as retailer MFI Furniture, Boots the pharmacy and grocer Tesco. These were businesses built to meet the demands of the UK consumer.

The index had a number of firms which bore the national name too: British Aerospace and British Petroleum to name but two.

For anyone looking to benefit from a burgeoning UK economy by investing in a stock market, the FTSE 100 was the first port of call.

However, times have changed.

Who remains?

Only 28 of the original 100 companies remain listed on the FTSE 100. Below, we have used the names they held in 1984 and referenced what they did. For some, the nature of their business has evolved.

| Company name | Type of business |

| AB Foods | Food producer |

| Barclays | Bank |

| BAT Industries | Tobacco maker |

| British Aerospace | Aircraft, munitions and defence manufacturer |

| British Petroleum | Oil producer |

| Guest, Keen and Nettlefolds (GKN) | Fastners to automotive and aerospace manufacturer |

| Glaxo Holdings | Drug maker |

| Hammerson Prop INv & Dev | Commercial real estate investor |

| Imperial Group | Tobacco firm |

| J Sainsbury | Grocer |

| Johnson Matthey | Chemical maker |

| Land Securities | Commercial real estate investor |

| Legal & General | Insurer |

| Lloyds Bank | Bank |

| Marks & Spencer | Retailer |

| Pearson (s) & Son | Publisher |

| Prudential Corporation | Insurer |

| Royal Bank of Scotland | Bank |

| Reckitt & Colman | Consumer goods producer |

| Reed International | Recruitment firm |

| Rio Tinto | Miner |

| Royal Insurance | Insurer |

| Shell Trans & Trading Co. | Oil producer |

| Smith & Nephew | Medical equipment manufacturer |

| Standard Chartered | Bank |

| Tesco | Grocer |

| Unilever | Consumer goods producer |

| Whitbread | Restaurant and brewing company |

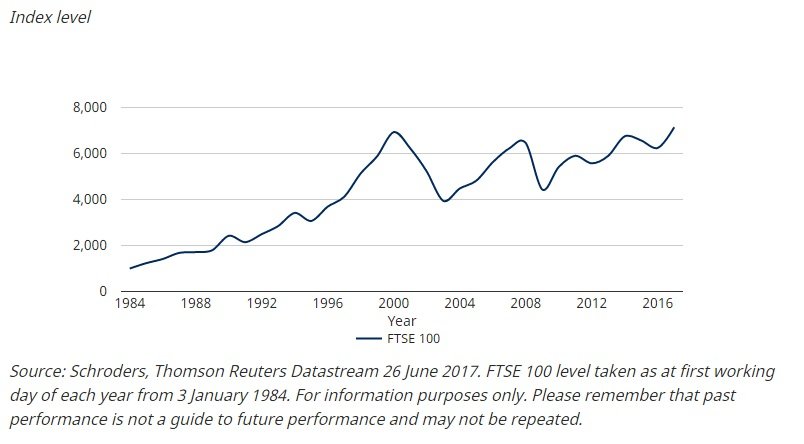

The components of the index have changed dramatically over the past three decades, as we outline below. But the index has still offered decent performance throughout. Since 3 January 1984, the FTSE 100 has risen by 614%.

If you include dividends the return is even greater. A £1,000 sum would theoretically have grown to £9,158, adjusted for 2% inflation which is the government target inflation rate. Past performance, of course, is not a guide to the future and investors should also consider the effect of any charges.

How the FTSE 100 has performed since 1984

How the FTSE 100 has changed since 1984

Below we list the names that have disappeared in the prev. Some have been taken over. Boots, founded in Nottingham in 1849, was bought by a Swiss private equity firm in 2007, the first FTSE member to be taken over by a private equity firm.

Another example is Allied Lyons. Back then it made a range of food and drinks including Lyons Maid ice lollies and Tetley beer. It began to experience problems in the late 1980s and merged with Domecq in 1994. It ceased trading in 2005 after being taken over by Pernod Ricard.

A recent example was Cadbury Schweppes, confectionery firm and maker of Dairy Milk chocolate bars. It was taken over by US food company Kraft for £11.5 billion in 2010.

Many have failed to survive in any form. MFI, which was founded as Mullard Furniture Industries in 1964, was relegated from the FTSE 100 soon after it was created. With an onslaught of rivals, such as Ikea, it finally closed down in December 2008.

Woolworths, pictured above, wasn't in the index at the start but was promoted soon after. As with MFI, it failed during the financial crisis with the last stores closing in early 2009.

Other original FTSE 100 members still exist but are no longer among the 100 biggest listed companies such as bookmaker Ladbrokes.

Here’s the list of companies no longer listed on the FTSE 100 in their original format. We cover some of the stories of those companies at the foot of this article:

| Company name | Type of business |

| Allied Lyons | Food and beverage producer |

| Associated Dairies Group | Grocer |

| Barratt Developments | Housebuilder |

| Bass | Brewer |

| Beecham Group | Drug maker |

| Berisford (S&W.) | Food producer |

| BICC | Building materials and construction |

| Blue Circle industries | Building materials and construction |

| BOC Group | Gas manufacturer and supplier |

| Boots | Pharmacist and drug maker |

| Bowater Corporation | Pul and paper supplier |

| BPB Industries | Building materials |

| British & Commonwealth | Conglomerate |

| British Elect, Traction Co. | Conglomerate |

| British Home Stores | Retailer |

| Britoil | Oil producer |

| BTR | Conglomerate |

| Burton Group | Retailer |

| Cable & Wireless | Telecommunications |

| Cadbury Schweppes | Confectionery maker |

| Eagle Star | Insurer |

| Commercial Union Assurance | Insurer |

| Consolidated Gold Fields | Gold miner |

| Courtaulds | Fabric and chemicals manufacturer |

| Dalgety | Food and agriculture products |

| Edinburgh Investment Trust | Investment trust |

| English China Clays | China clay extractor |

| Exco | Money broker |

| Ferranti | Electrical and engineering firm |

| Fisons | Pharmaceutical firm |

| General Accident Fire & Life | Insurer |

| General Electric | Conglomerate |

| Globe Investment Trust | Investment trust |

| Grand Metropolitan | Conglomerate |

| Great Universal Stores 'A' | Retailer |

| Guardian Royal Exchange | Insurer |

| Hambro Life Assurance | Insurer |

| Hanson Trust | Conglomerate |

| Harrisons & Crossfield | Chemicals and personal care firm |

| Hawker Siddeley Group | Engineering |

| House of Fraser | Retailer |

| Imperial Chemical Industries | Chemical manufacturer |

| Imperial Cont. Gas Association | Oil producer, bottled gas and utility firm |

| Ladbroke Group | Bookmaker |

| Magnet and Southerns | Kitchen retailer |

| MEPC | Property investor |

| MFI Furniture | Household furniture retailer |

| Midland Bank | Bank |

| Northern Foods | Food producer |

| P&O Steam Navigation Company | Shipping and logistics |

| Pilkington Bros | Glass manufacturer |

| Plessey Co. | Electronic, defence and telecoms company |

| Racal Electronics | Electronics and telecommunications firm |

| Rank Organisation | Leisure conglomerate |

| Redland | Building materials supplier |

| RMC Group | Concrete and quarrying products supplier |

| Rowntree Mackintosh | Confectionery maker |

| Scottish and Newcastle Breweries | Brewer |

| Sears holdings | Property to retail conglomerate |

| Sedgwick group | Insurance broker |

| Standard Telephone and Cables | Telecoms equipment manufacturer |

| Sun Alliance & London Insurance | Insurer |

| Sun Life Assurance Society | Insurer |

| Tarmac | Buildings materials supplier |

| Thorn EMI | Electrical rentals and music distributors |

| Trafalgar House | Property to shipping conglomerate |

| Trusthouse Forte | Hotelier and restauranteur |

| Ultramar | Oil and gas producer |

| United Biscuits | Food producer |

| Wimpey (George) | Housebuilder |

The FTSE 100 today

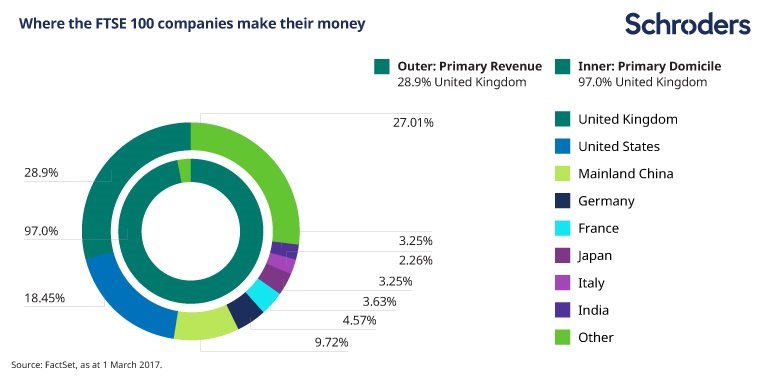

The index is now stocked full of global companies such as HSBC, oil producer Royal Dutch Shell and drug maker GlaxoSmithKline, all of which generate huge sales overseas. This is important.

The inner ring in this chart shows that the vast majority of companies – 97% – are domiciled or based in the UK. But only 29% of revenues are made here.

A better reflection of the UK economy would be the FTSE 250. Companies listed on the 250 generate 55% of their revenues in the UK, according to data from Factset.

This matters for two reasons: investing in the FTSE 100 does not necessarily mean you’re investing in the UK, which is important to understand if you’re trying to build a balanced portfolio; it also leaves FTSE 100 investments at the mercy of currency swings. For example, a strong dollar can be good for UK companies that make their money in dollars. Once the dollar revenues are converted into local currency it would be worth more.

- Find out more: How currency movements affect markets

James Rainbow, Co-Head of Schroders’ UK Intermediary Business, said: “The make-up of the FTSE 100 has changed dramatically in the past three decades. It is part of a constant cycle of healthy change for the stock market. Companies are bought, merged, or simply decline and leave the top flight. Some even go bust. But meanwhile new companies, often in new industries, constantly emerge to take their place.

“The expertise of fund managers in building and adjusting portfolios can help amid this constant flux. And as we’ve highlighted here, there are other factors for investors to consider. Don’t think that investing in the FTSE 100 is an investment in the UK’s fortunes.”

FTSE 100 weightings – a change in leadership

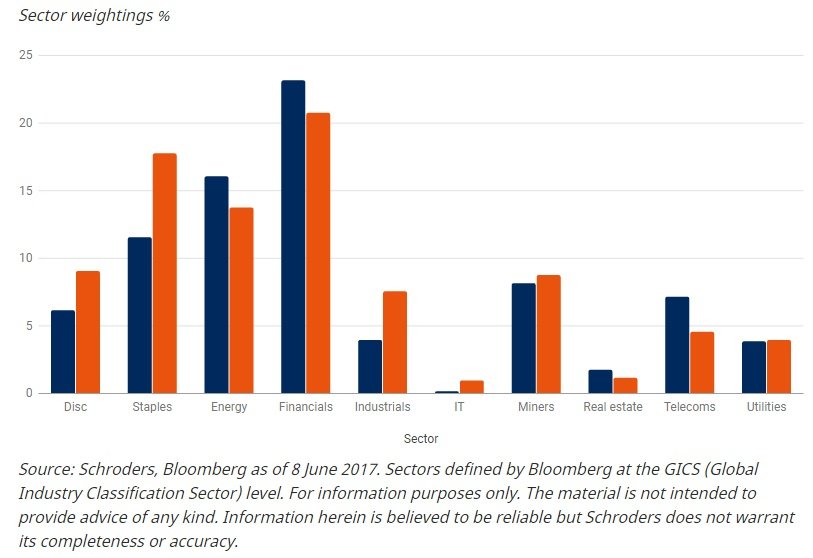

As the index has evolved so too have the sectors which dominate it. We looked at the available data, going back to 2007. Over the last ten years, consumer staples and healthcare have made big gains in their makeup of the FTSE 100.

The financial sector, made up largely of banks, and energy stocks, including BP and Royal Dutch Shell, are still among the biggest components but their importance has waned over the last decade.

It is useful to understand the sectors weightings in the context of a wider portfolio. Holding a large amount of money in the UK, may mean an investor has a large exposure to commodity stocks and therefore may not want to invest heavily in commodity stocks elsewhere.

FTSE 100 sector weightings comparison between 2007 and 2017

What is the FTSE quarterly review and why does it happen?

The FTSE continues to evolve with its constituents being reviewed every quarter. The index is changed to ensure it is a fair reflection of the current top 100 companies listed on the London Stock Exchange.

That sounds obvious but indexes such as the Dow Jones have made very few changes over their history, leading to accusations that it is out of touch and a poor reflection of real performance.

The FTSE 100 stocks of yesteryear

Here, we tell some of the stories of iconic companies that made up the FTSE 100 in 1984, but no longer exist today.

Hawker Siddeley was one of the most famous names in the aircraft industry. It is synonymous with the first and second world wars. Its founder, Tommy Sopwith, produced the Sopwith Camel which shot down Germany's World War one flying ace, the Red Baron. In the Second World War, its Hawker Hurricane played a crucial role in the Battle of Britain. More recently, it helped develop the Harrier jump-jet. The aerospace arm was taken into Bae in the 1970s. The remainder of the company was sold to BTR in 1992. BTR saw several mergers and today is now part of Schneider Electric of France.

It might seem strange now but renting electrical equipment was huge in the 1980s. Thorn EMIdominated the market through its ownership of rental firm Rumbelows and Radio Rentals. Thorn Electrical Industries began making lamps and lightbulbs in 1928 and went on to make televisions. In 1979 it merged with EMI, formed in 1931 as Electric and Musical Industries. Thorn EMI demerged in 1996 and by 1998 Thorn went into the hands of private equity and the brand disappeared. EMI, which was woven into British music culture through much of the 20th Century, was finally sold to Universal Music Group in 2012.

The demise of Rowntree Mackintosh as a listed entity was far quicker. Founded in York in 1864, the maker of Quality Street, Black Magic and Yorkie bars, dominated the shelves of sweet shops until the late 1980s. Its success attracted attention and by 1988 Rowntree Mackintosh was consumed by Nestle Confectionery for £2.55 billion.

Hanson Trust was a conglomerate created out of the former Wiles Group in 1964. It rose to prominence during the 1980s, boosted by the deregulation ushered in by Margaret Thatcher. It mounted a series of hard-fought takeover battles with major groups on both sides of the Atlantic, such as SCM, a US chemicals to typewriters business, and Imperial, a UK food to hotels conglomerate, which elicited claims of asset stripping. In its heyday it supplied electricity in the US and mined gold in Australia. You might have smoked its cigarettes, played with its golf clubs or seen its industrial cranes. It was one of the world’s largest companies and generated annual profits of over £1.5 billion. But by the late 1990s investors were beginning to lose confidence in conglomerates and the business demerged. It broke itself up into four separate companies: Hanson, Imperial Tobacco, The Energy Group and Millennium Chemicals.

Important Information: The views and opinions contained herein are those of David Brett, Investment Writer, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.