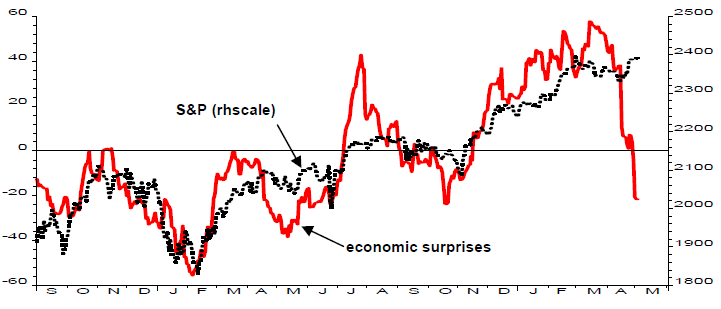

Can this chart really show what will happen next to the stock market?

Société Générale’s Albert Edwards, a market commentator that we on The Value Perspective blog respect very much, recently wrote his weekly strategy note on the dangers of stifling dissent and the comfortable ‘groupthink’ that can come about as a result.

On the first page was the following graph and – in a show of dissent that ought to please its originator – we have some issues with it.

Should we be worried?

Source: SocGen 4 May 2017, Datastream. Data Sep 2015 – May 2017.Past performance is not a guide to future performance and may not be repeated.

As you can see, one line on the graph shows the progress of the S&P 500, the main US equity market, over the last 18 months or so while the other illustrates the effect of US economic data surprises over the same period. It shows how the data is turning out versus expectations with readings above the line pointing to positive surprises.

Until recently, the two lines have taken a pretty similar course but the Surprise index has just fallen off a cliff.

Clearly the implication – underpinned by the graph’s title ‘Should we be worried?’ – is that the two indices have some sort of relationship and so the US stock market is set to follow suit.

As it happens, Edwards has been predicting a market crash for some years now – a consistently downbeat outlook that has gained him the nickname ‘Dr Doom’ – but might one really now be around the corner?

Well, maybe the market will shortly follow the path of the Economic Surprises index and maybe it won’t. If it does, however, we have serious doubts on The Value Perspective blog that the above graph will have any bearing on the matter.

This is not because we disagree with the underlying data – the graph shows what it shows – but we do take issue with the way the data is presented.

In stock market terms, 18 months is not much more than a blink of an eye and so finding an apparent relationship between two indices – what is known in investment as ‘correlation’ – over such a period cannot really be seen as an argument for or against anything.

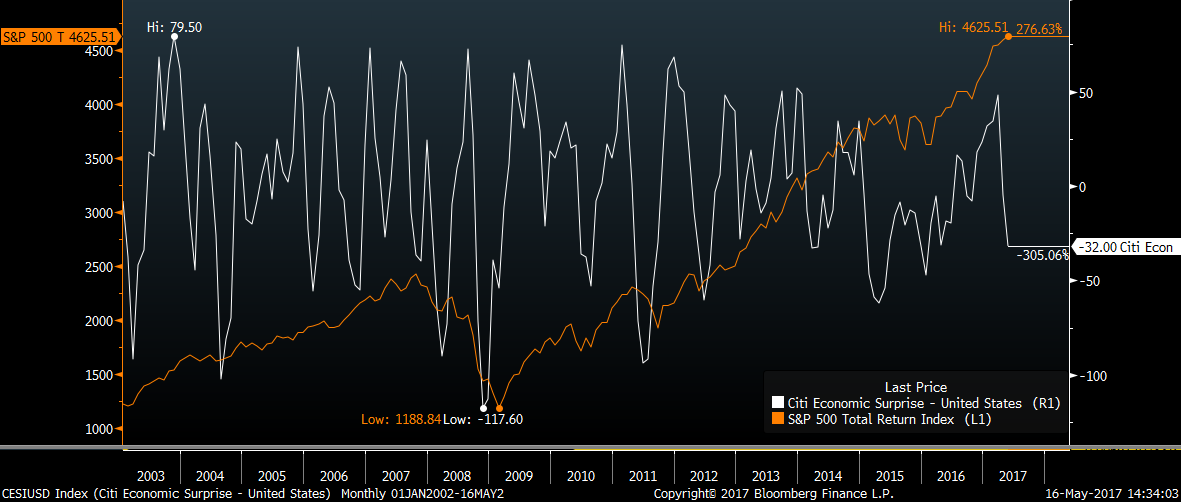

To underline the point, take a look at the following graph, which shows a very similar series of data but over a much longer period of time.

Citi Economic Surprises (US) v S&P 500

Source: Bloomberg, 16 May 2017. Past performance is not a guide to future performance and may not be repeated.

And, as you can see, there is now neither rhyme nor reason to the relationship, which suggest that – while there may indeed have been some short-term correlation, there was never any causal link.

What the above graph is then, really, is another example of the ‘p-hacking’ we touched on in our ever-expanding and increasingly inaccurately named Jellybean Trilogy.

The ‘p’ in that term stands for the 0.05 or 1-in-20 threshold below which any scientific or research finding becomes statistically significant.

While we are in no way suggesting any intention to mislead with the above graph, there are thousands of economic indices to compare and there will be periods where two appear convincingly correlated.

In truth, however, the future of short-term market movements – and indeed of everything else – remains stubbornly hard to predict.

More value investing ideas:

-

When to buy a company with a falling share price – and when not to

-

The calmest markets in 20 years – and why that should make you nervous

Ian Kelly is an author on The Value Perspective, a blog about value investing. It is a long-term investing approach which focuses on exploiting swings in stock market sentiment, targeting companies which are valued at less than their true worth and waiting for a correction.

- Weekly round-up: The best of our value investing ideas

Important Information: The views and opinions contained herein are those of Ian Kelly, Fund Manager, and may not necessarily represent views expressed or reflected in otherSchroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.