What is the Bank of England’s ‘once in a generation’ Bernanke review?

This Friday, the Bank of England will reveal the results of its “once in a generation” review into its internal operations, a review that some economists think could lead to profound changes in Threadneadle Street.

The review, launched last summer, was led by Ben Bernanke, who chaired the Federal Reserve between 2006 and 2014.

Like an anthropologist in the field, Bernanke has been studying the sometimes arcane practices in the Bank for the past few months and is expected to make a number of suggestions to improve its policymaking.

Before looking at what made the change, it’s worth recapping why the review was launched in the first place.

Why we’re here

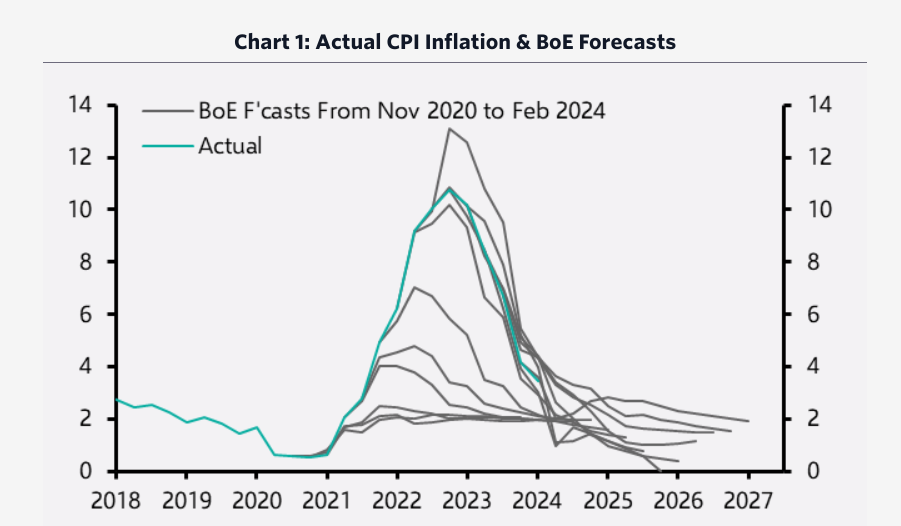

The Bank of England struggled to get to grips with the surge in inflation following the Russian invasion of Ukraine, repeatedly having to revise up its inflation forecasts.

Because it underestimated inflation, the Bank was too slow to raise interest rates. In its May 2022 Monetary Policy Report, when inflation was 7 per cent, the Monetary Policy Committee (MPC) thought a one per cent Bank Rate would be sufficient to return inflation to target. Needless to say, this was not quite how it turned out.

Now, on the way down, inflation has surprised to the downside too. Many critics argue the Bank is now being too slow to cut rates.

It’s worth pointing out that the Bank is not alone in facing these criticisms. Central banks all over the world were caught off guard by the sudden surge in inflation and its spillover impacts on the wider economy.

Rob Wood, chief UK economist at Pantheon Macroeconomics, suggested that the forecasts failed because they were based on a limited data set when inflation was low and relatively stable.

“Part of what went wrong, we think, was that relying on economic models estimated over a period of low and stable price rises—which forecast the quick return of inflation to target—was misleading,” he said.

What is the Bernanke review about?

Given the mistakes made over the past few years, it is sensible – indeed laudable – that the Bank of England is giving itself an opportunity to stop and think about what went wrong.

It identified a few key areas:

- The analytical framework for taking account of significant shocks and shifts on the supply as well as the demand side of the economy.

- The appropriate conditioning assumptions in projections, including the interest rate path on which the forecast is based.

- The role of the forecast in the MPC’s policy decisions and communications, including the roles of the MPC and the staff in the development of the official forecast.

- Material provided to the MPC to assist the discussion and communication of the outlook and the risks around that.

The first point relates to how the Bank should communicate uncertainty in an era when major shocks seem to come around with alarming frequency.

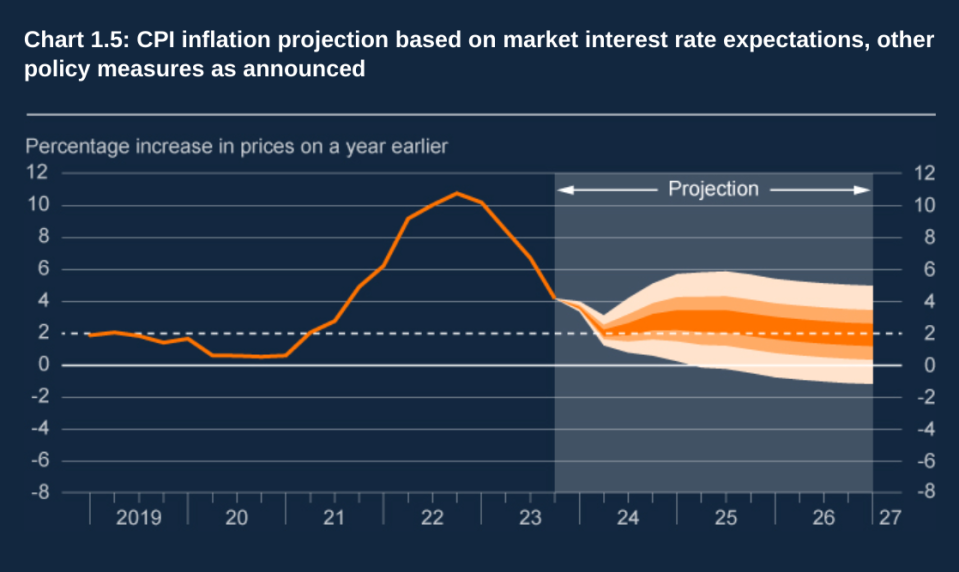

The second point relates to the Bank’s current policy of publishing two forecasts, one based on market expectations for interest rates and the other based on a constant Bank Rate.

Note that neither of those is what the Bank itself thinks about interest rates.

Gertjan Vlieghe, a former MPC member, described this procedure as follows: “We communicate about what we think we may do by showing you a forecast of what will happen if we do something else”. Not exactly clear.

The final two points are basically about how the Bank can communicate its position as clearly as possible.

What are the likely outcomes of the Bank of England review?

Bernanke is likely to suggest that the Bank of England move away from its dual forecasts based on the market curve and a constant Bank Rate and instead move to one central projection.

Exactly what form this will take is unclear. During his time at the Fed, Bernanke introduced ‘dot-plot’ graphs which give markets an anonymised picture of what rate-setters think is an appropriate path of interest rates.

Andrew Bailey, the Bank’s governor, is reportedly sceptical about dot-plot projections. Other policymakers have also expressed their scepticism.

Economists, on the whole, were supportive of a move to one central projection, with a clearer guide to the Bank’s preferred path of interest rates.

“The MPC should base forecasts on its preferred path for interest rates,” Pantheon’s Wood said. “That will allow it to better explain its choices, the forecasts will be internally consistent, and policymakers can better be held to account for their decisions”.

Paul Dales, chief UK economist at Capital Economics, agreed. “The benefits of a clear projection for the future path of interest rates outweigh the possible drawbacks,” he said.

The problem then is how to communicate uncertainty about one central forecast. One likely casualty to this question are the Bank’s ‘fan charts’. These graphs use a distribution of probabilities to signal uncertainty around the forecast.

The only problem is that in a time of increasing uncertainty, these charts have become increasingly wide. Dales said “the width of the fan charts has become so large that it is meaningless”.

Bloomberg has reported that the Bank is more likely to move to scenario-based analyses, an approach taken by the Swedish Riksbank. Essentially, these would allow the Bank to model the impact of surprise events.

For example, during the pandemic, scenario-based analyses would have enabled the Bank to convey how it would respond to different outcomes – like longer lockdowns or a successful vaccine.

The Bernanke review is not prescriptive, and it will take time for the reforms to come into force, but there is no doubt this could lead to big changes at the Bank.