UK remains world’s third largest crypto economy, and biggest in Europe

Blockchain data platform Chainalysis has released two new chapters of its 2023 Geography of Cryptocurrency report – the first on Central, Northern, and Western Europe, and the second on Eastern Europe.

The much-anticipated report – regarded highly among cryptocurrency and blockchain firms – is often cited as a barometer of the state of the global industry.

The update, released moments ago, shows the UK remains the world’s third largest digital asset economy, and the biggest throughout Europe in terms of raw transaction volume, at an estimated $252.1 billion received in the past year.

However, many experts fear this order could change dramatically following the Financial Conduct Authority’s stifling clampdown with new rules surrounding the marketing of cryptocurrency-related products.

Here is the summarised Chainalysis report…

Institutions in Central, Northern, and Western Europe Broaden Horizons with DeFi and Web3 Experimentation

Central, Northern, and Western Europe (CNWE) is the second largest cryptocurrency economy in the world this year, behind only North America. The region accounted for 17.6% of global transaction volume between July 2022 and June 2023, and received an estimated $1 trillion in on-chain value during the same time period.

Across the region, decentralized finance (DeFi) is the most popular service category, accounting for 54.8% of cryptocurrency value received. DeFi has played a key role in CNWE’s crypto adoption over the past few years, most notably with decentralized exchanges (DEXes). While much of this activity was driven by retail, institutions across the region are now opening doors to DeFi in light of regulatory frameworks that support diverse web3 initiatives.

When comparing inflows on both centralized and decentralized exchanges during the first six months of 2023 to the first six months of 2022, we see interesting differences in activity. First, 21 countries in CNWE experienced reductions in inflows to both types of exchanges. Seven countries saw an increase in inflows to decentralized exchanges: Albania, Luxembourg, Latvia, Spain, the United Kingdom, France, and Lithuania. Note that the two countries with the highest increases in DeFi activity — Albania and Luxembourg — are smaller in terms of overall transaction volume, thus making it comparatively easier to grow significantly.

CNWE includes six of the 50 highest grassroot adopters of cryptocurrency around the world: the United Kingdom (14), Spain (22), France (23), Germany (26), Italy (37), and the Netherlands (39). Keep reading to learn more about what is driving crypto adoption in these countries.

Spotlight: the United Kingdom is CNWE’s biggest crypto economy

In addition to ranking 14th on our Global Crypto Adoption Index for grassroots adoption, the U.K. is third in the world in terms of raw transaction volume, at an estimated $252.1 billion received in the past year.

Jamie McNaught, Founder and CEO of U.K.-based crypto exchange Solidi, noted that U.K. consumers are focused on crypto from both a technological and investing standpoint. He stated, “Customers in the U.K. typically seek alternatives to poor savings and investment returns — varying from propping up underperforming investment portfolios to customers going all in, looking for high returns on tokens or NFTs. While NFTs are no longer in favor, customers continue to look for overperforming, long-term returns in Bitcoin — particularly with the anticipated 2024 halving — and Ethereum, while also making sizable bets on XRP, Cardano, and Solana.” McNaught added that the U.K.’s institutional crypto growth is not surprising, given the country’s reliable and connected banking sector, and its history of relatively low inflation, until recently.

It appears that this activity has not been dampened by the U.K.’s regulatory developments; regardless, reactions to recent legislation have been mixed. In June 2023, the Financial Services and Markets Bill became U.K. law, adding a definition of crypto assets to existing financial services legislation while also granting the government powers to create a bespoke framework for stablecoins. The data suggest that the passage of the bill may have impacted stablecoin activity. In the months leading up to the enactment, the share of institutional transaction volume (based on transfer sizes) to centralized exchanges decreased and was replaced by an increase in Bitcoin and Ether shares.

Some financial institutions, such as venture capital firm Andreessen Horowitz (a16z), viewed the Financial Services and Markets Act 2023 (FSMA 2023) as a positive step forward. Soon after the bill was passed, a16z Founding Partner Chris Dixon announced, “we’re thrilled to open our first international office in a jurisdiction that welcomes blockchain technology and is committed to creating a predictable business environment by pursuing regulations that both embrace web3 and protect consumers. We look forward to helping foster the growth of the UK web3 ecosystem while the proper regulations come online.”

McNaught explained that it may take a while before the crypto industry in the U.K. sees significant tangible impact from the Act and other regulatory developments that are in progress. “We’re still waiting on additional rules bringing activities in scope under the Designated Activities Regime. We expect to see most stablecoins as well as a significant number of tokens brought in scope with further secondary legislation. For most crypto firms, the main focus right now is the introduction of the FCA Financial Promotions Regime in October 2024. This covers all buying and selling of crypto assets — the listing of a price and a buy button is considered a financial promotion.” From October 8, 2024, firms must meet FCA standards or they won’t be able to lawfully communicate crypto-related financial promotions to customers in the U.K.

Indeed, businesses such as crypto exchange Luno and crypto-friendly payments provider PayPal, announced their intentions to pause U.K. customers’ abilities to purchase certain cryptocurrencies, citing time needed for changes to be compliant with the FCA’s new laws. McNaught concluded, “Firms need certainty and clear guidance, delivered by the regulator in a timely manner, particularly when the adherence to regulations poses significant challenges or has the potential to cause significant harm toward consumers.”

How Markets in Crypto-Assets (MiCA) has impacted crypto innovation in the EU

In June 2023, the European Union approved the Markets in Crypto-Assets (MiCA) Regulation, putting in place a unified approach toward regulating crypto activities in all EU countries. MiCA’s provisions will take effect starting from mid-2024 and aim to promote financial stability and market integrity by establishing a single licensing regime that will supervise public offers of crypto assets, trading, and institutions involved in the digital asset space. Already, MiCA appears to have created favourable environments for crypto innovation. We spoke to industry leaders in France, Italy, and Germany to gain insight into these impacts.

In France, the Autorité des Marchés Financiers (AMF) immediately welcomed MiCA and soon drafted additional supportive technical standards for the industry as the country moves toward the MiCA licensing regime. Lorie Veillere, Lead Compliance at Paris-based cryptocurrency market maker and financial services platform Flowdesk, believes these regulatory developments are primary drivers for France’s crypto adoption. “Even before the introduction of MiCA, France’s attitude toward crypto regulation was broadly supportive,” she stated. “For example, the 2019 PACTE Act introduced France’s first regulatory framework for crypto assets and detailed that crypto entities must demonstrate that they have implemented an AML-CFT framework in order to be registered as a Digital Asset Service Provider (DASP).”

At the same time, France’s crypto hub in Paris has been flourishing. Société Générale obtained France’s first crypto license in June 2023 to offer its institutional clients improved custody, trading, and sales opportunities. Major players in the space, including Binance, Crypto.com, and Circle, chose Paris as their European headquarters. And blockchain developers have flocked to the city to work on decentralized projects. These advancements likely contributed to France’s ranking of number 23 on this year’s Global Adoption Index and number four in the region in terms of raw cryptocurrency value received.

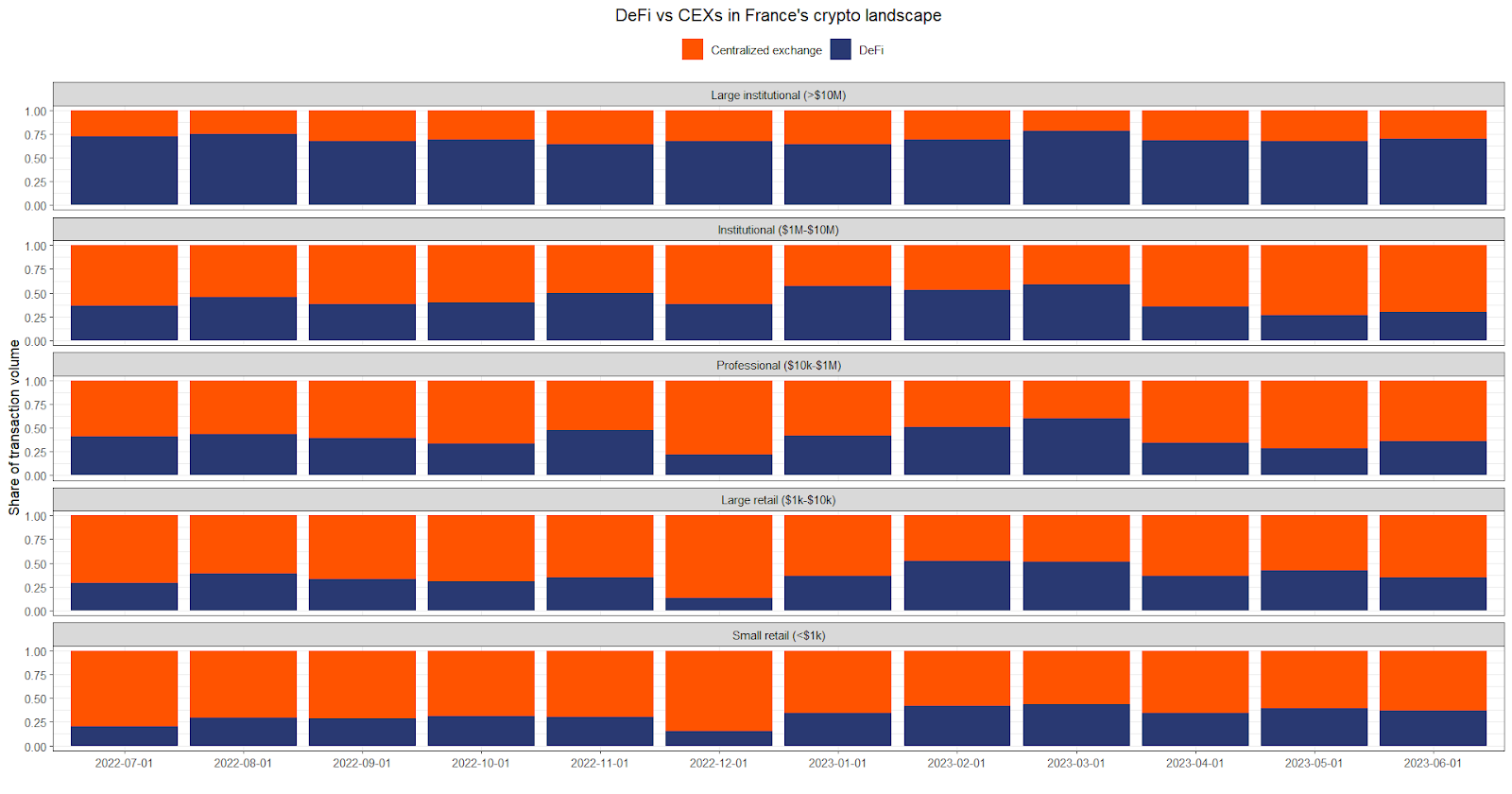

Many larger digital asset players in France appear to be prioritizing DeFi exploration, which is reflected in our data. As the below chart illustrates using transaction size data, large institutional sized transfers occur more often in DeFi than on centralized exchanges. These levels have remained relatively steady over the past year.

France also emerges as a leader in terms of percent change of raw value sent to DeFi services. The higher spikes around November 2022 and May 2023 shown in the below chart were likely driven more by users seeking to trade on volatility caused by the collapse of FTX and the decline of Silicon Valley Bank and USDC prices, respectively, rather than regulatory developments across Europe. Regardless, activity in France was typically more extreme than in other countries during these periods, illustrating its strong DeFi presence.

Veillere concluded that France’s future as a crypto hub depends on additional regulatory progress. “French regulators and public authorities frequently consult industry leaders — often those with knowledge of DeFi — to obtain insights on the state of the sector and technical developments. The most recent consultation occurred in May 2023. This proactive approach could enable the implementation of one of the first efficient DeFi regulatory frameworks.”

It is possible that MiCA will also be a driving force for crypto growth in Italy, especially in cities with tech-savvy populations where crypto initiatives are already on the rise. Nearly three years ago, Banca d’Italia created the FinTech Milano Hub, a modern update to Milan’s financial district where industry leaders in both the private and public sectors collaborate on digital initiatives. Several months after MiCA was approved, Banca D’Italia partnered with Cetif Advisory to help institutions explore DeFi and tokenized assets. This project is currently utilizing Ethereum-based Layer 2 protocol Polygon Labs and tokenization platform Fireblocks to achieve its aims. As Alessandro Perillo, Chief Operating Officer of Italy-based Young Platform told us, “The FinTech Milano Hub is poised to be a critical player in fostering crypto innovation in Italy. Given Italy’s robust financial sector and technological capability, the hub could potentially lead innovations in blockchain technology, DeFi applications, and perhaps even pioneer new ways to integrate cryptocurrency into traditional finance.”

Germany is another country in the region which offers some of the key elements necessary for crypto growth. Dr. Sven Hildebrandt, Executive Director of Business Development and Strategic Partnerships at Boerse Stuttgart Digital, a fully regulated infrastructure partner for crypto and digital assets in Europe, told us about some key drivers for crypto adoption in Germany, including trustworthy regulation and education provided to investors by institutions. Additionally, he noted that, “Germany has a very strong historical routing in technical blockchain development. For example, if you look for node operations, you will find that Germany has the second most full nodes for Bitcoin after the U.S., which is remarkable. Germany also has the largest number of web3 jobs in absolute terms with over 22,400 jobs in the crypto and blockchain sector.”

In April 2023, the German government approved the Future Financing Act (“ZuFinG”), which monitors crypto asset custody and provides insolvency protection. Since then, we’ve seen several institutional developments. Boerse Stuttgart Digital is working on a fully insured crypto staking service in collaboration with Munich Re, which is expected to go live in the first half of 2024. Other innovations include Deutsche Bank’s partnership with Taurus to explore crypto custody and tokenization, and the German-Dutch central banks’ “Project Atlas” to map on-chain transactions.

Dr. Hildebrandt believes that the effects of these acts are not yet tangible to the general public, however, given that most developments happen in the background. Regardless, these acts represent significant progress in the right direction. “Overall, MiCA paves the way for broad acceptance of cryptocurrencies and digital assets. Its uniform, clear rules and focus on consumer protection throughout the EU create a secure environment that strengthens trust in the market and opens doors to crypto for both individual investors and institutions.”

CNWE’s crypto future

Although crypto adoption in CNWE is still in its early stages, many industry leaders are excited about what’s to come. Perillo stated that the potential for innovations — especially in areas like smart contracts, NFTs, and DeFi — is immense. “It will be interesting to see how traditional financial institutions, tech startups, and regulators navigate through the challenges and opportunities presented by the crypto space.”

As these new opportunities and challenges emerge in the industry, regulations like MiCA will continue to play key roles. However, as Veillere notes, “much remains to be done, particularly in terms of harmonizing the regulatory framework for all European countries. Concerning MiCA’s future, I think the text will undergo several amendments before a real balance is found between the requirements of the regulators, the crypto players, and the political will to expand this sector.”

This material is for informational purposes only, and is not intended to provide legal, tax, financial, or investment advice. Recipients should consult their own advisors before making these types of decisions. Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.

This website contains links to third-party sites that are not under the control of Chainalysis, Inc. or its affiliates (collectively “Chainalysis”). Access to such information does not imply association with, endorsement of, approval of, or recommendation by Chainalysis of the site or its operators, and Chainalysis is not responsible for the products, services, or other content hosted therein.

Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.