Joblessness falls to brink of interest rate threshold

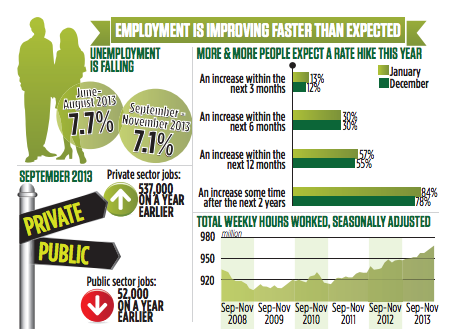

UNEMPLOYMENT plunged to 7.1 per cent during November, according to figures released yesterday, leaving the Bank of England’s forward guidance policy hanging in the balance.

The rate of joblessness fell from 7.4 to 7.1 per cent in just a month, the fastest drop in over 15 years, with the labour market improving at an unexpectedly rapid rate.

The drop leaves Bank of England governor Mark Carney in a precarious position. The Bank’s autumn inflation report, released only six months ago, said that when unemployment fell to seven per cent it would reassess its historically low interest rates, but projected that the threshold would not be met until 2016.

Yet the Bank has now been forced to admit that its expectations were wrong. In minutes of the last policy meeting, released yesterday, the Bank said: “The unemployment rate is now likely to reach the seven per cent threshold materially earlier than previously had been expected.”

The employment rate rose to 72.1 per cent in the three months to November, a 0.5 percentage point increase from the previous quarter.

In comparison to the same three months in 2012, 450,000 more people are in employment, and 172,000 fewer people are unemployed. There are also now fewer people claiming jobseekers’ allowance than at any point in the past four years, with 1.25m people accessing unemployment benefits. In the past year, the number fell by 307,000, a reduction of nearly a fifth.

Youth unemployment also saw a welcome decline, falling from 21 to 20 per cent in the three months to November.

“Given all this strength in labour market activity, the pay situation remains very benign. Headline average weekly earnings growth was just 0.9 per cent in November,” said David Tinsley of BNP Paribas. The consumer price index (CPI), Britain’s official measure of inflation, swelled by 2.1 per cent over the same period, meaning that real wages are still decreasing.