Cash Isa vs stock market Isa: which has returned the most?

Saving money into a stocks and shares Isa over the last 19 years would have returned two-thirds more than a cash Isa, according to calculations by Schroders.

The stocks and shares Isa carries more risk and is subject to greater volatility than the cash Isa, which also provides far greater protection for your investment. You can of course invest in both a cash Isa and stocks and shares Isa to help spread your risk. If you are not sure as to the right investment for you, speak to a financial adviser.

Schroders data tracked the performance of two separate investments of £1,000, one in a cash Isa and one in a stocks and shares Isa, between 1999, when Isas were first introduced, and 2018.

To calculate the cash Isa returns we used the average rate of interest, according to Bank of England data, between each tax year over the last two decades. For stocks and shares Isa returns we used the MSCI World Total Return index, which includes dividend payments, with returns calculated in sterling.

Returns for both the cash Isa and the stocks and shares Isa have been adjusted for inflation. We have also assumed a 1.5 per cent management cost for the stocks and shares Isa*, although investors might pay less.

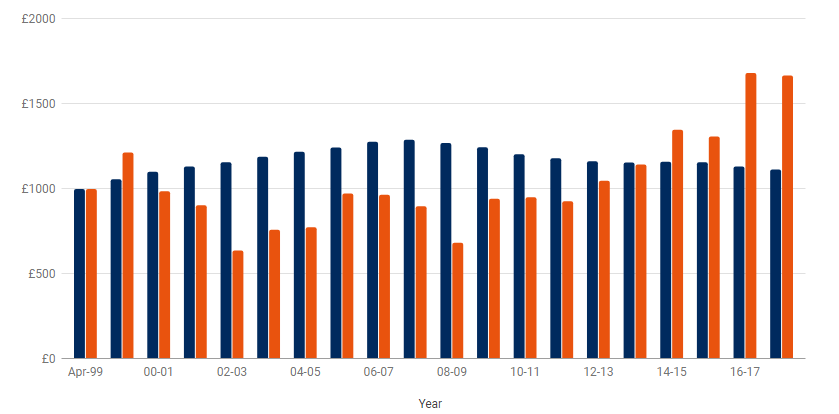

As the chart below shows, £1,000 saved into a cash Isa (blue bars) in 1999 might now be worth £1,115, a return of 0.6 per cent per year. The same investment in a stocks and shares Isa (orange bars) could now be worth £1,667, an annual return of 2.9 per cent. That is an increase of £552 or 50 per cent over the growth of a cash Isa.

Cash Isa and stocks and shares Isa returns: 1999-2018

End of year balance (£)

Past performance is not a guide to future performance and may not be repeated .The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

Source: Schroders. Annual UK inflation data according to Inflation.eu. Cash Isa returns calculated from Bank of England data: average yearly interest rate of UK monetary institutions for sterling cash Isa deposits from households. Stocks and shares Isa returns calculated using the MSCI World Index – total return. Calculations are net of inflation. The material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy.

What is an Isa?

‘Isa’ stands for Individual Savings Account. It is a tax-efficient account, for instance it is sheltered from personal income tax and capital gains tax. Anyone over the age of 18 can save up to £20,000 a year into a stocks & shares Isa or from age 16 for a cash Isa and withdraw the proceeds, at any time, although fees and charges may apply. Tax rules for Isas may change in the future, and their tax advantages depend on an individual’s circumstances.

A saver can choose to keep any savings in cash and in return receive interest payments, just like a bank account. Or they can invest their money into financial markets to try to get better returns.

There are pros and cons with each. If you leave your money in cash, the only risk is if the bank fails and even then, up to £85,000 is protected by the Financial Services Compensation Scheme (FSCS) for each bank where a saver has money, offering assurance. But cash returns have historically been lower.

Investing your money into financial markets might offer the potential of higher returns but it also comes with the risk that you could lose money.

What has affected Isa returns over the last two decades?

For the first 10 years, keeping your investment in cash might have seemed like the best option. A combination of higher interest rates and two stock market crashes meant returns on cash outperformed those in stocks and shares.

It is hard to imagine now but interest rates on cash deposits were as much as 6.5 per cent in the early 2000s. At its peak in the 2007/08 tax year the cash Isa might have been worth £1,289.

While cash savers enjoyed relatively high returns, investors in the stock market were faced with two of the biggest stock market crashes in history.

The first was the result of the bursting of the dot com bubble at the turn of the millennium, when highly-rated technology stocks were sold off, which was closely followed by an economic slowdown. From a peak of £1,214 in the 1999/00 tax year to a low of £638 by 2002/03 investors could have suffered a 47 per cent fall in the value of their portfolio.

After five years of recovery the stock market slumped again. In 2008 the collapse of the US housing market triggered the global financial crisis. The value of the stocks and shares Isa could have fallen 29 per cent from a peak of £966 in 2006/07 to a low of £684 by 2008/09.

Since 2008/09, however, stocks and shares has outperformed cash. During that period the average savings account could even have lost money.

To prevent the global financial crisis from deepening, central banks had to take action. This included reducing the UK bank rate to as little as 0.25 per cent, meaning returns on cash were eroded by higher inflation. From a peak of £1,289 in 2007/08 the value of the cash Isa fell in real terms to £1,115 by 2017/18, a drop of 13.5 per cent.

Stocks meanwhile have benefitted from central banks’ monetary policy. Because interest rates have been so low investors have been forced to back more risky investments to generate higher levels of income, thereby generating demand for shares. From a low of £684 in 2008/09 the value of the stocks and shares Isa could have risen to £1,667 by 2017/18, a gain of 244 per cent.

But while stocks and shares returns may have been higher, they have also been more volatile, with many sharp falls and rises. Cash, in contrast, has been a more stable home for Isa money.

Money still pouring into cash Isas

People have consistently put more into cash Isas despite the historic difference in returns.

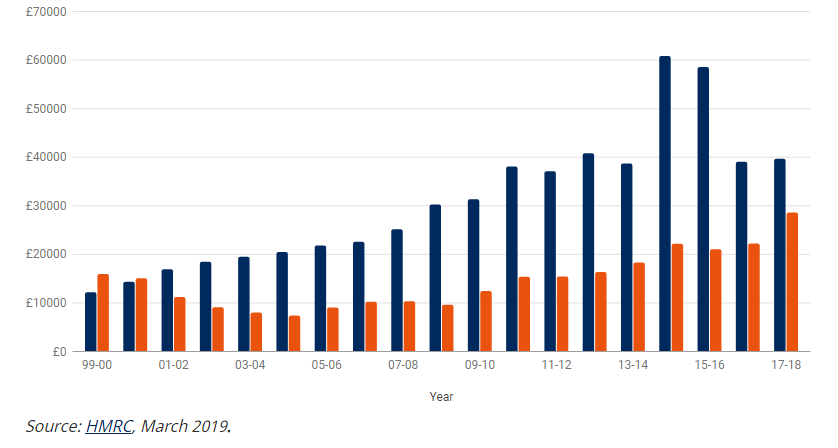

When Isas were launched in 1999, the total cash Isa subscriptions were £12.3 billion compared to £16.1 billion for stocks and shares Isas, according to UK government statistics. So 57 per cent of the money went into cash Isa savings accounts.

That was one of only two tax years, the other being 2000/2001, where investors have put more money into stocks and shares Isas. Demand for cash Isas over investment Isas has grown ever since.

The difference was most stark in 2008/2009, the height of the financial crisis, when £30.4 billion went into cash and £9.7 billion into investments.

The gap between the two has remained significant since then, although as the chart below illustrates the percentage of money going into stocks and shares Isas has risen in the last two years.

Still, by the end of the 2017/2018, 58 per cent of the money went into cash Isas despite a global economic recovery helping stock markets to make decent gains.

Cash Isa vs stocks and shares Isa subscriptions: 1999-2018

Subscriptions (millions £)

Claire Walsh, Personal Finance Director at Schroders, said: “As the HMRC data suggests, keeping money in cash clearly has its attraction for the majority of savers, despite the low interest rates we have had for the last 10 years.

“It is hard to blame them. It has been a tumultuous start to the new millennium. Keeping your investment in cash at least prevents the investor from having to endure the emotional rollercoaster ride that comes with stock market fluctuations.

“However, it is a state of mind. Cash is effectively a false safety net in times of ultra-low rates because of the corrosive effect of inflation on purchasing power. Providing investors take a long-term approach, usually more than five years, the stock market has historically provided a better rate of return.

“Our data, while it offers no guide to the future, shows this has happened recently, but there is also longer-term data to support the notion. The Barclays Equity-Gilt Study found that UK shares returned an average 5.1 per cent a year since 1899, with inflation factored in; cash returned 0.8 per cent a year.

“Of course, we believe diversifying your investments is important. Having a mix of assets, including some in savings, is a wise approach.”

Stocks and shares Isa carries more risk and is subject to greater volatility than the cash Isa. If you are not sure as to the right investment for you, speak to a financial adviser.

* The calculation based is on a typical annual fund charge of 0.75 per cent -1.25 per cent, as stated by the government-backed Money Advice Service. Investors may also face a platform cost – a charge by a third party company to hold a portfolio of funds on their behalf. For this reason, we’ve assumed an overall cost of 1.5 per cent. There may be additional costs for investors who also receive advice.

For more insights from Schroders visit their content hub and follow them on twitter

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.