Are we witnessing the US dollar’s fall from grace?

November’s multi-asset chart of the month highlights how a global shortage of US dollars could be reversing. This could signal the beginning of a weak phase for the currency.

A world in which money is scarce might appear to be a far-fetched idea. But for US banks in the business of taking deposits and making loans, this has become a reality.

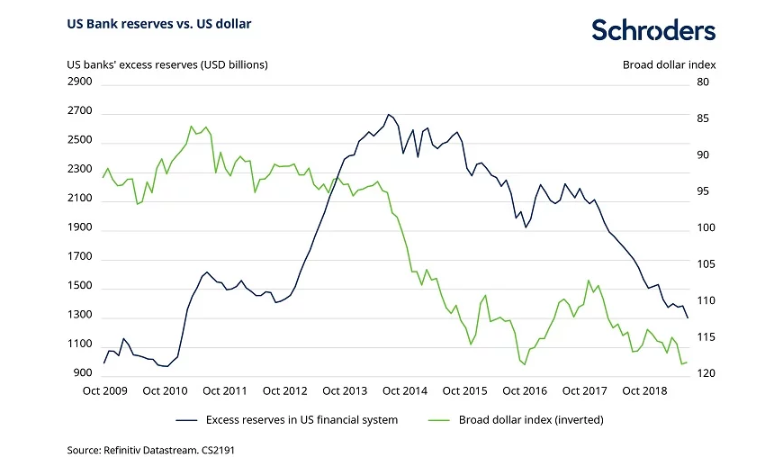

This month’s chart of the month (below) shows a global shortage of US dollars has emerged, shown in the left hand vertical axis in billions.

It has driven the dollar from strength to strength against other currencies for the last five years, according to the broad dollar index, show in the right-hand vertical axis and inverted.

However, this shortage of US dollars is being alleviated by the recent actions of the Federal Reserve (Fed), which could be the beginning of a fall from grace for the currency known as the greenback, as we explain below.

New rules after the financial crisis

The aftermath of the 2008 financial crisis saw a multitude of new rules and regulations for financial markets. The aim was to make sure such a damaging financial crisis could never happen again.

One of these new rules was that the US central bank would pay interest on the excess reserves (the ‘IOER’ rate) of banks.

Where do banks put their money? The concept of reserves and excess reserves

US banks are required to hold a ‘bank account’ at the country’s central bank in which they must deposit a minimum amount in order to conduct their business. This minimum amount requirement is called ‘Required Reserves’. Deposits at the Fed above this level are called ‘Excess Reserves’ and provide economists and investors alike with a useful barometer of the availability of US dollars in the financial system. Why is this useful? In principle the more excess reserves available, the more money banks feel comfortable lending out!

Quantitative easing increased the supply of US dollars…

Through the 2008-2015 era of quantitative easing (so-called QE) the Fed made large-scale purchases of bonds. In effect this created new money, delivering US dollars into the financial system and increasing their availability – most banks could in theory lend out more US dollars.

Economic growth improved markedly and the recovery in corporate earnings was reflected in the strong performance of US stocks.

…but once the policy stopped banks did not step up

These policies were wound down in recent years, reducing the supply of US dollars.

At the same time the behaviour of commercial banks has permanently changed. These institutions typically borrow money from each other and use safe assets such as US Treasuries to guarantee the loans (like a bank would ask for a deposit to guarantee purchase of a house).

Instead of using these securities to borrow money however, banks are displaying more conservative behaviour and keeping these safe assets locked down.

Less lending in the financial system means slower household and corporate expenditure alike, all else being equal.

The US needs more dollars…lower supply means higher prices

The end result is that not only is the Fed supplying fewer US dollars to the financial system, but commercial banks are also supplying fewer US dollars to each other.

The Federal Reserve to the rescue (again)

Smooth functioning of financial markets relies on the creation of credit and flow of liquidity. Commercial banks’ aversion to transforming safe assets into credit has impaired the flow of US dollar liquidity. That was displayed acutely in September by a sudden spike in the interest rates that banks charge each other for overnight loans. The Fed recognised the danger and stepped in to provide $250 billion worth of lending to financial markets.

Having made another interest rate cut at its recent October meeting, the Fed is acting to make lending easier for everyone.

September’s display of funding stress and the Fed’s reaction to provide liquidity could prove a catalyst for a reversal in the trend of falling excess reserves. As such, it could also be the start of a weaker phase for the US dollar.

- For more on the US economy and the global economic outlook visit schroders.com/insights and follow Schroders on twitter.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.