Why everyone’s talking about hydrogen

What is all the excitement about?

Renewable energy can and will decarbonise power generation. Renewable energy and batteries can and will decarbonise the automotive sector. But these technologies will not be as viable for aviation, shipping, commercial vehicles, steel or fertiliser manufacturing. In all of these vital industries it looks as though hydrogen will be needed, or at least that hydrogen will be one of the most viable solutions, for decarbonisation.

Hydrogen can be burnt in a combustion engine or boiler for transportation and heating; used to power a fuel cell for transportation or heating; or used as a reduction agent for iron to make steel. It can also be used as an energy storage agent by using excess solar energy in the summer to produce hydrogen, which can then be stored and converted back to electricity for use in the winter. All of these processes have zero or much lower CO2 emissions than current alternatives.

How much hydrogen will we need?

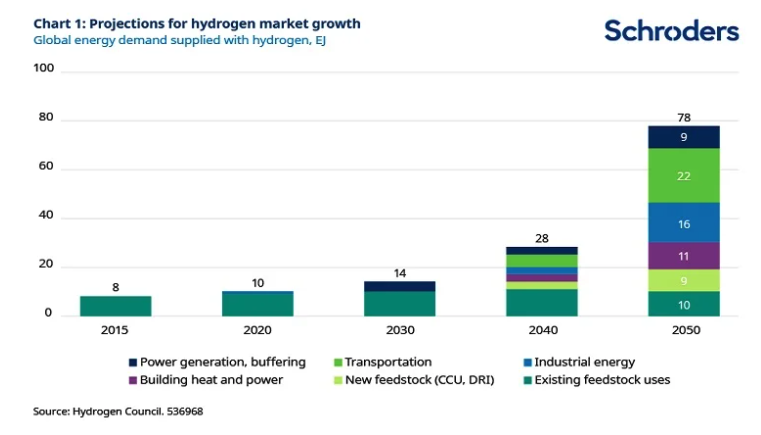

Hydrogen is already used in a few large scale industrial processes, such as oil refining ammonia and nitrogen fertiliser production. However, if hydrogen fulfils its potential in these new end markets of heating, industrial, transportation and energy storage, the production and consumption of hydrogen volumes would need to expand 7-10x from current levels. The chart below was produced by the Hydrogen Council, a consortium of industry and energy groups to highlight the potential market growth if all of the above use cases for hydrogen materialise.

Doesn’t hydrogen production create its own emissions?

Yes. 95% of existing hydrogen production is exceptionally polluting, being produced from natural gas (10kg CO2 per 1kg of hydrogen produced) or coal gasification (20kg of CO2 per 1kg of hydrogen produced). However, hydrogen can be produced CO2-free by electrolysis of water. If renewable energy is used to produce the electricity, the hydrogen can essentially be made CO2-free.

Discover more from Schroders:

– Learn: What is an impact bond?

– Read: Brexit deal: Three key takeaways

– Watch: What will the world look like in 2021?

What are the respective costs of these different production methods?

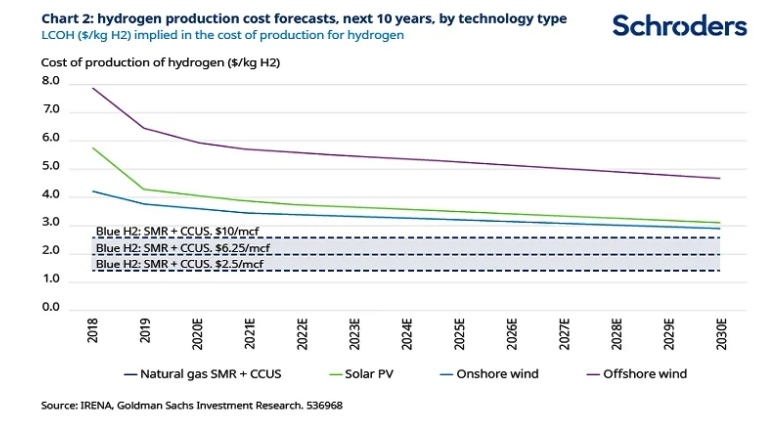

Today, renewable hydrogen is a lot more expensive than fossil fuel hydrogen. However, this is expected to change, and by 2030 renewable hydrogen should cross over and become the cheapest method of production, at which point there is really no need to persist with alternative production methods. The situation is very similar to where electric vehicles (EVs) and renewable energy itself were 5-10 years ago.

The chart below compares the costs of ‘blue’ hydrogen (made from natural gas) at different gas prices to renewable hydrogen. While very cheap gas with carbon capture and storage might still be slightly cheaper than solar produced hydrogen in 2030, the difference will be fairly small. There are also others who forecast renewable hydrogen costs to fall faster than this.

How big could the market for green hydrogen be?

This really depends on whether policy makers can be convinced by the natural gas industry that carbon capture and storage is a viable solution. In theory, making hydrogen from natural gas and then storing the CO2 underground could remain cost competitive with renewable produced hydrogen. However, currently no-one is really doing this at scale, and there are all sorts of legal and environmental problems with storing tens of billions of tonnes of CO2 underground.

The costs of renewable derived hydrogen are going to fall dramatically as shown above, driven by economies of scale and the ever falling costs of renewables, and this makes it quite likely, in our view, that green hydrogen will overwhelm fossil-derived hydrogen in 10 years’ time. Given that green hydrogen is only 1% of the hydrogen market today, the potential is huge. In a blue sky scenario, taking 100% share of a market that will be 8x larger means that green hydrogen production would be 800x larger than it is today in 2050!

What regulatory support is there for this transition?

The European Union (EU) is the furthest along in its planning for the transition to a zero emission economy, and it has recognised the need to develop a strong hydrogen industry to enable decarbonisation in industry, transport and heating. In July, the EU announced its hydrogen strategy, targeting at least 40GW of renewable hydrogen electrolysers and the production of 10mt of renewable hydrogen by 2030. The analysis anticipates the need for €24-42 billion of capital investment for electrolyser capacity up to 2030.

What will be the investment consequences of this transition?

There will, of course, be many investment consequences. There will be opportunities for energy companies and industrial engineering companies to build and operate all the new green hydrogen facilities. There will also need to be hundreds of gigawatts of new renewable energy capacity to supply electricity to the electrolysers, and these new renewable energy volumes are not yet built into market forecasts for the wind and solar industry suppliers.

However, perhaps the simplest business and investment opportunity will be the growth that comes to the companies that can capture the equipment market for all the new electrolysers that will be deployed. Electrolyser equipment sales are a truly tiny market today, at only approximately $250m revenues in 2020.

Building out the required scale of green hydrogen to decarbonise all these industries globally would require an annual electrolyser market of closer to $25 billion in the peak years of construction. In that context, the fact that there are only a handful of leading electrolyser players today makes this a very interesting industry, as while there could be some new entrants, the technology is not simple and the established players are rapidly forming alliances and customer relationships with developers and energy groups. This will give them economies of scale and help them drive down costs.

– For more visit Schroders insights and follow Schroders on twitter.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.