Why ‘Continual Learning’ is ready to disrupt investment

‘The only source of knowledge is experience’ – this quote, attributed to Albert Einstein, could be used to frustrate ambitious young analysts. The lesson? Grey hair will prevail. There simply is no substitute for experience in the investment business. Correct? Well, perhaps not any more.

A new technology might be about to give grey hair a pay cut. It’s one of the hottest threads of artificial intelligence (AI) research: continual learning (CL). CL enables machines to accumulate knowledge and learn how to apply that knowledge to make better decisions. It may prove to be the single most disruptive technology for investment management.

But how does this new technology compare with the old? Is it mature enough to use in a live investment process?

Human analysts and traditional quants – yes, quants – suffer from many behavioural biases. Perhaps the most fundamental are those that affect knowledge: what knowledge to accumulate and how to use that knowledge to guide investment decisions. Judgment, in other words.

But CL research challenges the primacy of human experience, potentially disrupting the businesses of traditional investment managers. We will get into the details, but first it’s helpful to demonstrate how a well-conceived AI investment strategy should work in practice.

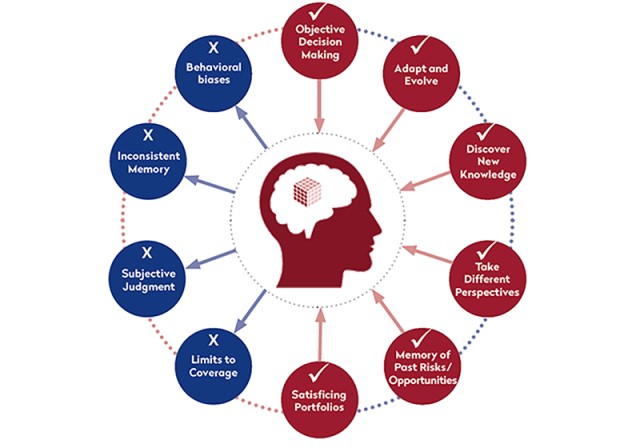

All fundamental investment methodologies should approach each investment decision from multiple perspectives, evolve as realities change, and provide understandable explanations for decisions. Both traditional (i.e. human analyst-driven) and AI-driven investment strategies should meet these criteria. But perhaps the chief advantages AI ought to have over traditional fundamental methods are objectivity and consistency. The graphic illustrates where AI-driven investment strategies should exceed their traditional fundamental investing counterparts (in blue). CL now extends these advantages to the objective accumulation and use of knowledge itself.

Which Type of Fundamental, Artificial Intelligence (AI) or Human?

Which Type of Fundamental, Artificial Intelligence (AI) or Human? (Source: Enterprising Investor)

While experienced investment managers may have subjective memories of past events, the best of them overcome these through discipline and the learned application of that knowledge — that is, good judgment. However, quant strategies, almost all of which rely on equity factor models, tend to suffer the worst of all worlds. These quant models have no explicit memory, and those who deploy them frequently dismiss exogenous causation because of their own confirmation biases. As soon as a market event leaves the sliding window used to train one of these models, it is forgotten. If we have nothing to learn from past crises and missed opportunities, we should stick with the traditional factor quant solutions of the 1990s.But this hardly makes sense in a world of vastly more and better data where AI offers a potential means to analyse that data.

At the Neural Information Processing Systems Conference (NeurIPS) in Canada in December, AI researchers presented cutting-edge innovations, and CL’s application to finance was an important part. A four-strong team from City, University of London presented a system that empowers machines to acquire knowledge and apply it to guide investment decisions.

This is called continual learning augmentation (CLA) – it is a new methodology, and its first application to financial markets. Leading AI researcher, Professor d’Avila Garcez, commented, “CL has been partially achieved in more sterile environments, but we believe this is the first time it has been successfully applied to the noisy, non-stationary real world of financial time-series.”

The system learns which events are worth remembering and which are best forgotten. This knowledge is selectively recalled to enhance stock-selection decisions.

The past decade or more of financial history was replayed, and the CLA system formed many important memories. The most interesting were of the lead-up to the subprime crisis, the ‘quant quake’, the post-quantitative easing (QE) era, and the (first) eurozone crisis. Models that appeared to best identify good (and bad) investments during these periods were stored as memories that could be recalled when events seemed to echo past ones. For example, the approach recalled the QE-driven recovery in 2009 and identified this knowledge as the most pertinent to apply in stock-selection decisions during another stimulus-driven stock market rally in China in 2017.

CL differs from ‘deep learning’ and other forms of AI, which tend to focus on isolated snapshots of information – for example, identifying faces on Facebook. It can be directed at a continuous stream of information from which it extracts knowledge over time.

CL is not new, of course. According to CL pioneer Danny Silver, research into CL began in the 1980s. Today, CL is moving so quickly that research must be checked on a weekly basis to keep abreast of developments.

Building investment knowledge over time used to be an exclusively human capability. No longer. AI as a driver of fundamental investing has come of age.

Few industries are more ripe for disruption than equities investment management in 2019. Crowded 1990s-era factor quant models are still in demand, while the recent explosion in high-quality data, coupled with the technology to make sense of it, has opened up new vistas. Things are changing fast, and the next generation of tech-fluent professionals coming into finance are poised to displace the grey hair and the outdated. Einstein may have been correct when he (supposedly) equated knowledge with experience. But did he anticipate his comments would apply to the machines of the future? The future is now.

If you liked this post, don’t forget to subscribe to the Enterprising Investor, where this article first appeared. It was written by Dan Philps, CFA.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice.