The top seven changes from Carney’s report

1 This is the first sign of tightening – or at least withdrawing stimulus – from the Bank of England since the crisis began, showing some parts of the economy heating up.

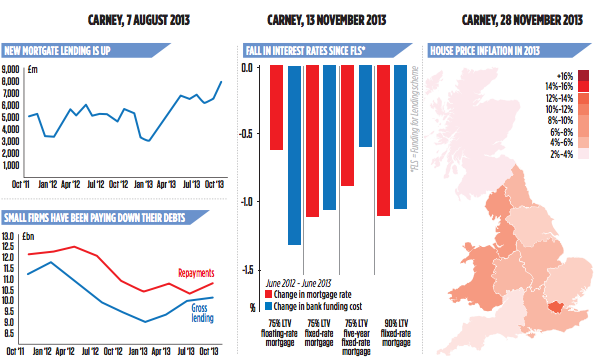

2 The Funding for Lending Scheme has been scrapped for mortgages. That means banks will no longer get access to cheap funding when they increase mortgage lending. The Bank and Treasury say this is because market funding conditions have improved and the support is no longer needed.

3 To make sure loans are not given away too easily, the Bank and the Financial Conduct Authority will look at tougher affordability criteria, testing borrowers’ incomes against a higher range of interest rates. This is a new macroprudential tool which Carney said is needed because underwriting standards have become too loose in previous housing booms.

4 Carney said he also has other tools to slow the housing market should it overheat and threaten financial stability, including limiting loan to value ratios and making banks hold more capital against mortgage loans.

5 The Bank has the power to recommend the government end the Help to Buy scheme, which aids buyers with small deposits. However, Carney said this is not yet a threat to financial stability.

6 Funding for Lending is still available for small business loans. For every extra £1 a bank lends to small firms, it gets access to another £5 in funding from the Bank of England, and the loans will not rack up capital requirements.

7 In addition the Bank of England’s Andy Haldane said he is looking at ways to create a market for securitised SME loans, a move which would enable banks to sell the loans on and so lend out more.

CARNEY’S DEVELOPING VIEW OF THE UK HOUSING MARKET

Valuations are still quite a bit off (pre-crisis peaks). They’ve started to recover, but they’re still quite a bit off, whether you measure them on a price to rent basis or relative to income. So the housing market is starting to recover, and actually the overall level of housing activity relative to GDP is a couple of percentage points lower than where it was prior to the crisis. So it needs to be put in context.

CARNEY, 7 AUGUST 2013

The Bank, through the financial policy committee, has been very vigilant about potential risks there. But we need to put the pick-up in housing activity in perspective. Activities levels, while they’ve picked up, are still running at between two thirds, or three quarters of historic averages in terms of whether it’s transactions, or approvals, home building. And so there is some room for that to further pick up and that’s the initial phase of this recovery.

CARNEY, 13 NOVEMBER 2013

Risks to financial stability may grow if there are further substantial and rapid increases in house prices and a further build-up of household indebtedness. These risks would be amplified if underwriting standards on mortgage lending were to weaken as has been the case in previous house price cycles. As part of a graduated response, the FPC is acting in concert with other authorities to implement a package of measures to guard against these risks.

CARNEY, 28 NOVEMBER 2013