How Martin Gilbert is poised to challenge the US giants

A painful experience in the past has helped Aberdeen Asset Management build for the future. Its CEO tells David Hellier how his latest deal can be a catalyst for US expansion

WHEN Martin Gilbert and his board first discussed the acquisition of Scottish Widows Investment Partnership (SWIP) from Lloyds last March, they turned the deal down.

The board met in Singapore, where Aberdeen Asset Management has a huge presence, and where Gilbert and his colleagues often get more time to discuss such things.

“We did not want to do another large acquisition, so the management and the board decided not to proceed with it,” Gilbert said.

That was then. By October, the mood music had changed. Aberdeen re-entered the fray, boosted by the prospect of Lloyds taking a stake in it, and now it is nearly the proud owner of SWIP (waiting just for regulatory approval), making it the sixth-largest listed asset management group in the world, and the biggest publicly traded group outside of the US.

Twelve years ago, things looked altogether different for Gilbert and the fund management giant he still runs. Aberdeen was at the wrong end of the split capital investment trust scandal, which resulted in a total of 50,000 investors losing an estimated £700m across the industry.

Investors had bought into two types of investment trusts, income split-caps, which gave both dividends and the hope of a capital growth, or capital split-caps, which paid investors a share in the trust’s capital growth.

In the event many of the trusts, some of which invested in each other, hit difficulties, leaving investors with heavy losses. Aberdeen’s shares fell 97 per cent and at its nadir the group was almost wiped out of existence. In the end it helped negotiate a £194m settlement, paying £75m itself into an industry-wide pot.

Gilbert says it was “great to get it over with”. “It was such a tough time. It almost bust us,” he says. “You’ve got to learn from your mistakes and there’s no doubt we came out of it a better company. It’s made us a lot more risk averse than we were.”

The next few years witnessed a series of deals, including the sale of a retail business to the well-known fund manager John Duffield at a time when the group was still reeling. “We shook hands and John stuck to his word, despite the fact I was under severe pressure.”

There followed a series of acquisitions that helped to take Aberdeen’s assets under management to £201bn, and propelled the group into the FTSE 100 by 2012.

The SWIP deal, which takes funds under management to £336bn, was introduced to Aberdeen by Tadhg Flood, the veteran Irish investment banker at Deutsche Bank. Flood came knocking on Gilbert’s door with news that Lloyds, which is preparing itself to come out of government hands, was willing to sell SWIP. Says Gilbert: “We had a group strategy which envisaged us doing a number of things, but part of it involved us growing in the US where 50 per cent of investable wealth is invested. That was the strategy.”

The lack of an obvious US element to SWIP put the board off initially but then it gradually dawned, says Gilbert, that a deal “would improve us, make us financially stronger and would take us to the size of one of the top 10 independent fund managers in the world”.

Aberdeen knew by this stage that Macquarie was interested, as was the Canadian bank RBC. The key, says Gilbert, was in offering Lloyds a stake in the combined business. “We thought we had the advantage in promoting a long-term relationship with Lloyds.”

Gilbert met the Lloyds chief executive Antonio Horto-Osorio a couple of times, a man he has known for some years, and offered him a 10 per cent stake in Aberdeen’s equity. The combination of cash and a stake in the business won the day for Aberdeen, resulting in a £550m deal.

“This deal is going to boost Aberdeen’s financial strength,” says Gilbert, who adds that it gives Aberdeen a 20 per cent rise in revenue in return for giving away 10 per cent of the group’s equity to Lloyds.

It also makes Aberdeen less reliant on its emerging markets business. At the moment global equities, emerging market equities and Asian equities make up 53 per cent of the group’s assets under management; this will go down to 32 per cent after the deal, as Aberdeen’s current asset portfolio becomes diluted by the more UK-oriented risk-averse SWIP portfolio.

Gilbert says there shouldn’t be too many job cuts after the deal. “There’s about £50m of synergies to be made from putting the two businesses together but the deal is not prefaced on cutting masses of jobs.”

Gilbert can at times be hot tempered, but he also quite obviously commands loyalty in spades from those he gets on with, and he generously returns their loyalty. He has assembled around him a group that have been together for years.

His four main lieutenants are Andrew Laing, deputy chief executive, Bill Rattray, finance director, Hugh Young, group head of equities and Ken Fry, chief operating officer.

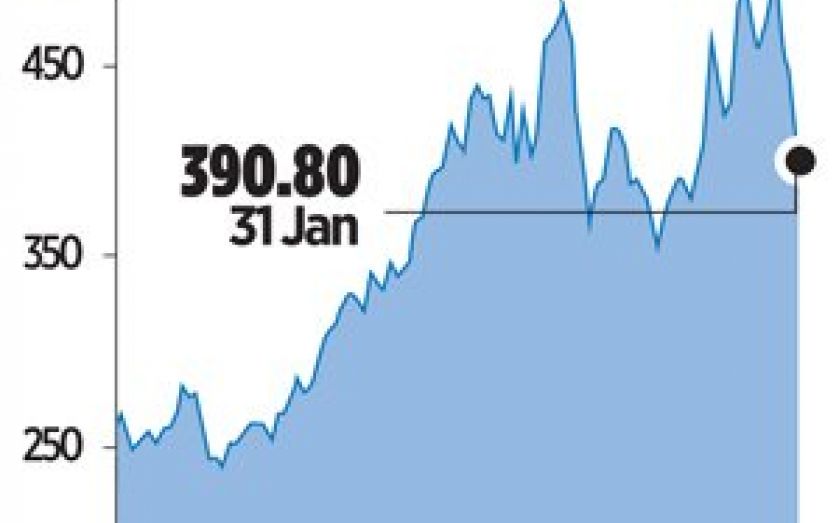

When the deal was finally clinched in November, as Macquarie pulled out of the bidding, Aberdeen’s shares strengthened and at one point traded close to 500p. In recent days, with financial markets concerned about the fortunes of the emerging markets, the shares have retreated to nearer the 400p level.

“We’ve been whacked by the emerging market volatilities but the nervousness is largely over currencies rather than the companies. In the long-term I think our investments are fine and actually valuations are looking attractive. However, markets could be a bit volatile for six to nine months.”

As the ink goes dry on his latest deal, Gilbert is already looking to grow further, probably in the US. “We regard ourselves as competing with the US funds,” he says.

And then there’s a note of caution, no doubt inspired in part by those dark days near the beginning of the century when he had to endure the anger of investors and MPs. “I try not to believe too much in my own publicity. I’m always looking for what could go wrong.”

CV MARTIN GILBERT

Born: 1955

Lives: London and Aberdeen

■ Educated at Robert Gordon College, Aberdeen and then at Aberdeen University

■ In 1993, he co-founded Aberdeen Asset Management

■ Sits on the board of BSkyB and on the Treasury’s Financial Services Trade and Investment Board, and on the Scottish Government’s Financial Services Advisory Board.

■ He was appointed Chairman of the Prudential Regulation Authority’s Practitioner Panel in December 2013.

■ His hobbies include golf, fishing, skiing and sailing