Big Tech’s market might in five charts

The largest US technology stocks – Apple, Microsoft, Amazon, Facebook and Google (Alphabet) – known as the “FAMAGs”, tumbled sharply at the beginning of this month, after supercharging the US stock market from the depths of the Covid-pandemic in March.

These “superstar” firms have largely benefitted from the economic fallout of the crisis, as more people rely on their technology to work and shop from home. However, their increasing dominance is raising concerns about the top-heavy composition of the US equity market and the sustainability of the tech rally.

Here are five charts that demonstrate the FAMAGs’ growing size and influence.

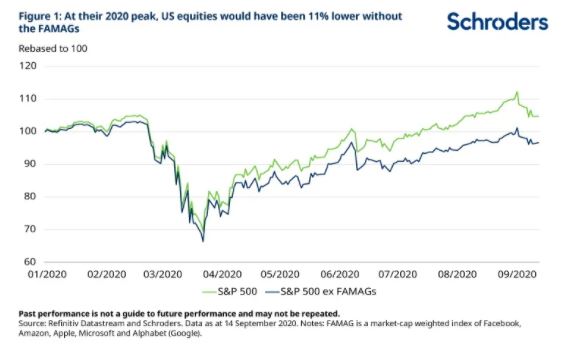

1. How Big Tech is propping up stock market returns

With Apple briefly becoming the first US company to be valued at US$2 trillion, more investors are turning their attention towards the impact of the tech sector on market returns.

As at 14 September, the S&P 500 was up 6 per cent this year, while the FAMAGs were collectively up 42 per cent.

If we exclude the tech giants, the index return drops to -2 per cent. In other words, US equities would be 8 per cent lower this year without the FAMAGs (or 11 per cent when measured at their peak on 2 September). This is how important these firms have become.

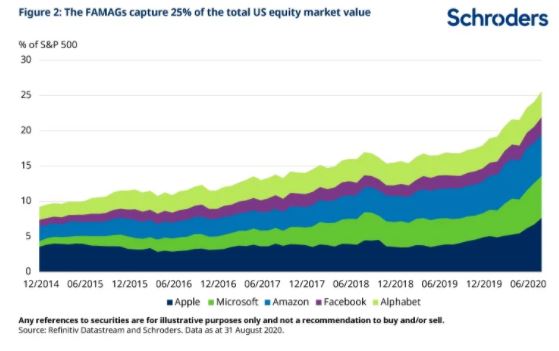

2. The US market is increasingly concentrated

One reason why these firms have become so influential is because they are the most heavily weighted stocks in the index.

Investors’ rush into tech this year has propelled the weight of the FAMAGs in the S&P 500 Index to a record high of 25 per cent, more than double their weight from five years ago.

This means that the performance of the FAMAGs will clearly impact the performance of the overall market more than a small cap company will.

To illustrate this, let’s suppose hypothetically that the FAMAGs collectively fell by 10 per cent. That would mean that all remaining 495 stocks in the S&P 500 would need to increase by at least 3.3 per cent just for the whole index level to stay the same.

Discover more:

– Learn: Would a Biden presidency hurt stock markets?

– Read: What’s driving stock market returns?

– Watch: Is Big Tech under threat?

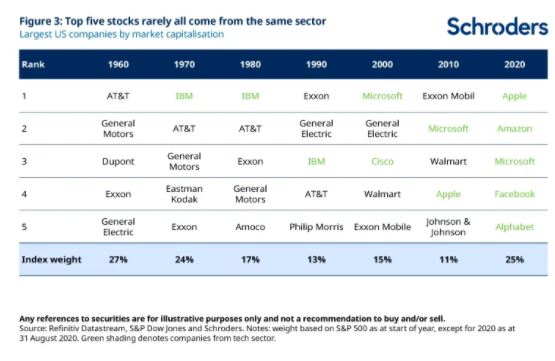

3. Unprecedented dominance of a single sector

The five largest members of the S&P 500 are now all from the tech sector. The last time the US equity market was as concentrated as this was back in the late 1960s. So it is not unusual for the market to be concentrated in a handful of stocks (see table). Although the extent of concentration at present is greater than normal, what is more unusual is for the top five stocks to be all from the same sector – tech.

This lack of sector diversification should not be taken lightly. Any pullback in tech sentiment can have an outsized impact on overall market moves, as was recently the case.

4. Big Tech’s dominance reflects the companies’ profits

So are stock market valuations ringing alarm bells? This is the question that confronted investors at the height of the dotcom bubble in 1999 before it burst.

However, comparisons between the 1999 dotcom and today are often oversimplified. They often ignore the fact that many of the fast-growing internet companies back then were not generating significant profits or cash flows.

In contrast, the current tech giants are highly profitable. They account for 15 per cent of trailing 12-month S&P 500 earnings and an even higher proportion of forecast earnings, e.g. 20 per cent of projected 2023 earnings. When benchmarked against their market cap weight of 23 per cent, which reflects all future earnings, their valuations no longer look as extreme.

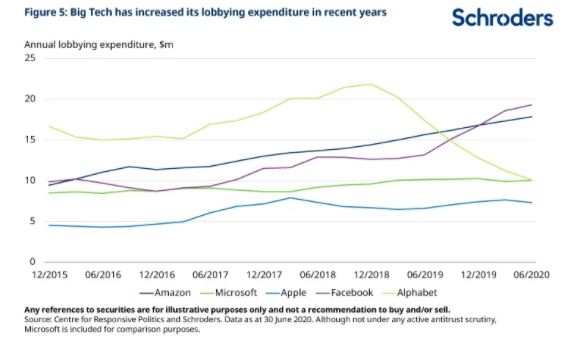

5. Big Tech has ramped up its political presence to protect its business interests

Faced with the threat of regulatory action to limit their market dominance, Amazon, Facebook, Apple and Alphabet’s Google are spending millions of dollars each year trying to influence regulators and politicians on policy issues ranging from data privacy to taxes.

For example, according to the Centre for Responsive Politics, Amazon and Facebook spent a record $17 million each in 2019. This was more than any other US company. This is not just a tech phenomenon, however. Academic studies show that corporate lobbying has been a key explanation for the decline in competition across numerous US industries.

In a recent Bloomberg interview, the chairman of the US House Antitrust panel, which is leading investigations into Amazon, Facebook, Apple and Alphabet’s Google, stated that these firms were abusing their market power to maintain their industry dominance. The chairman was critical of the government’s track record on policing anti-competitive behaviour, such as Facebook’s acquisition of Instagram.

Investors should stay on guard if decisive regulatory action is taken against the tech giants. Given their high benchmark weights, it could drag returns for the overall US market lower if confidence in them deteriorates for any reason. The closer a portfolio’s weights are to the benchmark, the bigger this risk. Passive strategies are most exposed.

Big tech has grown ever more influential, whether through index concentration, stock price performance, earnings generation, and money spent lobbying.

At a minimum, investors should at least be aware of the risk they are running in a portfolio, whether they are comfortable running those risks, and ideally, whether they are being rewarded for taking those risks.

Any references to stocks/companies are for illustrative purposes only and not a recommendation to buy and/or sell. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions. If you are unsure as to the suitability of any investment speak to a independent financial adviser.

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.