£100K isn’t a big salary – and we need to talk about it

He lives in a grotty flat, shops in Aldi, can barely afford a holiday and earns £100k. Meet Henry: a High Earner Not Rich Yet. He may not attract sympathy, but he’s a symptom a failing economy, says Eliza Filby

Nine out of ten Brits earning over £100,000 do not consider themselves wealthy. Maybe you are one of them, maybe you definitely aren’t (and find this statistic laughable) but, before you judge, meet Henry.

Back in 2019, Henry was a 28-year-old strategy consultant earning just over £50,000. He was full of optimism about his future. He’d been in the workforce for eight years and things seemed to be on the right track. He worked long hours, some weekends, but was secure that his career was gaining momentum. Fast-forward to 2025 and Henry, at 34, is now earning £103,500. His boss says he’s thriving. In wage terms, he’s made it to the six-figure mark, and all before his 40th birthday. So why does Henry feel like he’s been treading water these past six years? Why does homeownership (even outside London) feel out of reach?

Why is it impossible to save for anything, whether a house deposit or even holidays?

He may have a ‘big’ job, but he has not done the ‘big expensive things’ in life yet. He’s in a relationship, but they don’t live together, and kids aren’t on the cards anytime soon. And yet, he’s barely keeping up; he can hardly afford to attend all his friends’ weddings.

He’s on a six-figure salary, he’s hitting midlife, but that life feels precarious. That’s because, on paper, Henry’s made it. But in reality, Henry doesn’t feel secure for a very simple reason.

He may have had a £50k pay increase since 2019, but this has resulted in only a £6k increase in real disposable income – after accounting for inflation – not monthly, but yearly.

While his gross salary more than doubled, in real terms his disposable income only increased by about 27 per cent due to inflation and the rising cost of essentials.

This is the financial story of Henry; a man who should feel rich but doesn’t and how in today’s economy, six figures doesn’t stretch as far as it should.

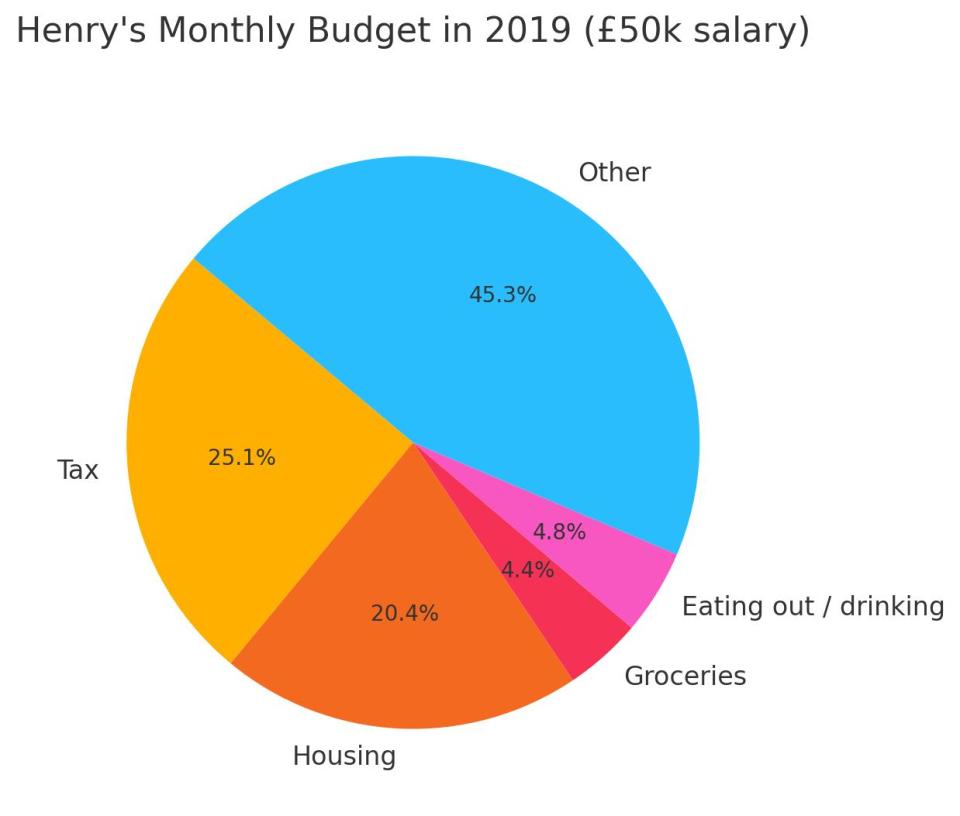

Back in 2019, Henry lived in London and paid £850 a month for a shared rental in Zone 2. It was relatively central and he saved money on commuting by cycling to work. He was also living in his mate’s parents’ buy-to-let, so the rent was reasonable. It was a fixed contract and bills were included.

Henry lived a frugal life for a 20-something in London, cooking four or five days at home. He was an Aldi man – spending £183 a month on groceries and only around £200 a month on eating out/beer money which, given a pint then cost around £5, he didn’t feel too guilty about. Monthly, Henry paid about £1,047 in tax and had a disposable income of around £1500. He saved a bit, mostly for travelling.

Henry got a promotion in 2019 and decided to look at moving out of his friend’s flat share. He was done having his mate as his landlord and effectively paying rent that would eventually be his mate’s house deposit or inheritance.

Covid lockdown then proved a decider. Henry had had enough working from his tiny room in a noisy flat share, he was also mindful that his life needed to feel less like living in a student dorm and more like the 30-something professional he was. The new place cost £1,650 a month – a stretch, but it felt like time.

The reality in 2025

Now, that same flat costs Henry £2,230 a month. His landlord passed on the mortgage rate hikes. Henry knows that a one-bedroom flat is a luxury, but it doesn’t feel like it. There’s mould, the landlord has barely touched the place in years, and while Henry would like to eventually move his girlfriend in, they’ve only been dating for six months. He is also aware of the chaos and cost of the London rental market right now.

Henry still shops at Aldi, but that same bill now costs £317 per month – a 73 per cent increase. He still likes to go out, but that Friday pub bill has increased by £100 a month. The average cost of a pint in London is nearly £7, much more than that near Henry’s office. Overall, his food bill has gone from £391 per month to £625 – a 60 per cent increase – just to eat and drink exactly as he used to. Between rent and food, costs have shifted from £1,241 a month to £2,855 a month.

Then there’s tax. Henry now pays £2,868 per month, nearly three times what he paid when his salary was £50k. In total, £34,420.60 of his annual salary goes on tax. So, in terms of disposable income, between 2019-2025, despite the £50k increase, Henry only sees an increase of £6k of real disposable annual income (adjusted for inflation).

Would things look different if Henry had kids? Maybe worse; he and his partner wouldn’t qualify for free childcare hours. We also didn’t factor in student loan payments or private pensions. Let’s assume Henry has no student debt thanks to parental help, but still can’t afford to contribute to a private pension beyond his workplace plan.

You could ask why Henry moved to his own flat. Maybe because he was under the illusion that he earned more money than he thought and was at a professional stage in life when he could make those kinds of decisions. You could ask why he didn’t leave London, but as a young professional that is a bold move – and if you work for one of the big consultancy firms, it would be challenging with recent return to office mandates. He could technically buy in a city like Leeds, where the average house price is £220,000 with a 10 per cent deposit (£22k) and a mortgage of around £1,157 a month, but would he still be earning that salary in Leeds? You could ask, why didn’t he spread the costs with his girlfriend? Possibly, but they’ve only been dating for six months.

The only way that many young professionals are managing these costs is by coupling up (Double Income, No Kids: DINKS), moving back home, or (like a lot of his friends) leaving the country.

Meet the Henrys

Henry belongs to a growing class: the High Earners Not Rich Yet – HENRYs. Coined by financial advisers, the term describes millennials in top tax brackets (from £65k up), disproportionately working in London, often highly educated yet struggling to feel economically secure.

According to The Economist, they account for five per cent of taxpayers but nearly half of all income tax receipts. And they represent a conversation we don’t want to have in Britain and which our politics (understandably) isn’t geared towards. After all, plenty of people are worse off than Henry.

The problem with Henrys is that most people assume they are rich, but they aren’t – certainly in terms of their expectations. They are the people for whom the public rarely has sympathy: highly paid professionals in banking, professional services and consultancy, disproportionately in London and often with access to the Bank of Mum and Dad. They are often least likely to talk about any of this publicly.

When he was Chancellor, Jeremy Hunt got into trouble when he claimed that £100k was “not a huge salary” for people in his constituency in Surrey. Many were outraged. But he wasn’t wrong – and now even high-paid NHS consultants are in dispute, arguing their real pay has fallen by 26 per cent since 2008. Relatively speaking, they are right. Look to America, where they see our professional salaries as laughable, and where Silicon Valley tech companies see jobs in the UK as ‘cheap offshoring’.

This speaks to the broader economic point here that we are a poor country, pretending to be a rich country. The truth is that years of stagnant growth, depressed wages, a dysfunctional housing market and low investment mean we are living in an era when the emerging middle class have struggled, the established middle have stagnated, and the working class have been hammered. Henrys are just one victim of that story; not the only victim, but a victim nonetheless.

And the point is, we need Henrys for our public services to function. Just as we need nurses, care workers and teachers. Around 60 per cent of all income tax revenue comes from the top 10 per cent of earners, up from 53.5 per cent in 2010/1 according to HMRC.

Those with the broadest shoulders should carry the greatest burden, but under current constraints, many Henrys are opting out: moving abroad, rejecting pay rises, dropping down to four days a week to avoid tax and qualify for childcare hours. I’ve heard from an NHS surgeon who is actively trying to work less in order to ensure he doesn’t find himself in a childcare tax trap. I’ve also heard from plenty of millennials working in different sectors whose lifestyle simply isn’t what they thought it would be. Their reactions include anger, surprise and resignation. The truth is, the country can’t afford the brain drain this state of affairs is already triggering, nor can we afford to have this cohort or take their foot off the gas. We need to talk seriously about income, not just at the bottom, but in the middle. And yes, at the top (and very top).

Of course £100k isn’t a small salary. But in today’s Britain, it doesn’t buy what it used to and the resentment is reaching a tipping point.

This isn’t about class war. It’s not about saying £100k is poverty. It’s about recognising that the rewards for work, including well-paid work, are shrinking in real terms.

The one thing that saves many Henrys? The Bank of Mum and Dad. Or a partner. Otherwise, six figures is not enough to stand still, let alone progress at the rate people had not unreasonably expected. We need a new conversation, not just about inequality but the shape of middle-class life. Because the old model under new economic conditions is creaking.

And Henry? He’s the canary in the coal mine.

Eliza Filby is the author of Inheritocracy: The Bank of Mum and Dad