What the analysts are saying about Chinese rebalancing and trade data

What does this morning’s narrowing of China’s trade surplus and boost in imports and exports mean for the economy?

This morning, it was revealed that China’s trade balance narrowed much more drastically than expected in July – to $17.818bn from $27.100bn (a fall to $26.200bn had been forecast). At the same time, Chinese imports rose at an annual rate of 10.9 per cent and exports 5.1 per cent (from respective falls of 0.7 per cent and 3.1 per cent the month before).

The results sent FTSE 100 miners surging this morning, with Antofagasta and Glencore Xstrata up around 2.7 per cent, and Anglo American up over three per cent.

Christian Schulz, senior economist at Berenberg Bank, says the data is in line with the goal of China’s managed slowdown – to shift the growth model away from export- and investment-led growth towards consumption.

Over time this should lead to rising imports and a falling trade surplus. While monthly trade data can be volatile and its quality has been in doubt, the July data certainly does not contradict the rebalancing story. We expect tomorrow’s data release for July retail sales, industrial production and investment to provide further evidence of progress as retail sales growth should stay strong.

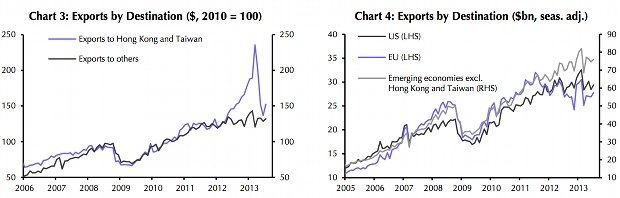

Qinwei Wang, China economist at Capital Economics, adds that the growth in exports shows foreign demand is recovering, particularly in Hong Kong and Taiwan, while the import data provides further evidence investment is picking up following the strong expansion of credit over the past year.

The upshot is that the underlying state of foreign demand looks slightly better than a couple of months ago. Indeed, the components for new export orders from China’s two manufacturing PMI surveys both rebounded last month, though they remain below 50. Note too that exports from other parts of Asia also picked up last month.

The rebound in imports was much larger than that of exports…. Nearly one-third of the increase was contributed by imports for processing and re-export. This is consistent with the idea that export demand is recovering.

However, the rebalancing of the economy away from investment could mean the pick-up in commodity imports will not be sustained, which could mean a bigger trade surplus later on.

But imports for domestic use also rebounded. Commodity imports (in volume terms) were especially strong and support other evidence pointing to a rebound in investment. This may suggest that the rapid expansion of credit over the past year is finally passing through to the real economy. That being said, given government efforts to rebalance the economy away from investment, we doubt that the pick-up in commodity imports will be sustained.

Finally, China’s trade surplus edged down last month, but at $17.8bn remains large. And if we are right in thinking that the recent pick-up in commodity imports is unlikely to last, the surplus is likely to rise further over the next year or so.