Treasury insists Britons benefiting from growth

THE TREASURY insisted yesterday that compensation for workers in the UK is still closely linked to output, adding to debate over the cost of living in the lead up to the Autumn Statement.

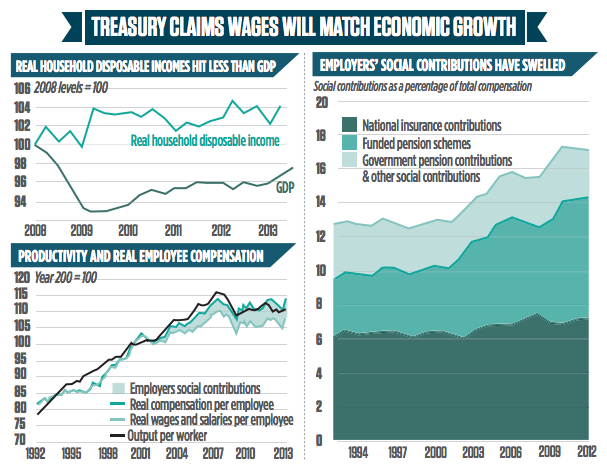

A new paper seen by City A.M. yesterday suggests that in the years since the crisis, the share of output going to workers’ remuneration has actually increased, and that this can be explained by the rising level of employers’ social contributions.

These contributions have ballooned in recent years, climbing upward from 13 per cent of an employee’s social contributions in 2000 to 17.2 per cent during 2012, according to the Treasury’s economists.

The value of pension and national insurance contributions from employers almost doubled between 1997, when the Labour party entered office, to 2010, according to the paper.

However, the Treasury also says that these contributions sometimes increased for reasons other than new government policy: as some private sector pension schemes closed from the 1990s onwards, costs were placed on employers, and a fall in bond yields around the world put pressure on pension funds.

The analysis goes further, saying that real household disposable incomes have risen 3.9 per cent from their pre-crisis peak, while GDP recorded a 3.3 per cent decline.

The Treasury believe that its analysis of the cost of living crisis is reinforced, citing research on the link between wages and productivity authored by economists Joao Paulo Pessoa and John Van Reenen.