Socially responsible investing and performance: a long-term winner

Companies with stronger ESG ratings outperform, particularly in times of crisis, as we witnessed during 2020, says Coline Pavot, La Financière de l’Echiquier (LFDE)’s head of responsible investment research.

Companies that rank well according to environmental, social and governance (ESG) criteria tend to outperform the average and have greater resistance to crises.

This was confirmed by our latest study, which reviewed and compared performances during an 11-year period (from January 2010 to December 2020), of mock asset portfolios compiled according to a single criterion: the ESG ratings of more than 750 companies.

We put together portfolios of European stocks, then attempted to distinguish between the performance of two opposite portfolios: the 40 best ESG-rated stocks in our database (‘TOP 40’) and the 40 worst-rated (‘FLOP 40’). We built up two model portfolios in line with our traditional equity funds and our high-conviction management. In addition, we conducted similar analyses on portfolios composed of the best and worst rated stocks on ESG criteria separately.

These portfolios have been rebalanced regularly, annually between 2010 and 2015, and quarterly from 2016. The ratings used were never older than three years. We considered that any older rating would be insufficiently up-to-date.

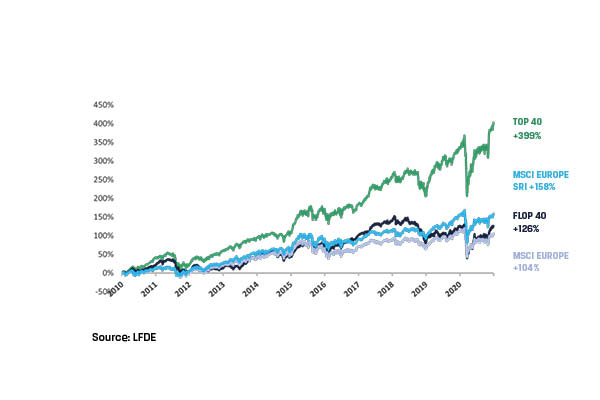

Our ‘TOP 40’ beats our ‘FLOP 40’

Investing systematically in companies with the highest ESG scores delivers a stronger performance in the long term than investing in companies with poor scores or in comparison to the main stock market indices.

Over 11 years, the portfolio with the best ESG ratings in our investment universe (TOP 40) delivered performance that was 3.2 times greater than the portfolio with the worst ESG ratings (FLOP 40), while over a nine-year period it was 2.3 times greater.

Over 11 years, the risk/return ratio of the portfolio with the best ESG ratings was 1.9 times greater than the portfolio with the worst ratings, while over a nine-year period it was 1.6 times greater. The further increase in outperformance did not involve higher volatility.

Examining ‘E’, ‘S’ and ‘G’ individually

When assessed separately, strong ‘E’, ‘S’ and ‘G’ performance also inspire better long-term performance.

In fact, over the past 11 years the performance of the mock portfolios composed of the best Social ratings (+362%), the best Governance ratings (+262%) and the best Environmental ratings (+233%) has been superior to those composed of the worst Environmental ratings, the worst Social ratings and the worst Governance ratings (with the best of these three categories coming out to +185%).

However, of all our mock portfolios, the one that created the most value over 11 years remains the TOP 40 (+399%). The portfolio made up of the worst Governance ratings displayed the worst performance for the period (+120%).

In respect of potential biases in our portfolios, even if there is an overweighting of portfolios based on growth management and/or small caps, the corresponding indexes are beaten over the long term.

There is also a certain selection bias as before a stock can be rated it needs to be pre-selected by a member of LFDE’s portfolio management team. This may explain the good overall performance of all the mock portfolios. Nevertheless, the portfolios of companies with the best ESG scores beat the portfolios of companies with poorer scores over the long term, even though the latter benefit from the same selection bias.

Another look to confirm our findings

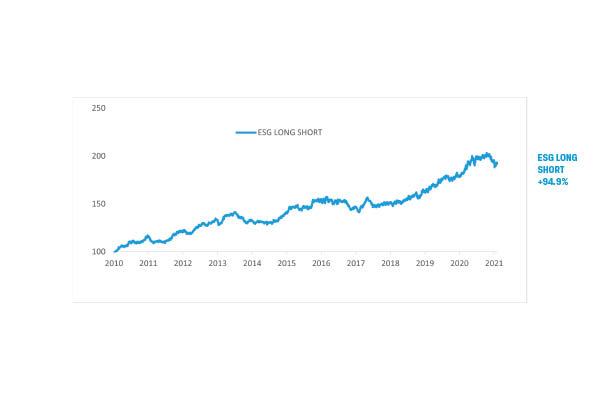

To reinforce our confidence in the results, we also tested our hypothesis using a long/short portfolio featuring the 750 companies of our database using solely the ESG ratings.

The ‘long’ compartment was composed of companies with the highest ESG ratings (higher than the average of our rated universe) and the ‘short’ compartment was composed of companies with the lowest ESG ratings. The balance of companies within the compartments was proportional to their ESG rating. According to our hypothesis, regardless of whether we are in a bull or bear market, if the best-rated companies on ESG criteria performed relatively better than the worst-rated companies, then the performance of the long/short portfolio will be positive and will demonstrate the relevance of the ESG rating factor in explaining performance.

So, what did we find? We observed that the long/short portfolio had a positive performance of +94.9% between 2010 and 2020, demonstrating the outperformance of the compartment composed of the best ESG ratings (long) over the one composed of the worst (short). Consequently, we can state that the integration of ESG criteria is a long-term performance factor. We have also observed that the long compartment outperformed the short for nine years out of the 11 analysed, which confirms our belief that socially responsible investing (SRI) improves performance in different market conditions. This was particularly the case in 2020, a year of global health crisis, where the long/short portfolio displayed a performance of +9.5%.

ESG heroes are better performers

On the basis of our research, we would assert that the outperformance of portfolios made up of stocks with the best ESG ratings is significant and robust over the long term.

Portfolios made up of good ESG scores had similar levels of risk to the bad ESG scores and not far off the risk levels of the indices. Risk/return was nevertheless more favourable for the portfolios of good ESG ratings, whose ratios were boosted by their strong performances.

Even where there is an overweight to growth-focused management and/or small capitalisation stocks, the portfolios still outperformed their benchmarks over the long term.

Overall, there seems to be an intrinsic performance boost from taking ESG criteria into account.

If you liked this post, don’t forget to subscribe to the Professional Investor Blog.

By Coline Pavot, Head of Responsible Investment Research at La Financière de l’Echiquier (LFDE).

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.