Recession, interest rates and inflation: Five graphs that explain the UK economy

It feels like the economy decisively turned a corner this week, and its not just because the sun came out (although that probably helped).

Figures out this morning confirmed the economy was no longer in recession. Economists had suspected this might be the case from the moment a recession was confirmed, but this morning’s growth figures were significantly better than anticipated.

The Bank of England also took another step towards cutting interest rates, with a summer rate cut a virtual certainty.

So where does the UK economy stand after another busy week?

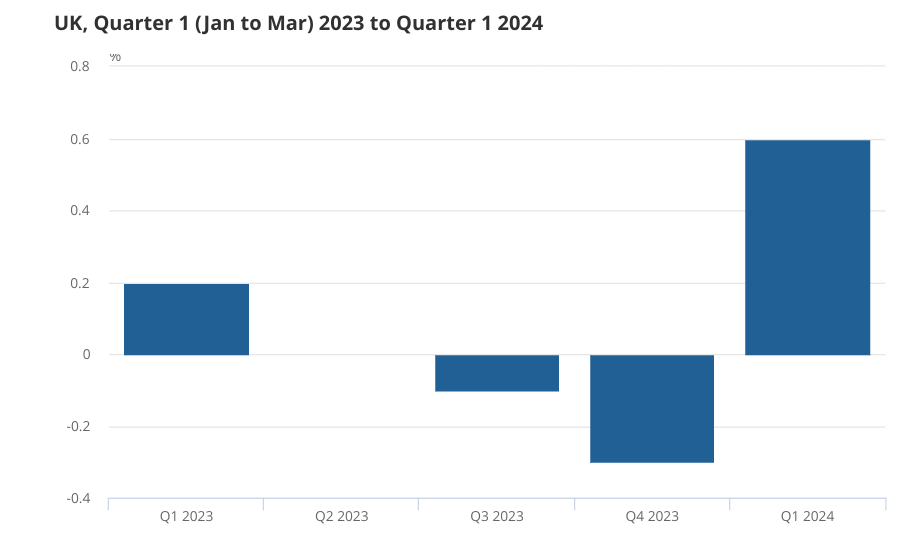

GDP

The UK leapt out of recession, with GDP growing by a relatively impressive 0.6 per cent in the first quarter of the year.

A look over the longer term shows there’s still real challenges for the UK. The economy has never recovered to its trend growth rate before the financial crisis and since the pandemic it has barely grown at all.

Look closely at the end of the graph though and you can see a marked pick up which, if sustained, would put the UK back on its pre-Covid trend growth path.

GDP per head

GDP per capita figures – a country’s GDP divided by its total population – are even more important than basic GDP. At last, the signs there are positive too.

After seven consecutive quarters of falling per capita growth, it turned positive in the first quarter of this year, growing 0.4 per cent.

GDP per capita is generally seen as a better proxy for living standards than GDP. The stagnation in GDP per capita over the past couple of years suggests that what growth there has been, was driven by a bigger population rather than an improvement in the underlying performance of the economy.

PMI

There’s no doubting the UK performed well in the first quarter, the big question is whether this will continue.

Recent survey data suggests the economy retains strong underlying momentum. S&P’s April purchasing managers’ index (PMI), for example, showed business activity at its strongest level for a year.

PMIs are seen as fairly reliable forward indicators of GDP growth. April’s reading of 54.1 was actually an acceleration on March and is consistent with a quarterly growth rate of around 0.4 per cent.

Inflation

The biggest factor driving the improvement in growth is lower inflation, which has given a boost to household spending. Having peaked at over 11 per cent in autumn 2022, inflation fell to 3.2 per cent in March.

The Bank of England expects inflation to fall to around two per cent when April’s figures are released in two weeks, largely thanks to lower energy prices.

There will be a slight rise in inflation over the second half of the year, but inflation is forecast to return to the two per cent target sustainably in early 2026.

Interest rates

Lower inflation will pave the way for interest rate cuts. Although the Bank of England voted to maintain interest rates this week, the accompanying forecasts and communications were dovish.

Speaking after the decision, Andrew Bailey said: “Its likely that we will need to cut Bank Rate over the coming quarters…possibly more so than currently priced into market rates”.

Following the press conference, markets moved to fully price in an August rate cut and thought a June cut was 50/50. The Bank Rate currently stands at 5.25 per cent after a rapid burst of rate hikes in 2022 and 2023.