Profits at Rio Tinto jump on high demand

Bid target miner Rio Tinto posted a better-than-expected 55 per cent rise in first-half profit yesterday, boosted by its takeover of aluminium producer Alcan and strong Asian demand for commodities.

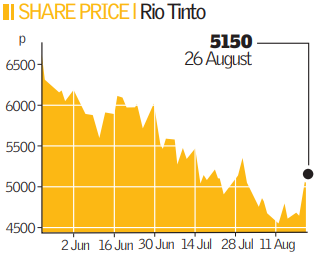

The company, which bought Canada’s Alcan, for $38bn (£19bn) just over a year ago, said its pre-tax profit to the end of June rose to $9.6bn compared to a year ago. Rio, led by chief executive Tom Albanese, is defending itself against a $150bn takeover bid from bigger rival BHP. The deal is awaiting clearance from Australia’s competition watchdog, due in October, and from the European Commission, in December, before formally launching its offer.

BHP said it will offer 3.4 shares for each Rio share. Rio has rejected this offer as undervaluing the firm.

Rio chairman Paul Skinner said: “The group’s performance in the first half, together with our growth potential, supports the boards’ view that Rio Tinto presents a very strong standalone value proposition for shareholders.”

The Australian government has signalled concerns that combining the two giants would lead to higher iron ore prices, which would hurt Australian steelmakers. The Chinese have also voiced the same fears.

And last week the Australian government cleared the way for Chinese state-owned aluminium giant Chinalco to raise its stake in Rio Tinto to 14.99 per cent, or 11 per cent of the dual-listed group as a whole.

Rio Tinto attributed its strong growth to high demand for commodities, in particular from China.

Analysts Views: Will Rio Tinto’s strong first-half results be enough to keep the firm independent?

Tom Gildley-Kitchen (Charles Stanley): “If the results had been bad, they would have counted against Rio in its bid to remain independent. Rio has been making quite a good case to remain a standalone business, and this fits into the case it has been making since BHP Billiton announced its bid last year. But ultimately the independence of Rio depends on how much the board at BHP are prepared to pay for it. For the last two weeks the share prices of both firms have been tracking each other, so little has changed.”

Jane Coffey (Royal London Asset Management): “The results were pretty good across the board, despite the market reaction sending shares down across this sector because of fears of a global commodities slowdown. But these results do a great deal to strengthen Rio’s argument that BHP should pay a bit more for the business. And let me make it clear that we see it that way around, rather than Rio remaining as an independent company. They are complementary businesses and a merger should go ahead.”

Michael Starke (Edison): “The results of both companies have been good recently, and their share prices relative to each other have been stable. If Rio’s had been good, and BHP’s bad that would have put pressure on BHP’s bid. But BHP may have to work a little harder to keep its bid on track anyway, because the commodity bubble may have burst and investors will want to see which is the best run firm. There will be a lot of pressure on commodity prices this year compared to last year.”