The Brexit unknown: how the votes moved markets – and what next

British politics has faced a turbulent week: three nights of Brexit votes, a Spring Statement and a downgrade to economic growth.

Market prices have swung on each twist as investors attempt to digest a constantly shifting set of possible outcomes. The single constant factor is uncertainty. With the scheduled exit date of 29 March looming, key questions have risen to the fore: will the date of departure be extended (which would require the agreement of the other EU nations)? Or could Article 50 – Britain’s formal notice of exit – be revoked (something the UK can do unilaterally)? Will the UK leave the European Union at all? Or will it leave with no deal and no transition period in place?

First we set out each event and the market reaction that followed. Then, below, a range of Schroders experts offer their take on the week’s extraordinary events – and look ahead to the emerging range of outcomes.

This week’s Brexit votes:

- Brexit vote night no.1 – withdrawal agreement: On Tuesday night, MPs voted down Theresa May’s withdrawal agreement – the second defeat. The 149 majority (391 vs 242) was greater than had been expected – but significantly narrower than the 230 majority in the previous vote.

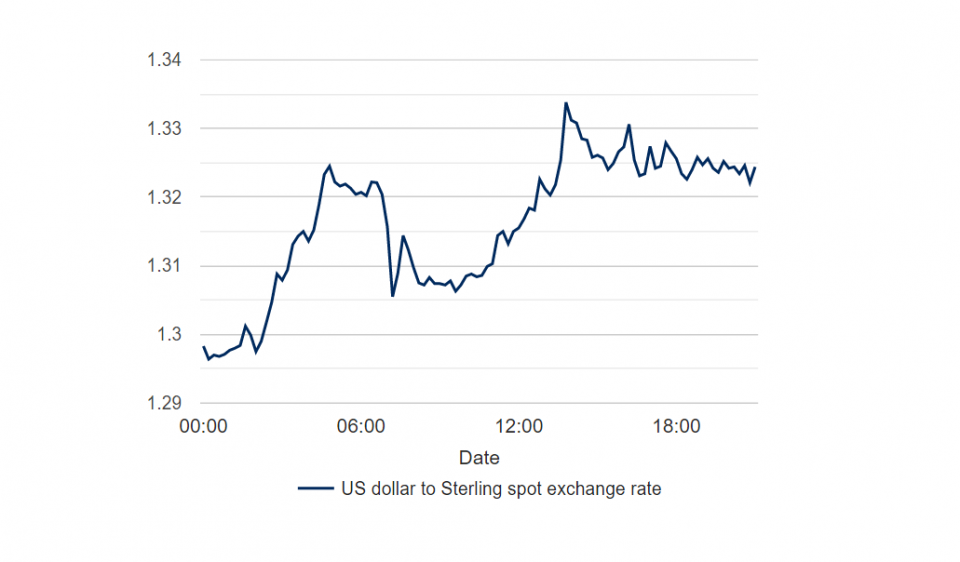

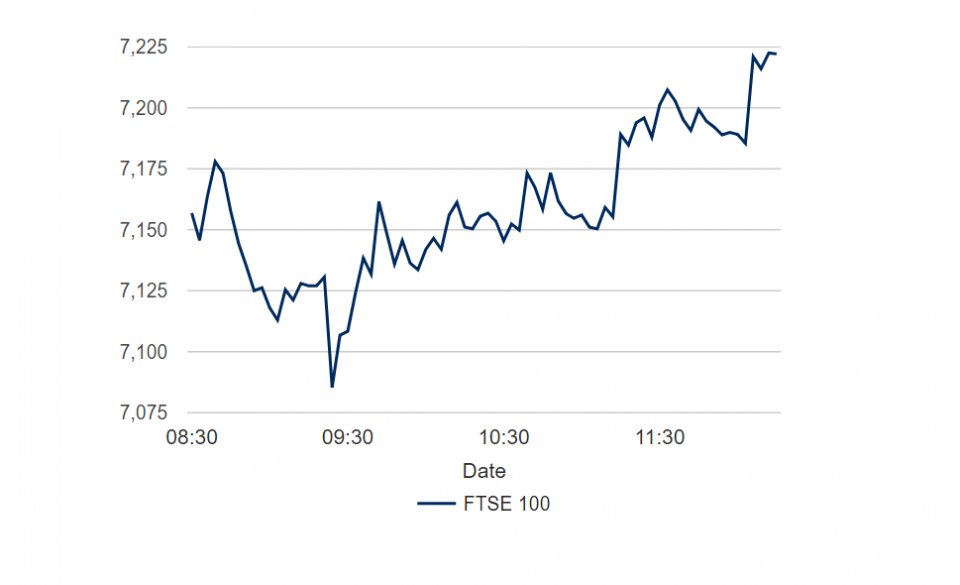

The reaction: Sterling had enjoyed a recovery after the January Brexit vote, surpassing $1.33 at the end of February. It had waned in recent weeks and saw further turbulence on Tuesday, falling from $1.324 to $1.308. The FTSE 100 rose from 7131 to 7151 points during trading ahead of the vote. This was largely related to the fall in the pound: falls in sterling improve the profitability of FTSE 100 companies when overseas earnings are converted into pounds. - Brexit vote night no.2: On Wednesday night, MPs narrowly voted that no-deal should not be permitted under any circumstances. The amended motion was decided on a majority of 321 to 278.

The reaction: Sterling rose throughout the day in anticipation of the results but gave up some of the gains once the outcome was known, up $1.323 from $1.308 on the day. The FTSE 100’s reaction was more ambivalent, as shown in the middle section of the second chart.

Sterling performance from Monday to Friday

Source: Refinitiv, 15 March 2019. Chart shows data from 00:00 on 11 March to 09:00 on 15 March.

FTSE 100 performance from Monday to Friday

Source: Refinitiv, 15 March 2019. Chart shows data from 08:30 on 11 March to 08:30 on 15 March. This material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Past performance is not a guide to future returns and may not be repeated.

Next:

- Brexit vote night no.3: MPs voted 412 to 202 in favour of applying to the EU next week for a short delay in Brexit which applies only if MPs finally endorse the Prime Minister's exit deal at the third time of asking next Tuesday.

Reaction: The pound was largely unmoved by the news, holding at around $1.32. The FTSE 100 rose by around 0.5% in early trading on Friday.

Amid this flurry of Brexit developments, Wednesday also saw the Chancellor of the Exchequer, Philip Hammond, deliver the Spring Statement, which focuses on the UK economy and government finances.

The Office for Budget Responsibility (OBR), the independent watchdog, downgraded its forecast for growth in 2019 to 1.2 per cent from 1.6 per cent in October. It maintained its forecast of 1.4 per cent growth in 2020 and revised up its forecast for 2021 to 1.6 per cent from 1.4 per cent in October.

Azad Zangana, Senior European Economist, said: “The outlook is simply too uncertain to read too much into the current forecasts and plans. The Chancellor was at pains to stress that Brexit uncertainty must be lifted to help boost the economy. He even published a list of tariff schedules that would apply if there is a no-deal Brexit. Of course, there is no guarantee that he would be in his post to push them through in a few months time.”

Brexit and the economy

The Schroders Economics Group recently lowered forecasts for UK economic growth highlighting that the delay had already done some “irreversible damage”.

The estimate for real GDP growth for 2019 was reduced from 1.4 per cent to 1.1 per cent. The forecast for 2020 was left unchanged at 1.5 per cent. This scenario is based on growth in investment and household spending from the second half of the year, which should last well into 2020.

The group also pushed back its expectation for a rise in interest rates to 1 per cent from May to August.

Keith Wade, Chief Economist, said: “Our view on the Brexit outcome has not changed as a result of the votes in parliament this week. The odds on a damaging no deal have risen, but we still see the most likely outcome as being a deal with a transition period allowing the economy to recover as the ‘cloud of uncertainty’ is lifted.

“For some time we have taken the view that a deal would be done at the last minute as has been the EU’s modus operandi in past crises. In this way they can obtain maximum leverage as the clock ticks toward midnight on 29 March. Clearly, any deal would have to contain a legally binding agreement that the UK would not be locked into the EU by default as a result of arrangements for the Irish border. Such an agreement is not impossible to imagine, but the EU is likely to demand a price, probably extra contributions to the budget or possibly on areas like future fishing rights.

“That said once agreed there would still be a delay as any deal would have to go back to parliament for approval and would then have to be ratified by the EU27. There is also the need for parliament to pass a massive amount of legislation before the country can depart.”

Brexit and the UK stock market

Brexit concerns have left UK stock markets unloved and, on some measures, undervalued. When comparing share prices with earnings, a key measure of value, the UK market registers 14.1. This is 12 per cent below the 20-year average and compares with 19.9 for the US and 15.2 for Europe. (All figures based on MSCI data, 14 March 2019).

Income yield is also attractive with the UK market currently paying 4.7 per cent compared to 3.7 per cent for Europe, 2.9 per cent for Asia Pacific and 2 per cent for the US.

Sue Noffke, Fund Manager, UK Equities, said: “Uncertainty about the UK’s relationship with the EU has left many international investors nervous about investing in UK equities. A recent poll showed that UK stocks were the least popular asset class among global fund managers.

“While it is understandable to fear uncertainty, we embrace it since uncertainty creates the mis-priced opportunities in markets that we look to exploit. Some of the most attractive opportunities are among companies whose businesses are most exposed to the domestic consumer such as housebuilders and hotel and leisure companies.

“Of the larger companies listed on the UK stock market, many derive a significant portion of their earnings from overseas. The prospects for these businesses are determined by wider global factors – and we’d say those prospects appear fundamentally sound whatever happens in the context of Brexit.”

Brexit: what next?

Caspar Rock, Chief Investment Officer, Wealth Management, said: “A day is a long time in politics and we still have 14 to go.

“MPs have indicated they don’t want a no-deal, and tonight they may vote to extend the Brexit date. That’s not a given, because EU countries need to agree to an extension and they’ll demand a rationale for doing so – such as Theresa May backing down on some of her red lines, or the calling of a referendum.

“One outcome that’s looking increasingly likely is that the Prime Minister will put her deal to parliament again.

“As the deadline nears she’s cornering MPs by reducing their range of options. Brexiteers may increasingly fear a revocation of Article 50, a second referendum or no Brexit at all, while Remainers will be pressured by the fact that a no-deal could still arise.

“It might be a case of the government losing many battles to win the war. Theresa May has already reduced the margin of opposition to her deal and she may now slog onward to reach a majority, however close that takes us to the 29th.”

- For more views on Brexit from Schroders visit the Brexit hub.

Important Information: The views and opinions contained herein are of those named in the article and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 1 London Wall Place, London, EC2Y 5AU. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.