Bitcoin crashes below $200: Here’s what you need to know

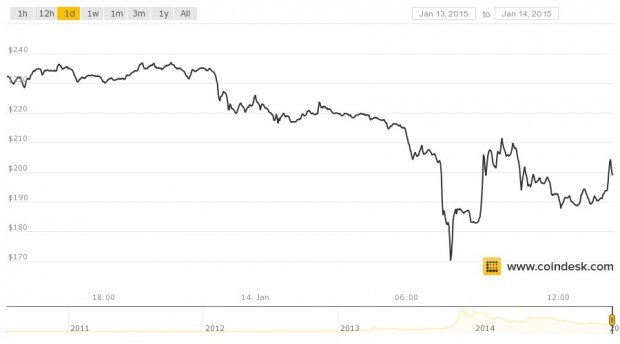

The price of cryptocurrency Bitcoin has fallen through the floor, touching lows of $173. The troubled digital currency has lost 30 per cent of its value in just two days.

Bitcoin has suffered something of a fall from grace after reaching highs of $1,000 and winning a host of fans among businesses and entrepreneurs. A key point in the selloff was when Bitcoin fell through the $250 mark yesterday, seen by many industry experts as an important barrier, according to Coindesk.

Sell orders have been flooding into major Bitcoin exchanges like Bitstamp. Bitcoin's market capitalisation is now down to below $3bn, a huge fall from $13bn in 2013. If things continue at this rate Bitcoin could be in the running to again be dubbed the worst investment of the year.

Bitcoin got off to a bad start this year after Bitstamp was hacked and 19,000 Bitcoins, equivalent to just under $5m at the time, were lost. After the disastrous Mt Gox hack and Bitcoin's possibly unfair association in the public mind with crime, the digital currency's image problem isn't getting any better.

But more importantly, Bitcoin's structure of mining is becoming increasingly difficult to sustain. As a system, Bitcoin requires competition from Bitcoin “miners”, who validate transactions blocks in their search for new Bitcoins.

Whoever validates the most recent transactions block is rewarded with Bitcoins. The process is designed so mining Bitcoins gets more difficult as time goes on – meaning that as the cryptocurrency's value falls, it becomes difficult for many miners to stay in business. It has been argued that the industry itself is a natural monopoly, and its collapse is inevitable. Mining service CEX.io announced on Monday that it would be suspending its activities.

Bitcoin is decentralised and peer-to-peer, unbacked by any central bank. Those who criticised Bitcoin's massive spikes over the past couple of years may have reason to feel vindicated.