Investment opportunities despite stubborn inflation

It is not just equities that are providing real growth for investors

INFLATION remains static at 2.7 per cent on the consumer price index, the 46th month it has sat stubbornly above the Bank of England’s 2 per cent target. Coupled with historically low interest rates, this has led millions to turn to bond, equity income and commercial property funds. It’s hardly surprising. Recent research from JP Morgan found that, in 2007, the annual income from a £100,000 investment in a one-year bank deposit was £5,700. Today, it is a fraction of that amount.

Of the 853 ISA and non-ISA accounts currently on the market, only eight savings accounts negate the effects of tax and inflation (if you’re a basic rate taxpayer). According to Which?, AA offers the best instant-access savings account, with a 1.6 per cent annual equivalent rate and a 1.1 per cent bonus rate. This is merely treading water, however. Where can you look for growth?

THE FIRST PORT-OF-CALL

A diversified portfolio is obviously essential. JP Morgan research analysed the performance of a portfolio invested 50-50 in shares and bonds over each five year period since January 1950, and found the biggest loss for investors was just 1 per cent per year, as opposed to up to 7 per cent for those exclusively invested in stocks. Equities, however, should be your first port-of-call. “Shares are a good hedge against inflation, because they represent a real claim on a real company’s assets and cash flows, which can rise in line with rising inflation,” says Tom Stevenson of Fidelity.

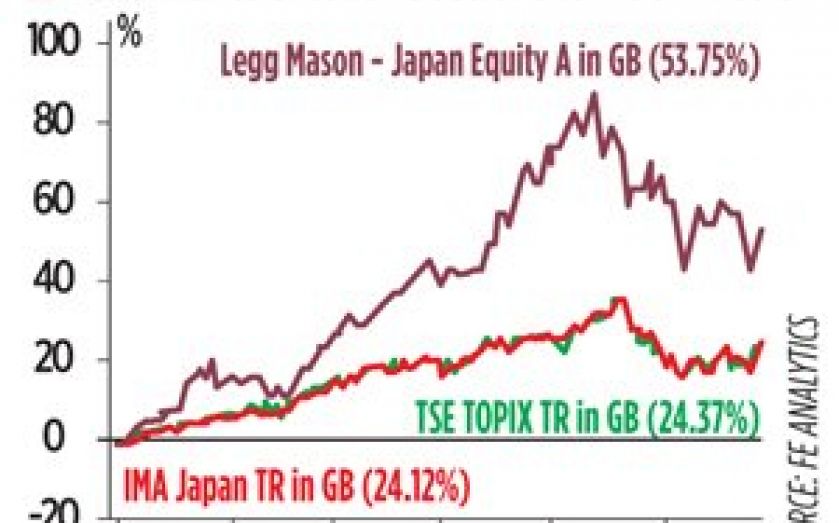

Japanese equity funds performed well during September, with the MSCI AS Asia Pacific ex Japan Index rising 1.2 per cent in sterling terms, for example. But Fidelity thinks long-term investors should look to global equity funds, like the Newton Global Higher Income fund, which has seen 4.76 per cent growth in the past 12 months. Jason Hollands of Bestinvest, meanwhile, rates the Threadneedle UK Equity Income fund, whose managers seek balance, “rather than exhibiting strong sector, style, cyclical, or defensive biases often seen in the UK Equity Income sector”.

Regionally, developed markets are outperforming emerging markets, which Fidelity’s Eugene Philalithis expects to continue into 2014. “We anticipate further strengthening of the dollar and weakening of the yen – a bad scenario for emerging markets,” he says.

THE BOND DEBATE

Although arguably less risky than equities, some bond funds still offer reasonable returns. The Henderson Strategic Bond fund, for example, is currently yielding 5.7 per cent, and invests in a mix of high-yield, investment grade, and government bonds. But if prices rise, the “nominal value of the income you will get – and the capital repaid on that bond – is fixed. So it becomes a less valuable asset in a rising inflation environment,” says Stevenson.

And spooked investors have started to pull out of these funds for fear that they are overvalued, and that the US Federal Reserve will start to taper its stimulus programme. In September, the IMA Global Bonds and IMA Index-Linked Gilts sectors delivered the worst performance. So where else can you look?

REAL ASSETS

Gold is often viewed as a hedge against inflation, but is heading for its first annual loss in 13 years, having dropped by over 20 per cent this year. It can be bought physically, through an exchange-traded fund, or through gold equities. But while a US default this week could lead to a surge in its popularity as the panic asset of choice, Morgan Stanley has said bullion will average $1,313 an ounce in 2014, down from the $1,420 forecast this year. “It’s a marmite asset class. You love it or hate it,” says Philalithis.

For those concerned that property – also traditionally seen as an inflation hedge – is a big investment and highly illiquid, investing in commercial real estate could be a good option, as it enables you to put your cash over a wide range of properties. Hollands points to the Henderson UK Property fund, which has a spread of property investments in areas like retail parks and hospitals, and is yielding 4.3 per cent.

But regardless of your take, the two key considerations when buying any asset must be its valuation, and future prospects.