Countdown to Brexit: three market indicators to watch

The UK is due to leave the European Union (EU) on 29 March 2019. With politicians still struggling to agree the terms of withdrawal, investors in assets linked to the UK economy could be in for an uncertain time.

UK investments have already underperformed their global peers since Britain voted to leave the EU, in June 2016. For instance, sterling is down 8.4 per cent since the vote and despite UK stocks hitting record highs in August 2016 and the FTSE All-Share index returning an apparently healthy 24 per cent since June 2016, it nevertheless lags the 32 per cent gain made by global stocks, as measured by the MSCI World Index.

There are of course other factors also affecting markets, such as the ongoing trade dispute between the US and China and a slowing global economy. However, the influence of Brexit will have been significant.

Positioning now for a particular Brexit conclusion is perhaps unwise as the range of possible outcomes is very wide. But gauging market sentiment could help investors manage their investment risk and return expectations.

Below are three simple Brexit indicators for investors to keep an eye on.

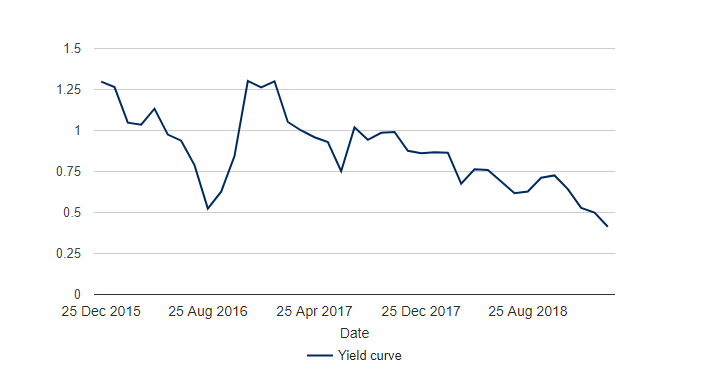

1. The yield curve

This is far less complicated than it sounds. The yield curve is the difference between the interest rate (yield) on a longer-dated bond (debt issued by a corporation or country) and a shorter-dated bond.

For instance, typically it should cost less to borrow money for two years than for 10 years. This is because the economy is expected to grow over time and experience inflation. Inflation erodes the fixed return of a bond and investors tend to want compensation for taking on that risk. They therefore demand a higher yield for longer-dated bonds, so the yield curve should slope upwards.

However, when it costs more to borrow money in the short term than it does in the long term, the yield curve inverts.

The yield curve has been a reliable predictor of US recessions over the last four decades. Its track record in the UK is less dependable. Nevertheless, a UK yield curve that is close to inverting suggests at best that investors expect the economy to slow, at worst it might be an early signal a recession could be on the way.

In the example below, we look at the difference between the yields on a two- and 10-year gilt, which is a UK government bond.

Currently a two-year UK government bond yields around 0.8 per cent. This compares with a 10-year which yields around 1.2 per cent. The interest rate on the longer-dated bond is more than the shorter dates but this gap has been narrowing. Before the Brexit vote the comparable yields were 0.6 per cent and 1.9 per cent respectively.

The sharp fall on the graph below, in 2016, coincided with the Brexit vote. That was a signal, rightly or wrongly, that investors were concerned about the outlook for the UK economy. Should the line on the chart dip below zero, this would indicate that the yield curve had inverted. This is as close to happening now as it ever has been since the vote.

How the gap between 2 and 10 year gilt yields has narrowed

This material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Past performance is not a guide to future returns and may not be repeated.

Source: Schroders. Data for Sterling trade weighted index from Refinitiv correct as at 26 February 2019.

A weak currency has so far prevented UK stocks from underperforming even further. This is because a lot of the companies listed on the UK stock market generate their profits from outside the UK.

Profits earned in foreign currency are worth more when converted back into local currency providing the local currency is weaker, which is currently the case with sterling.

A stock market is a leading indicator of what investors think company profits will be in the future. However, many believe the positive effects of a weak currency are beginning to wear off for UK stocks.

Read more: How currencies move stock markets

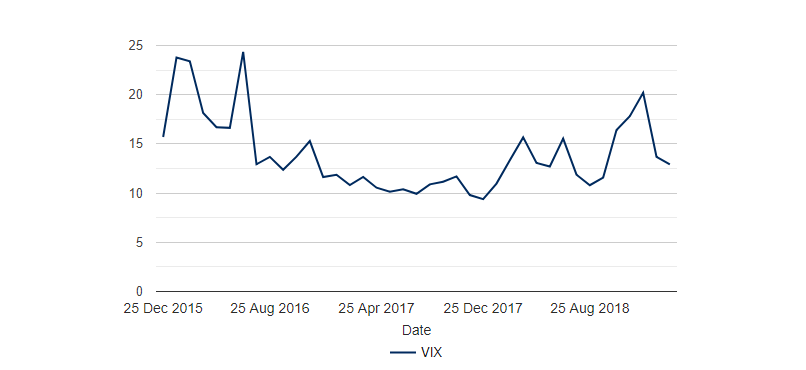

3. FTSE volatility index

As mentioned previously, UK stocks have underperformed their global peers by a long way since the Brexit vote. In fact, their underperformance has left UK stocks looking attractively valued against historic comparison.

Read more: Which stock markets look cheap

The challenge for investors is working out if UK stocks are being unfairly undervalued or if they have been accurately priced for any further global and Brexit-related uncertainties.

Predicting precisely when and if a market falls is all but impossible. However, we can look for signs of a growing lack of confidence or overconfidence among investors.

The volatility index (VIX), otherwise known as the fear gauge, attempts to measure sentiment among investors. It is a leading indicator, not based on historical data, which narrows the outlook to the near-term.

The VIX currently has a reading around 13 per cent. In the days surrounding the Brexit vote, in June 2016, the gauge was in the mid 20s.

A higher reading suggests that investors anticipate a market-moving event is on the horizon. To put the current level of the VIX into a broader context, it touched a high of 75% at the height of the global financial crisis in October 2008.

The VIX is not a perfect indicator. For instance if the VIX rises by 20 per cent that doesn’t necessarily mean FTSE will fall by the same amount, if at all. Investors should consider it carefully and decide how much weight they want to attribute to it when they make an investment decision.

The FTSE volatility index: fear gauge is rising

This material is not intended to provide advice of any kind. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Past performance is not a guide to future returns and may not be repeated.

Source: Schroders. Data for the Volatility Index from Refinitiv correct as at 26 February 2019.

Claire Walsh, Personal Finance Director at Schroders, said: “While Brexit is a cause for uncertainty it shouldn’t necessarily be a reason not to invest. History has shown that people can still benefit from investing despite wars, disasters, economic strife and political instability.

“Preparing your portfolio for a specific Brexit outcome is all but impossible but investors can take steps to minimise turbulence. Diversifying your portfolio and making sure you’re not over exposed to one particular area of the market would seem sensible.

“A mixture of local and international company shares, property, bonds, and commodities could provide some mitigation against any shocks. You can buy funds that specialise in these areas. Funds will pool your money with that of other investors to give exposure to more investments than you could buy by yourself.”

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

If you are unsure as to the suitability of your investment, speak to a financial adviser.

If you want more insights from Schroders visit thier content hub and follow them on twitter.

Important Information: The views and opinions contained herein are of those named in the article and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 1 London Wall Place, London, EC2Y 5AU. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.