Consolidate: Don’t let your Isas go to waste

But be very careful to avoid committing the cardinal sin of losing the tax wrapper on your existing investment

With the end of the tax year fast approaching (5 April), the clock is ticking to make the most of your full Isa allowance (currently £11,520, up to half of which can be held in cash). But it is just as important to review existing Isa investments, says Catherine Penney of Barclays Stockbrokers, and take action by transferring and consolidating where necessary. Transferring old cash Isas can help avoid below inflation returns, while consolidating stocks and shares Isa investments through one platform could keep a lid on fees.

MEASLY RETURNS

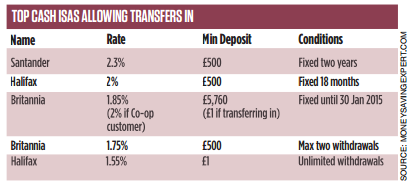

Transferring existing Isa investments (whether cash or stocks) does not eat into the current year’s allowance. And doing so makes financial sense, particularly with older cash Isas. The returns on these products are sometimes slashed by as much as 90 per cent after the initial rates expire, leaving savers exposed to losses in real terms. Some will need to keep this capital in cash as a “rainy day fund”, says Jason Witcombe of Evolve Financial Planners, in which case there are a range of new cash Isas allowing transfers in (see table). But returns will still be small compared to equities. As Tom Stevenson of Fidelity says, over long time horizons, the number of years in which equities outperform cash is very close to 100 per cent.

Moving from a cash to a stocks and shares Isa is “one way trip”, says Interactive Investor’s Rebecca O’Keeffe. “While you can transfer from a cash Isa into a stocks and shares Isa, you can’t transfer back.” But most stocks and shares Isa providers offer a cash park facility, meaning you can hold it as cash until you are ready to invest, or phase it into the market over a period of time.

THE CARDINAL SIN

Crucially, and this also holds for transfers between stocks and shares Isa providers, the switch must be made through the institutions. “You should never take the cash out of the tax wrapper and make the transfer yourself,” says Ben Smaje of Kennedy Black Wealth Management. “This is the cardinal sin of Isa transfers.” By pulling capital out of the Isa (whether cash or stocks and shares), you will lose the tax-free status, and have to slowly build it up again through subsequent annual allowances. Instead, go directly to the institution that you would like to switch to, fill out its transfer form, and tell the old provider to close the account.

CONSOLIDATING STOCKS AND SHARE ISAS

Moving existing stocks and shares Isa investments into one platform can lead to significant savings if carried out correctly, says Smaje. “You can realise economies of scale by not paying multiple fees to different providers.” And Penney points out that the introduction of “clean” share classes in the wake of the Retail Distribution Review adds another dimension to this: “If you are in the legacy trail-paying share classes, this could adversely impact your returns.”

But as exit fees are often charged, switchers should make sure that the new platform will meet the cost of transferal. Barclays Stockbrokers, for example, will cover costs up to £150 per old account, up to a maximum of £500. Further, James Robson of Plutus Wealth points out that not all platforms have the same range of funds on offer, which means it’s always worth checking to make sure you won’t be forced to sell a favourite pick upon switching.

There are two ways of making the transfer, O’Keeffe says – in-specie or cash. “Cash transfers take a lot less time, but you are out of the market while it’s underway.” This could mean missing out on a market rally. “In-specie transfers mean you stay invested, but can take a few weeks to complete.”