In charts: Half of women don’t have private pensions

Despite the maximum state pension being only £113.10 a week, just under half the people in the UK don't pay into a private pension scheme.

This includes a third of employees – half of the self-employed and 80 per cent of unemployed people are also without a plan.

The data was published by the Office of National Statistics and was accumulated between 2010 and 2012.

As you might expect, the figures vary across age, earnings and gender bands.

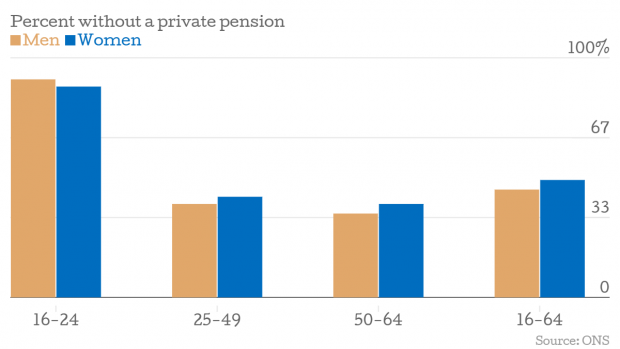

Interestingly, across all but the 16-24 age group, women were less likely to have a scheme. This could be down to differences in employment demographics rather than a difference in attitude, especially given what the earnings data (chart three) shows.

The split among workers from different employment brackets is much more varied, with higher-paid professionals far more likely to pay into a scheme. Among those in managerial positions (typically better-paid posts) women are more likely to have a private scheme. The tables turn as the brackets move towards "routine" roles (e.g. bar staff, lorry drivers or labourers):

Viewed by earnings rather than socio-economic group, the data shows a bigger gap at the high end of wages. Among those earning more than £600 a week, 27 per cent of men don't pay into a private pension, while all but 18 per cent of women do.

The earnings split implies that when only money is considered, women were more likely to have a private pension:

We believe the reason why [the data in the above graph] shows a higher percentage of men without a pension… is that there are large numbers of female employees in the industries where pension membership is relatively high.These female employees will be spread across the earnings bands… and so raise the membership level for women ineach earnings band.Also, more men had higher weekly earnings than women, and given that those with high earnings are more likely to have a private pension, it helps to explain why overall men have higher percentages with a private pension.

Regional differences

How likely people are to have private pension provision was also influenced by where in the country they live. The costs of living in London seem to be prohibitive, with 35 per cent of capital dwellers going without a pension.

Step just outside the capital though, and the figure drops to 20 per cent, again likely reflecting the demographics of the areas. London is expensive and has a relatively young population.

The report draws some obvious conclusions, including the wealth/pension ratio:

The households that had no private pension also seemed to have lower amounts of other wealth such as wealth in property, financial wealth and wealth in physical assets. London was the English region that had the highest proportion of households without a private pension.