Why pension funds might not be to blame for the UK’s capital market decline

Pension funds have taken on an interesting new role in the City psyche over the past year.

Once just guardians of the country’s retirement cash, they have morphed into punch bags on which to unleash frustration at the UK’s capital market decline. A sort of anti-growth coalition unwilling to back home-reared equities and believe in British prosperity.

That flurry of punches has ramped up significantly in the past month. London’s markets have been struck a series of blows as Arm snubbed London for New York, CRH packed its bags to head for the Big Apple and WANdisco (then yet to reveal that $15m of its revenue may have been fictitious and fraudulent) said it was scoping out a dual listing.

Blame has again been shifted partly on to the pension funds for not getting behind the country’s home-grown firms. But is this fair?

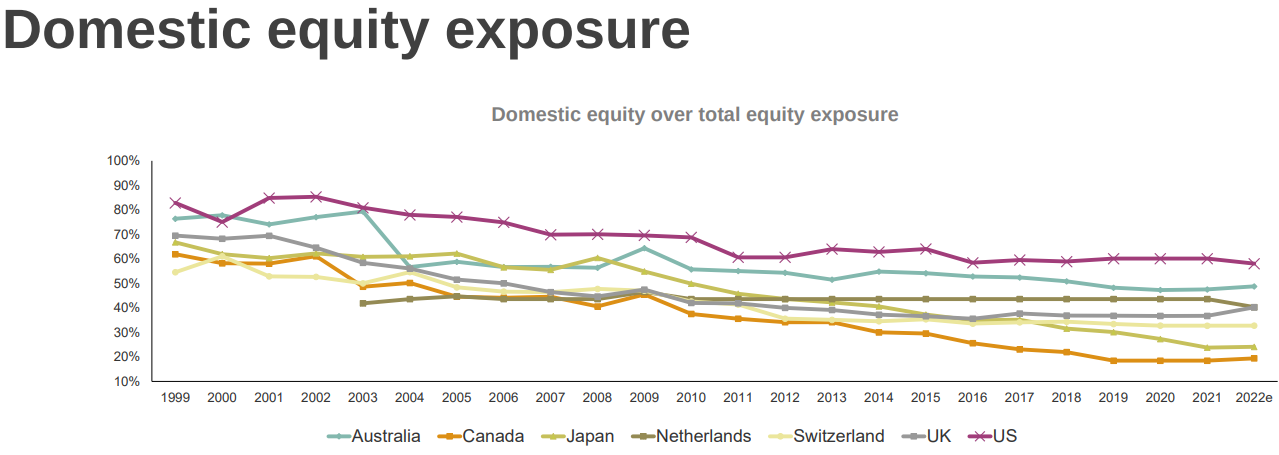

Pension funds’ holding of UK equities has dropped sharply over the past two decades. Just four per cent of the UK stock market is now held by pension funds – down from 39 per cent in 2000, according to a new report from think tank New Financial.

A letter from the Capital Markets Industry Taskforce, headed by London Stock Exchange chief Julia Hoggett, recently flagged an “alarming” fall in domestic equity holdings and urged Jeremy Hunt to step in to accelerate consolidation.

But declining domestic equity investment by pension funds is a global trend. Since 2000, pension funds have looked to diversify their holdings and much of that has been global diversification.

Domestic equity exposure, as a percentage of equity holdings, has dipped on average from 67.1 per cent to 37.7 per cent between 2002 and 2022 in every major market, according to figures from Willis Towers Watson. And the UK has actually held up more steadily in its home-market holdings than many.

Global head of pensions at PwC Raj Mody tells City A.M. that the managers running defined benefit pension money in the UK – which are now largely in run-off and therefore unlikely to be punting on long-term growth stocks – don’t really care geographically where the money’s invested as long as it’s not vulnerable to wild swings relative to their liabilities.

“To the extent that they do invest in equities, pension funds do so to grow their assets. Whether that’s UK or global, they’re not necessarily that concerned about where the listing is as long as they’ve got diversification,” he says.

A general drop in equity holdings is not a UK phenomenon, he adds, and the money that managers do still set aside to invest in stocks can flow wherever they want it to.

And to that end, the Canadian and Australian super funds – that are so often held up as an example to the UK – could easily flow into UK equities to make up the shortfall left by the UK funds. They’re just choosing not to.

Pension fund managers are on the hunt for the best of their beneficiaries, not some sense of national good, says Dan Mikulskis, an investment partner and pensions specialist at City actuary firm LCP. He argues the problems lie instead with what’s on offer from UK corporates rather than pension money.

“If British companies are so great, everyone would want to invest in them, and it’s no problem. Why would we [need] this kind of nationalistic, jingoistic hype speech,” he says.

For Mikulskis, the problem lies in years of uncompetitive policy and corporate underperformance rather than conservatism on the part of pension fund managers.

Earnings per share statistics bear that out. US firms have far outpaced their UK counterparts and therefore simply make a more shrewd investment, Mikulskis argues.

“When you look at all those things before pointing the finger at pensions, then it doesn’t make any sense to try and wind back to some anachronistic 90s situation where all UK pension funds were investing in UK companies,” he says.

Mikulskis says pension schemes trustees and fund managers “should be more annoyed” at the public kicking they get, but scheme trustees and money managers “tend to let it wash over them”.

The market may be shifting more naturally towards equity backing in the UK, however, as defined contribution schemes – a pension based on how much is paid in rather than out – grow with a younger, auto-enrolled member base. Buyouts by insurance companies and master trusts are also helping pool cash and potentially helping a move toward investing in stocks and companies again.

There are also movements in the private markets, with the Lord Mayor of London looking to galvanise the nation’s big insurers and pension funds into backing British start-ups and growth companies via a £50bn ‘future growth fund’. Jeremy Hunt also unveiled new measures in the budget last week for investment vehicles designed to ease the flow of cash from DC schemes into science and tech firms.

But those are, unfortunately, fairly long-term fixes. For the minute, it may be right to look at pension funds’ lack of enthusiasm for UK equities as a symptom of corporate decline, rather than a cause.