Texas Stock Exchange (TXSE) Selects Options’ AtlasInsight for Next Generation Packet Capture and Real Time Analytics

Options Technology (Options), the leading provider of financial services infrastructure, today announced that its AtlasInsight platform has been selected by the Texas Stock Exchange (TXSE) to deliver high-fidelity packet capture and real-time analytics across TXSE’s proprietary, world-class trading infrastructure.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260311267175/en/

As TXSE prepares to launch the first fully integrated exchange in over 25 years, the exchange has engineered its core infrastructure from the ground up to prioritize performance, speed, and latency. AtlasInsight will integrate with TXSE’s architecture to provide full-fidelity capture at line-rate (up to 200 Gb/s), deep protocol analytics, and infrastructure performance management, enhancing transparency and competitiveness from day one.

Danny Moore, President and CEO of Options Technology, commented: “We are excited to partner with TXSE as they bring a truly disruptive exchange model to the U.S. markets. By integrating our ultra-high-performance capture and analytics capabilities with their proprietary infrastructure, we are supporting their commitment to operational transparency and reliability from day one.”

“At TXSE, we are building our core exchange infrastructure from the ground up, to meet the highest standards of performance,” said Rick Yoder, Chief Technology Officer at TXSE. “AtlasInsight integrates with and enhances that foundation by delivering the real-time, full-fidelity visibility we need across our network and market data infrastructure.”

The announcement builds on recent milestones at Options, including the global deployment of AtlasInsight across Options global infrastructure, the launch of AtlasInsight Capture 200 enabling line-rate 200Gb/s packet capture on commodity hardware, and the introduction of PrivateMind, a secure AI platform designed specifically for financial services.

Options Technology:

Options Technology (Options) is a financial technology company at the forefront of banking and trading infrastructure. We serve clients globally with offices in New York, London, Belfast, Cambridge, Chicago, Hong Kong, Tokyo, Singapore, Paris, and Auckland. At Options, our services are woven into the hottest trends in global technology, including high-performance Networking, Cloud, Security, and AI (Artificial Intelligence).

www.options-it.com

View source version on businesswire.com: https://www.businesswire.com/news/home/20260311267175/en/

Contact

For media inquiries, please contact Colleen Murray, colleen.murray@options-it.com

Xsolla Releases New Industry Report Identifying the Biggest Opportunities for the Future of Video Games for Developers

Xsolla, a leading global video game commerce company, today released the latest edition of The Xsolla Report, timed to coincide with this week’s activations and collaborations in San Francisco. This edition provides insights from working with thousands of studios to map out where the industry’s biggest opportunities are emerging.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260311021020/en/

The gaming industry remains extraordinarily vibrant, and the playbook for success is changing. Studios that are adapting their commercial strategies, embracing direct-to-player commerce, expanding into high-growth global markets, and leveraging AI to sharpen operations are pulling ahead and building businesses designed to thrive for years to come.

“The economics of game development have and will continue to shift and evolve into the future. Budgets have expanded, player acquisition costs have surged, and traditional publishing models are under increasing strain,” said Chris Hewish, President of Xsolla. “We have reached a tipping point where old assumptions no longer hold, and leaders who recognize this shift early will capture disproportionate advantage.”

“The conversation around direct-to-consumer in gaming has fundamentally changed coming out of multiple regulatory changes,” said Berkley Egenes, Chief Marketing and Growth Officer at Xsolla. “What began as a tactical revenue diversification play has evolved into a strategic imperative for studios to grow and thrive into the future of live-service games.“

Key Findings From The Xsolla Report Include:

- Leading game companies are already generating 15–45% of total revenue through D2C web shops, yielding up to 25% more profit per transaction compared to platform-based purchases

- High-growth markets like Turkey (13% CAGR), India (11%), and Southeast Asia (6%) represent the industry’s most exciting expansion opportunities through 2029

- AI is delivering real operational gains, compressing development timelines by roughly 20% and reducing support costs by approximately 40%

- “Platform omnivore” gamers who play across consoles, PC, and mobile now represent 43% of US gamers, up from 30%, creating new pathways for studios to reach players wherever they are

- Titles with sustainable live service models continue to grow, with PUBG: Battlegrounds reaching approximately 75 million Steam users and Roblox on Xbox climbing to nearly 30 million owners

- The April 2025 U.S. court ruling allowing in-app linking to external offers has opened the door for developers to engage players across channels like never before

The report also outlines a clear roadmap for what leaders should prioritize next: building for modularity and faster development cycles, investing in owned audience infrastructure, and turning compliance into a competitive advantage as global markets open up.

“We’re entering a period where the studios with strong foundational commercial infrastructure will outperform those with superior creative execution alone,” added Egenes. “D2C is becoming a table-stakes requirement for ambitious live-service games, and the studios that treat this moment as strategic will be the ones defining the future of mobile gaming success.”

The full Xsolla Report is available for download at: xsolla.pro/xsolla-report-v9.

About Xsolla

Xsolla is a global commerce company with robust tools and services to help developers solve the inherent challenges of the video game industry. From indie to AAA, companies partner with Xsolla to help them fund, distribute, market, and monetize their games. Grounded in the belief in the future of video games, Xsolla is resolute in the mission to bring opportunities together, and continually make new resources available to creators. Headquartered and incorporated in Los Angeles, California, Xsolla operates as the merchant of record and has helped over 1,500+ game developers to reach more players and grow their businesses around the world. With more paths to profits and ways to win, developers have all the things needed to enjoy the game.

For more information, visit xsolla.com.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260311021020/en/

Contact

Media Contact

Derrick Stembridge

Vice President of Global Public Relations, Xsolla

d.stembridge@xsolla.com

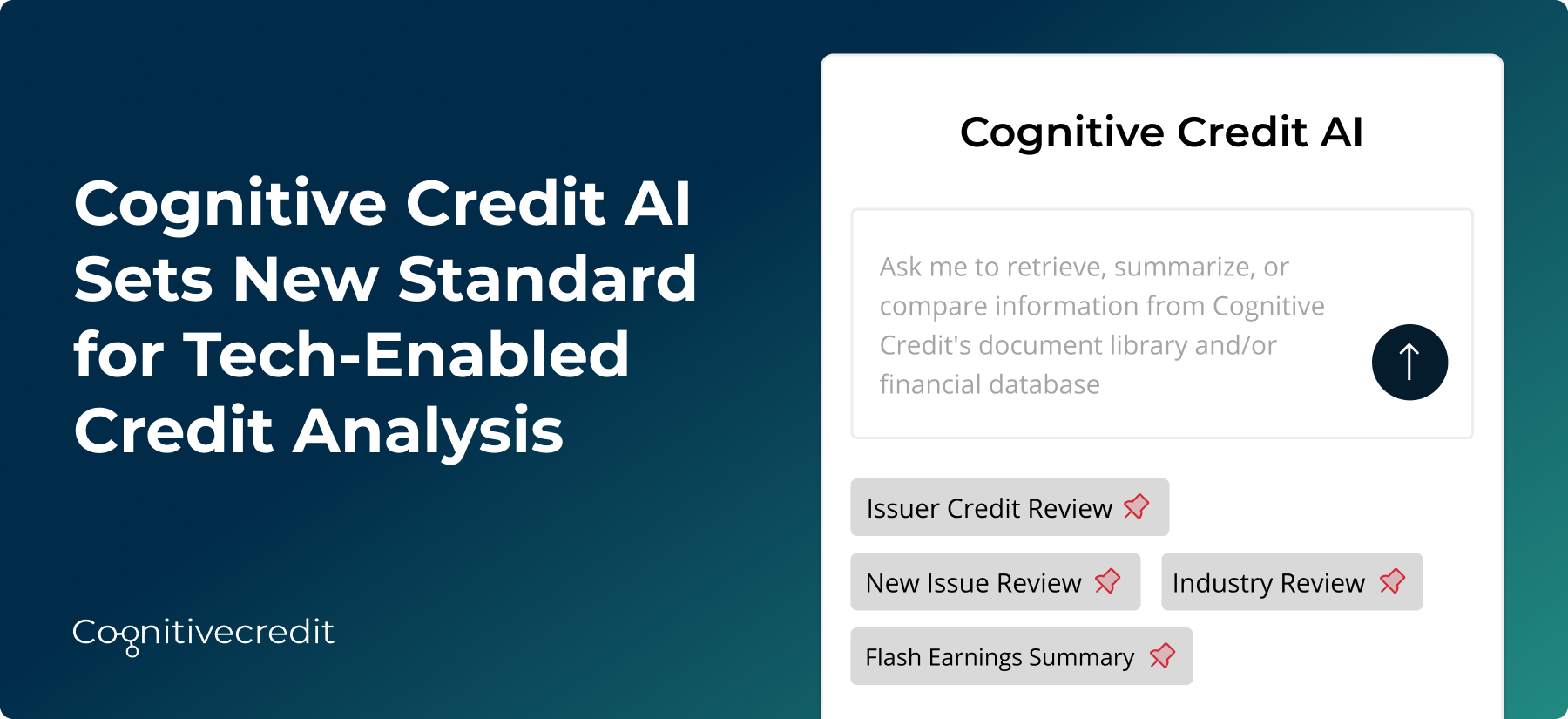

Cognitive Credit AI Sets New Standard for Tech-Enabled Credit Analysis

Cognitive Credit, the leading provider of specialist data and analytics for corporate credit markets, today announces the launch of Cognitive Credit AI, a new intelligence capability integrated into its existing offering. The new service enables credit investors to generate detailed, context-aware analysis from a library of more than 200,000 official documents and structured financial data sets covering over 3,000 European and U.S bond and loan issuers.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260311896261/en/

The launch comes as institutional credit teams seek new tools to modernize research workflows. As the volume and complexity of credit disclosure continue to expand, traditional research methods are increasingly difficult to scale. Faced with rising deal flow and large quantities of unstructured information, investment firms are turning to solutions that combine structured financial data with specialized AI capable of supporting faster analysis and broader market coverage.

Unlike general-purpose AI tools, Cognitive Credit AI is reinforced with domain-specific logic and built on proprietary data sets covering much of the European and U.S. credit markets, all designed specifically for credit professionals. Grounding AI outputs in structured financial data and official company disclosures ensures that resulting analysis remains accurate, transparent, and auditable — essential requirements for institutional investors. This approach also means users can summarize and synthesize key information across multiple inputs to support idea generation free from third-party opinions or hidden biases.

Users can query rich datasets using natural language, generate detailed responses to complex questions, and surface insights otherwise trapped in large volumes of disclosure, for all the companies they cover. Insights become available to users as soon as disclosures reach the market, and clients can manage sensitive documents in a closed, ring-fenced environment designed to preserve data security.

“The launch of Cognitive Credit AI represents a step change for how credit analysts can allocate their time,” said Robert Slater, CEO of Cognitive Credit. “This new capability adds a whole new layer of qualitative insights into our market-leading quantitative data offering, and allows credit teams to focus even more time on idea generation and expanding their market coverage.”

With this launch, Cognitive Credit further strengthens its position as the leading provider of credit market technology. By combining structured fundamental data with advanced analytics and AI, the firm delivers an integrated research workflow supporting market screening, idea generation, and ongoing credit monitoring across global corporate credit markets.

About Cognitive Credit

Cognitive Credit is the leading independent provider of specialist data, infrastructure, and AI solutions for global corporate credit markets. Built by credit professionals, for credit professionals, Cognitive Credit delivers the credit market’s fastest, broadest, most accurate fundamental structured data, as well as a suite of analytics and workflow tools that elevate the productivity of credit teams at the world’s leading investment banks, hedge funds, and asset managers. Today, Cognitive Credit counts 100% of the top 10 global investment banks and the majority of the top 25 global asset managers, as clients.

For more information, visit cognitivecredit.com/AI

View source version on businesswire.com: https://www.businesswire.com/news/home/20260311896261/en/

Contact

Robert Slater

CEO & Founder

robert.slater@cognitivecredit.com

Andrew Johnson

Head of Marketing

andrew.johnson@cognitivecredit.com

+44 (0)20 8103 3090

Abstract

Cognitive Credit today announces the launch of Cognitive Credit AI—a new intelligence capability integrated into its existing offering.

TweetText

“This new capability adds a whole new layer of qualitative insights into our market-leading quantitative data offering, and will allow credit teams to focus even more time on idea generation and expanding their market coverage.”

Janus Henderson Group plc Board of Directors Determines by Unanimous Vote that Victory Capital’s Proposal Is Not Superior and Reaffirms Recommendation of Transaction with Trian and General Catalyst

Janus Henderson Group plc (NYSE: JHG; “JHG,” “Janus Henderson,” or the “Company”) today announced that its Board of Directors (the “Board”), acting on the unanimous recommendation of the Special Committee of the Board (the “Special Committee”), has determined by unanimous vote that the unsolicited, non-binding proposal received on February 26, 2026 (the “Victory Proposal”) from Victory Capital Holdings, Inc. (NASDAQ: VCTR; “Victory”) is not in the best interests of Janus Henderson and its shareholders and does not constitute, and would not reasonably be expected to result in, a Company Superior Proposal under the terms of the merger agreement providing for the acquisition of Janus Henderson by Trian and General Catalyst (the “Merger Agreement”).

In the course of its review of strategic alternatives described in the Company’s proxy statement relating to the Merger Agreement, the Special Committee previously received two non-binding proposals from Victory on November 24, 2025 and December 8, 2025. After evaluating the prior proposals, the Special Committee determined that they were not actionable. The February 26 Victory Proposal offered no meaningful improvement in terms.

The February 26 Victory Proposal contemplates an acquisition of Janus Henderson for $30 per share in cash and Victory stock representing pro forma ownership of 38% of the combined company, consistent with Victory’s prior proposals of $30 per share in cash and Victory stock representing pro forma ownership of 37% to 39% of the combined company. The purported increase in headline price resulted solely from movements in Victory’s stock price since its prior proposals. Since Victory resubmitted its proposal, Victory’s stock price has declined 14%.

Nonetheless, following receipt of the Victory Proposal, at the direction of the Special Committee and in the interest of maximizing shareholder value, Janus Henderson obtained a temporary waiver from Trian and General Catalyst under the Merger Agreement in order to clarify and diligence the terms of the Victory Proposal. After another thorough review of the Victory Proposal, including direct engagement with Victory management, the Special Committee and the Board continue to believe the Victory Proposal is not in the best interests of Janus Henderson and its stakeholders, including its shareholders, clients and employees, and is not actionable because it presents significant consummation risk and uncertain value.

Significant Closing Risks

The Victory Proposal presents significant closing risks.

-

Based on Client Feedback, Significant Uncertainty in Ability to Obtain the Required 75% Client Consent Threshold. In order to close the transaction contemplated by the Victory Proposal, Janus Henderson would need to obtain client consents representing at least 75% of its revenue run-rate. The Special Committee has received feedback from key Janus Henderson clients indicating they would have significant reservations about maintaining their relationships with Janus Henderson if it were to enter into a transaction with Victory. Based on this feedback, the Special Committee has serious concerns that the requisite client consents may not be obtained.

-

Aggressive $500 Million Synergy Estimate Exacerbates Closing Risk. These concerns arise from, among other things, the substantial cost-cutting inherent in Victory’s business model and implicit in Victory’s estimate of $500 million of synergies, a figure which exceeds all of Janus Henderson’s non-investment costs in the U.S. and which suggests a level of cost-cutting that could lead to the disruption of systems and services, attrition of investment staff, deterioration in compliance functions and the degradation of investment performance and client experience. Key Janus Henderson investment professionals have also informed the Special Committee that they would leave the Company if it were acquired by Victory, and the possibility of those departures would make it more difficult to obtain the requisite client consents. By contrast, clients have expressed overwhelming support for the proposed transaction with Trian and General Catalyst, and the Special Committee believes the client consent condition for that transaction will be satisfied.

-

Highly Uncertain Janus Henderson Shareholder Approval. Under Jersey law, a merger proposal requires approval by two-thirds of the total number of votes cast at the shareholders’ meeting. Trian, which as of the March 9, 2026 record date for the Janus Henderson shareholder meeting held 20.7% of Janus Henderson’s outstanding shares, has reiterated to the Special Committee that it will vote against, and actively solicit opposition to, the Victory Proposal. Accordingly, a transaction with Victory would require approval by a proportion of other Janus Henderson shareholders approaching 90%, even assuming the transaction is voted on by a larger than average proportion of shares voted at recent Janus Henderson annual meetings over the last five years. If even a limited number of other significant shareholders are skeptical of the value or closing certainty of the Victory Proposal and vote against it, the proposal would fail to receive the required vote.

- Victory Shareholder Vote Is Uncertain. The Victory Proposal would also require approval by Victory’s own shareholders, another deficiency relative to the existing transaction with Trian and General Catalyst. There is risk that Victory’s shareholders might not approve the transaction, particularly considering the significant decline in Victory’s stock price since the announcement of its February 26 proposal—a decline that suggests that some Victory shareholders may oppose the combination. No acquiror shareholder approval is required to complete the transaction with Trian and General Catalyst.

Continued volatility in Victory’s stock price creates additional risk for the required shareholder votes, which would not occur for several months, as the value of Victory’s proposed stock consideration at that time is highly uncertain.

If any of the required shareholder approvals or the requisite client consents were not obtained, the transaction with Victory would not close. During the Special Committee’s engagement with representatives of Victory, they did not articulate a specific plan for obtaining the required shareholder and client consents necessary to complete the transaction.

The Special Committee disagrees with Victory’s criticism of the strength of Trian’s and General Catalyst’s financing commitments and the implication that Victory’s financing package is superior. The Trian and General Catalyst transaction is backed by customary binding debt and equity commitment letters covering the full purchase price, without relying on any of Janus Henderson’s available balance sheet cash.

By contrast, Victory’s debt commitment papers are in draft form, include a due diligence out for the lenders and are subject to credit committee approval. Victory also has not clarified its sources and uses and whether it plans to rely on cash from Janus Henderson’s balance sheet to fund a portion of its purchase price. Even assuming Victory fixed these defects in its debt commitment papers, its financing would be no more certain than the financing under the Merger Agreement, which is fully backed by customary limited conditionality commitment letters.

Uncertain Value and Significant Execution Risks

If Janus Henderson were to enter into a merger agreement providing for a transaction with Victory that fails to close, the Company would be gravely damaged. Most importantly, during the pendency of a transaction with Victory—a period expected to be meaningfully longer than the remaining time needed to complete the transaction with Trian and General Catalyst—Janus Henderson may suffer substantial client outflows and employee attrition given Victory’s aggressive planned cost-cutting and clients’ resulting expectations of reduced client service and diminished investment performance. The Special Committee has already received feedback to that effect from certain key clients and employees.

If that transaction failed to close, Janus Henderson’s business would be significantly diminished. There would be no guarantee that the Company could at that point command a valuation approaching the $49 per share payable in the transaction with Trian and General Catalyst, and there is significant risk that it would not. In addition, Janus Henderson would be required to pay a termination fee of $297 million to accept the Victory Proposal or change its recommendation with respect to the transaction with Trian and General Catalyst, which Victory has not offered to pay, unlike the vast majority of interloping buyers.

In addition to the significant closing risks, the Victory Proposal offers uncertain value. The value of Victory’s proposal, and the 38% share of the combined company proposed to be acquired by Janus Henderson shareholders, depends significantly on Victory’s ability to successfully integrate its largest ever acquisition target—with the Company’s current market capitalization more than 80% larger than Victory’s—manage substantially higher leverage, and achieve its $500 million in estimated synergies. The integration of Janus Henderson’s product offering into Victory’s multi-boutique model may create product overlaps that could result in meaningful dis-synergies. The disparate business models and cultures of the two companies puts further pressure on synergies and integration risk. If Victory is unable to achieve its target synergies, the combined company would bear even higher leverage and risk increased borrowings costs.

In its proposal and in discussions with the Special Committee, Victory has not adequately justified its synergies estimate, which exceeds typical synergy levels realized in precedent transactions. The Special Committee is not persuaded that the synergies contemplated by the Victory Proposal can be achieved, and even targeting such a large reduction in costs would likely result in technology and systems disruption, employee attrition and client outflows. Victory also has not provided any explanation as to why the combined company stock would continue to trade at Victory’s existing multiple following a combination with Janus Henderson, even without accounting for these financial and operational risks.

In contrast to the Victory Proposal, Janus Henderson’s binding Merger Agreement to be acquired by Trian and General Catalyst is an actionable transaction that offers certain value to shareholders with significantly less closing and execution risk than the Victory Proposal and is on track to be completed on its planned timeline in mid-2026.

For these reasons, the Janus Henderson Board, acting on the unanimous recommendation of the Special Committee, has determined by unanimous vote that the Victory Proposal does not constitute, and would not reasonably be expected to result in, a Company Superior Proposal, and reaffirms its recommendation that Janus Henderson shareholders vote for the approval and adoption of the Merger Agreement at the Janus Henderson shareholders’ meeting to be held on April 16, 2026.

Goldman Sachs & Co. LLC is acting as financial advisor to the Special Committee, and Wachtell, Lipton, Rosen & Katz is acting as legal advisor to the Special Committee. Skadden, Arps, Slate, Meagher & Flom LLP is acting as legal advisor to Janus Henderson.

Forward Looking Statements

Certain statements in this press release not based on historical facts are “forward-looking statements” within the meaning of the federal securities laws. Such forward-looking statements involve known and unknown risks and uncertainties that are difficult to predict and could cause our actual results, performance or achievements to differ materially from those discussed. These include statements as to our future expectations, beliefs, plans, strategies, objectives, events, conditions, financial performance, prospects or future events, including with respect to the timing and anticipated benefits of pending and recently completed transactions and strategic partnerships, and expectations regarding opportunities that align with our strategy. In some cases, forward-looking statements can be identified by the use of words such as “may,” “could,” “expect,” “intend,” “plan,” “seek,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “continue,” “likely,” “will,” “would,” and similar words and phrases. Forward-looking statements are necessarily based on estimates and assumptions that, while considered reasonable by us and our management, are inherently uncertain. Accordingly, you should not place undue reliance on forward-looking statements, which speak only as of the date they are made and are not guarantees of future performance. We do not undertake any obligation to publicly update or revise these forward-looking statements.

Various risks, uncertainties, assumptions and factors that could cause our future results to differ materially from those expressed by the forward-looking statements included in this press release include, but are not limited to, the impact of any alternative proposal, Janus Henderson’s ability to obtain the regulatory, shareholder and other approvals required to consummate the proposed transaction and the timing of the closing of the proposed transaction, including the risks that a condition to closing would not be satisfied within the expected timeframe or at all or that the closing of the proposed transaction would not occur, the outcome of any legal proceedings that may be instituted against the parties and others related to the merger agreement, that shareholder litigation in connection with the proposed transaction may affect the timing or occurrence of the proposed transaction or result in significant costs of defense, indemnification and liability, unanticipated difficulties or expenditures relating to the proposed transaction, including the impact of the transaction on Janus Henderson’s business, that the proposed transaction generally may involve unexpected costs, liabilities or delays, that the business of Janus Henderson may suffer as a result of uncertainty surrounding the proposed transaction or the identity of the purchaser, that Janus Henderson may be adversely affected by other economic, business, and/or competitive factors, including the net asset value of assets in certain of Janus Henderson’s funds, and/or potential difficulties in employee retention as a result of the announcement and pendency of the proposed transaction, changes in interest rates and inflation, changes in trade policies (including the imposition of new or increased tariffs), volatility or disruption in financial markets, our investment performance as compared to third-party benchmarks or competitive products, redemptions, and other risks, uncertainties, assumptions, and factors discussed in our Annual Report on Form 10-K for the year ended December 31, 2025, and in other filings or furnishings made by Janus Henderson with the SEC from time to time.

Important Additional Information and Where to Find It

In connection with the proposed transaction, Janus Henderson Group plc (“Janus Henderson”) filed a definitive proxy statement with the U.S. Securities and Exchange Commission (the “SEC”) on March 11, 2026, which will be first mailed to Janus Henderson’s shareholders on or about March 12, 2026. Janus Henderson and affiliates of Janus Henderson jointly filed a transaction statement on Schedule 13E-3 on March 11, 2026. Janus Henderson may also file other documents with the SEC regarding the proposed transaction, including amendments or supplements to the proxy statement or Schedule 13E-3. This communication is not a substitute for the proxy statement, the Schedule 13E-3 or any other document that may be filed by Janus Henderson with the SEC. INVESTORS AND SECURITY HOLDERS OF JANUS HENDERSON ARE URGED TO READ THE PROXY STATEMENT, THE SCHEDULE 13E-3 AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY, BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain the proxy statement and the Schedule 13E-3 and other documents that are filed with the SEC by Janus Henderson free of charge from the SEC’s website at https://www.sec.gov or through the investor relations section of Janus Henderson’s website at https://ir.janushenderson.com.

Participants in the Solicitation

Janus Henderson and its directors and certain of its executive officers and other employees may be deemed to be participants in the solicitation of proxies from Janus Henderson’s shareholders in connection with the proposed transaction. Information about the directors and executive officers of Janus Henderson and their ownership of Janus Henderson common shares is contained in the definitive proxy statement for Janus Henderson’s 2025 annual meeting of shareholders (the “Annual Meeting Proxy Statement”), which was filed with the SEC on March 21, 2025, including under the headings “Proposal 1: Election of Directors,” “Corporate Governance,” “Board Compensation,” “Proposal 2: Advisory Say-on-Pay Vote on Executive Compensation,” “Executive Compensation,” “Executive Compensation Tables,” “Securities Ownership of Certain Beneficial Owners and Management” and “Our Executive Officers.” Additional information regarding the persons who may, under the rules of the SEC, be deemed participants in the solicitation of the shareholders of Janus Henderson in connection with the proposed transaction, including a description of their direct or indirect interests, by security holdings or otherwise, has been included in the definitive proxy statement relating to the proposed transaction. To the extent holdings of securities by potential participants (or the identity of such participants) have changed since the information printed in the Annual Meeting Proxy Statement, such information has been or will be reflected on the Statements of Change in Ownership of Janus Henderson on Forms 3 and 4 filed with the SEC. Free copies of the proxy statement relating to the proposed transaction and free copies of the other SEC filings to which reference is made in this paragraph may be obtained from the SEC’s website at https://www.sec.gov or through the investor relations section of Janus Henderson’s website at https://ir.janushenderson.com.

About Janus Henderson

Janus Henderson Group is a leading global active asset manager dedicated to helping clients define and achieve superior financial outcomes through differentiated insights, disciplined investments, and world-class service. As of December 31, 2025, Janus Henderson had approximately US$493 billion in assets under management, more than 2,000 employees, and offices in 25 cities worldwide. The firm helps millions of people globally invest in a brighter future together. Headquartered in London, Janus Henderson is listed on the NYSE.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260311343450/en/

Contact

Investor enquiries:

Jim Kurtz

Head of Investor Relations

+1 303 336 4529

jim.kurtz@janushenderson.com

Innisfree M&A Incorporated

Scott Winter / Gabrielle Wolf

+1 212 750 5833

Media enquiries:

Candice Sun

Global Head of Corporate Communications

+1 303 336 5452

candice.sun@janushenderson.com

Kekst CNC

Ruth Pachman ruth.pachman@kekstcnc.com

Tom Davies tom.davies@kekstcnc.com

James Hartwell james.hartwell@kekstcnc.com

For the Special Committee

Gladstone Place Partners

Steve Lipin/Felipe Ucrós

212-230-5930

Curatis and Neupharma Announce Exclusive Licensing Agreement to Develop and Market Corticorelin (C-PTBE-01) for the Treatment of Peritumoral Brain Edema in Japan

Curatis Holding AG (SIX: CURN) and Neupharma Co., Ltd. (“Neupharma”), a Japanese pharmaceutical company specializing in oncology, immunology, pulmonology and cardiology disorders, today announce an exclusive license and development agreement for corticorelin (C-PTBE-01) in Japan.

Under the terms of the agreement, Neupharma will receive exclusive rights to develop and commercialize corticorelin for the treatment of peritumoral brain edema (PTBE) in Japan. PTBE is a tumor-associated condition for which no approved targeted therapies currently exist. Neupharma will finance and conduct a pivotal clinical trial in Japan to support filing for approval in Japan. Curatis will receive upfront and milestone payments for the achievement of regulatory and commercial targets totaling up to CHF 83.5 million, as well as royalties on future sales in Japan of up to 20%.

The agreement stipulates that corticorelin is planned to be introduced in Japan initially for children and adolescents. A meeting with the Japanese drug regulatory authority PMDA to discuss the registration enabling study is planned for summer 2026, and the clinical study is expected to start in 2027.

At the same time, preparatory work for the pivotal Phase 3 study for approval in the US and Europe as well as global partnering activities are proceeding as planned.

Corticorelin / C-PTBE-01

Curatis’ lead product candidate, C-PTBE-01 (corticorelin), is being developed to treat peritumoral brain edema (PTBE). PTBE occurs in association with many primary and metastatic (secondary) brain tumors, often in connection with metastases caused by lung cancer, breast cancer, melanoma and colorectal cancer. PTBE results in impairment of brain function due to the accumulation of extracellular fluid around the tumor and can cause symptoms such as headaches, vomiting and neurological dysfunction such as paralysis, speech disorders, visual problems and altered mental status. Standard of care treatment for PTBE is the use of corticosteroids which frequently have serious side effects such as severe myopathy, impaired glucose metabolism, muscle wasting, abnormal weight gain, osteoporosis, gastritis, gastrointestinal bleeding, hypertension and personality changes. Additionally, corticosteroids can also counteract certain cancer therapies such as chemotherapy or emerging immunotherapies that rely on adequate T-cell functionality which is impaired by corticosteroids.

Corticorelin (hCRH), a 41 amino acid endogenous polypeptide, has demonstrated preclinically (in vivo) the ability to positively impact the blood-brain barrier after a disruption due to the underlying malignant tumor. In two clinical studies in patients with PTBE, corticorelin demonstrated the potential to substantially reduce, or in some cases completely replace, steroid use, which may reduce or avoid the severe glucocorticoid-related side effects and subsequently improve quality of life. In the US alone, more than 150,000 patients suffer from PTBE. The estimate for the potential market opportunities for corticorelin is therefore over USD 1 billion per year. Corticorelin is an investigational drug not approved for therapeutic use in the United States or outside the United States.

About Curatis

Curatis Holding AG is a publicly listed company (CURN.SW) focused on the late stage development and commercialization of drugs for rare diseases and specialty care. Curatis has a sales portfolio of more than 40 products and a pipeline of orphan and specialty drugs. More information can be found on www.curatis.com.

About Neupharma

Neupharma is a Tokyo-based company specializing in the development, manufacture, and marketing of innovative drugs for rare and progressive diseases in Japan. The team has successfully developed and launched several products, for example in the areas of cardiology, pulmonology and oncology. For more information, visit www.neupharma.jp.

Disclaimer:

The information contained in this media release and in any link to our website indicated herein is not for use within any country or jurisdiction or by any persons where such use would constitute a violation of law. If this applies to you, you are not authorized to access or use any such information.

This media release contains “forward-looking statements” that are based on our current expectations, assumptions, estimates and projections about us and our industry. Forward-looking statements include, without limitation, any statement that may predict, forecast, indicate or imply future results, performance or achievements, and may contain the words “may”, “will”, “should”, “continue”, “believe”, “anticipate”, “expect”, “estimate”, “intend”, “project”, “plan”, “will likely continue”, “will likely result”, or words or phrases with similar meaning. Undue reliance should not be placed on such statements because, by their nature, forward-looking statements involve risks and uncertainties, including, without limitation, economic, competitive, governmental and technological factors outside of the control of Curatis Group, that may cause Curatis’ business, strategy or actual results to differ materially from the forward-looking statements (or from past results). For any factors that could cause actual results to differ materially from the forward-looking statements contained in this media release, please see the risk factors included in our listing prospectus in connection with the Business Combination. Curatis Group undertakes no obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information, future events or circumstances or otherwise. It should further be noted that past performance is not a guide to future performance. Persons requiring advice should consult an independent adviser.

The information contained in this media release is not an offer to sell or a solicitation of offers to purchase or subscribe for securities. This media release is not a prospectus within the meaning of the Swiss Financial Services Act nor a prospectus under any other applicable laws.

Some financial information in this media release has been rounded and, as a result, the figures shown as totals in this media release may vary slightly from the exact arithmetic aggregation of the figures that precede them.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260310112972/en/

Contact

Patrick Ramsauer, CFO

Phone: +41 61 927 8777

ir@curatis.com

FERM FOOD Acquires Orkla’s Former Site and Scales Up: Up to 20,000 Tonnes of Fermented Ingredients Per Year

Danish ingredient producer FERM FOOD is acquiring Orkla’s former manufacturing site in Skovlund, Denmark, effective 1 April 2026. The acquisition provides new production facilities to expand the output of fermented plant-based ingredients for the food industry — driven by export demand that has emerged faster than expected.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260310904877/en/

“We have outgrown our current facilities. With the Skovlund site, we can supply many more food manufacturers in Denmark and abroad. Global interest has developed faster than we expected — and that is why we are scaling up now,” says Jens Legarth, CEO of FERM FOOD.

Once fully ramped up, the new fermentation facility is expected to reach an annual capacity of up to 20,000 tonnes, depending on product mix, in addition to FERM FOOD’s existing capacity in Denmark (Vejen).

More functionality – fewer additives

Food manufacturers are seeking more natural ingredients that deliver functionality without expanding the ingredient list. FERM FOOD’s fermented ingredients are developed to help extend shelf life, enhance food safety and improve binding properties — while also adding nutritional value in the form of protein, vitamins, minerals and dietary fibre to finished products.

“Our fermentation technology makes it possible to use fermentation in everyday foods. It offers manufacturers a more natural ingredient solution with functionality — and a way for consumers to benefit from fermentation in mainstream products,” says Jens Legarth.

Already used in everyday products

FERM FOOD’s ingredients are already used in a range of product categories found in foodservice and in retail.

“Our ingredients are used in everyday products such as bread, ready-to-eat legumes, hybrid meat products, plant-based alternatives, binders and salads. With the Skovlund site, we are scaling up to supply fermentation-based ingredients to many more manufacturers and categories,” says Jens Legarth.

Industrial biotechnology at a global scale

Production is based on solid-state fermentation and a carefully selected mix of lactic acid bacteria. The parent company, Fermentationexperts A/S, has patented the technology and operates factories in the USA, Malaysia, Denmark and Ukraine to produce plant protein at scale. Experience from international large-scale production is part of the foundation for FERM FOOD’s 2019 launch and the company’s current scale-up.

FACTS

- Location: Nørremarken 19 and 23, Skovlund, 6823 Ansager, Denmark

- Acquisition date: 1 April 2026

- Expected capacity: Up to 20,000 tonnes/year (depending on product mix) — in addition to existing capacity in Vejen, Denmark

- Products: Fermented legumes, rapeseed press cake, kernels, oats, buckwheat, wheat and binders for food applications

- Technology: Solid-state fermentation using lactic acid bacteria is a mild processing step to break down unwanted compounds and form natural bioactive compounds that contribute to functionality in foods

- Applications: Bread and bakery, hybrid meat, plant-based foods, salads, snacks, ready meals, etc.

- Functionality: Extended shelf life, improved binding capacity, higher viscosity, better water-binding capacity, and added nutritional value through higher digestibility and improved availability of protein, vitamins, minerals and dietary fibre in finished products.

About FERM FOOD

FERM FOOD is a Danish producer of fermented plant-based ingredients for the food industry. The company uses solid-state fermentation with lactic acid bacteria to develop functional ingredients for direct use in everyday foods. FERM FOOD works to enable more natural and economically sustainable solutions across the value chain — from field to fork.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260310904877/en/

Contact

For more information, contact:

Jens Legarth, CEO, jens@ferm-food.com, +45 23 34 93 34

Abstract

FERM FOOD acquires Orkla’s former site and scales up: Up to 20,000 tonnes of fermented ingredients per year

KBRA Assigns Preliminary Ratings to NewDay Partnership Master Trust, Series 2026-1

KBRA UK (KBRA) assigns preliminary ratings to three classes of notes to be issued under the NewDay Partnership Master Trust (Master Trust), a UK credit card ABS programme backed by receivables originated by NewDay Ltd. (NewDay) and serviced by NewDay Cards Ltd.

NewDay is a UK-based consumer credit provider established in 2001 and regulated by the Financial Conduct Authority. The Company provides credit products either directly to consumers or through relationships with retail partners and serves approximately five million customers across its merchant offering and direct-to-consumer platforms. The receivables securitised through the Master Trust are limited to the merchant offering segment and consist of co-branded credit card accounts originated pursuant to agreements with individual retail partners, together with a smaller proportion of store card receivables.

The Series includes a revolving period of up to three years during which principal collections will be used to purchase additional eligible receivables. During the revolving period, and so long as a series pay-out event has not occurred, no principal payments will be made on the notes. Credit enhancement on the rated notes consists of subordination of junior note classes, excess spread generated by the pool of receivables and a liquidity reserve. The transaction also includes a minimum transferor interest which provides structural protection against dilution risk.

To access ratings and relevant documents, click here.

Click here to view the report.

Methodologies

- ABS: Credit Card ABS Global Rating Methodology

- Structured Finance: Global Structured Finance Counterparty Methodology

- ESG Global Rating Methodology

Disclosures

Further information on key credit considerations, sensitivity analyses that consider what factors can affect these credit ratings and how they could lead to an upgrade or a downgrade, and ESG factors (where they are a key driver behind the change to the credit rating or rating outlook) can be found in the full rating report referenced above.

A description of all substantially material sources that were used to prepare the credit rating and information on the methodology(ies) (inclusive of any material models and sensitivity analyses of the relevant key rating assumptions, as applicable) used in determining the credit rating is available in the Information Disclosure Form(s) located here.

Information on the meaning of each rating category can be located here.

This credit rating is endorsed by Kroll Bond Rating Agency Europe Limited for use in the European Union. Information on a credit rating’s endorsement status is available on its rating page at KBRA.com.

Further disclosures relating to this rating action are available in the Information Disclosure Form(s) referenced above. Additional information regarding KBRA policies, methodologies, rating scales and disclosures are available at www.kbra.com.

There are certain issuers, entities or transactions rated by KBRA Europe or KBRA UK that may be or have relationships with Shareholders and/or Shareholder-Related Companies, as that term is defined in KBRA’s Shareholder and Shareholder Related Companies for KBRA Europe and KBRA UK Policy and Procedure. Relevant disclosure information may be found here.

About KBRA UK

Kroll Bond Rating Agency, LLC (KBRA), one of the major credit rating agencies (CRA), is a full-service CRA registered with the U.S. Securities and Exchange Commission as an NRSRO. Kroll Bond Rating Agency Europe Limited is registered as a CRA with the European Securities and Markets Authority. Kroll Bond Rating Agency UK Limited is registered as a CRA with the UK Financial Conduct Authority. In addition, KBRA is designated as a Designated Rating Organization (DRO) by the Ontario Securities Commission for issuers of asset-backed securities to file a short form prospectus or shelf prospectus. KBRA is also recognized as a Qualified Rating Agency by Taiwan’s Financial Supervisory Commission and is recognized by the National Association of Insurance Commissioners as a Credit Rating Provider (CRP) in the U.S. Kroll Bond Rating Agency UK is located at 1 Connaught Place, 2nd Floor London, England.

Doc ID: 1013845

View source version on businesswire.com: https://www.businesswire.com/news/home/20260310135750/en/

Contact

Analytical Contacts

Irfan Surti, Associate Director (Lead Analyst)

+44 20 8148 1079

irfan.surti@kbra.com

Killian Walsh, Managing Director

+353 1 588 1184

killian.walsh@kbra.com

John Hogan, Co-Head of Europe (Rating Committee Chair)

+353 1 588 1191

john.hogan@kbra.com

Business Development Contacts

Miten Amin, Managing Director

+44 20 8148 1002

miten.amin@kbra.com

Mauricio Noé, Co-Head of Europe

+44 20 8148 1010

mauricio.noe@kbra.com

Forbes 40th Annual World’s Billionaires List

Forbes releases its 40th-annual World’s Billionaires list, the definitive ranking of the planet’s richest people. Wealth surged to unprecedented levels over the past year, with fortunes climbing at a record pace. This year’s list features 3,428 billionaires, the most since the list’s inception in 1987. The world’s wealthiest people are worth a record $20.1 trillion combined, up from $16.1 trillion in 2025.

Elon Musk tops the Billionaires list for the second year in a row and is the richest person ever recorded, worth an estimated $839 billion. His net worth skyrocketed by half of a trillion dollars from last year, thanks to a rise in the value of Tesla, and SpaceX which is aiming to go public in 2026. Musk is the first person ever recorded to reach the $800 billion mark, as he moves toward becoming the world’s first trillionaire.

“It’s the year of the billionaire,” said Chase Peterson-Withorn, Forbes Senior Editor, Wealth. “The planet added more than one billionaire per day over the past twelve months as the AI-powered stock market boom boosted fortunes to previously unimaginable heights.”

Larry Page, cofounder of Google, follows far behind Musk, in the No. 2 spot with an estimated net worth of $257 billion, followed by his cofounder Sergey Brin at No. 3 ($237 billion). Jeff Bezos holds the No. 4 spot ($224 billion) and Mark Zuckerberg ($222 billion) rounds out the top 5.

President Donald Trump’s fortune increased by 27%, to an estimated $6.5 billion, thanks largely to crypto dealings and his New York fraud penalty being thrown out. He ranks No. 645 worldwide.

The 2026 ranking features 390 newcomers, including Dr. Dre; Beyonce Knowles-Carter; and tennis legend Roger Federer.

The United States has more billionaires than any other country, now boasting a record 989.

For the full list, visit: www.forbes.com/billionaires.

About Forbes

Forbes is an iconic global media brand that has symbolized success for over a century. Fueled by journalism that informs and inspires, Forbes spotlights the doers and doings shaping industries, achieving success and making an impact on the world. The Forbes brand reaches more than 140 million people monthly worldwide through its trusted journalism, signature ForbesLive events and 49 licensed local editions in 81 countries.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260310629058/en/

Contact

Media Contact:

Feryal Nawaz, fnawaz@forbes.com

Language Weaver Brings Secure AI Translation Directly Into iManage Work Legal Workflows

LEGALWEEK– RWS (RWS.L), a global AI solutions company, today announced the upcoming launch of its Language Weaver integration for iManage Work, giving legal professionals the ability to translate documents instantly and securely without leaving their trusted document management environment.

The new integration embeds Language Weaver’s AI directly within the iManage Work environment for enterprise-scale translation. Legal professionals can instantly translate contracts, briefs, emails, presentations and other business-critical documents in context, with a single click – no downloads, uploads or platform switching required.

“Our partnership with iManage gives firms a decisive competitive edge by enabling secure multilingual content management directly within the platform their legal professionals use every day,” said Heather Rossi, Solutions Consultant at RWS. “Firms can accelerate cross-border M&A, streamline global contract negotiations, and manage multi-jurisdictional compliance — without exposing sensitive information to external translation tools. The integration strengthens global reach, enhances client service, and allows translations to be tracked by matter or client code, all while upholding the highest standards of security and auditability.”

Language Weaver is a secure, AI-powered neural machine translation platform, designed for enterprise, legal and government use. It provides fast, high-quality, and scalable translation across 4,400+ language combinations, supporting secure on-premise (Edge) and cloud-based deployments to handle sensitive data.

“Legal work increasingly spans jurisdictions, languages, and teams,” said Paul Bower, AI Director at iManage. “Embedding Language Weaver directly within iManage Work allows firms to translate sensitive documents inside governed workflows – preserving security, auditability, and matter context they depend on. This integration reflects our commitment to engendering AI Confidence – in this case, by ensuring translation workflows leverage AI without risking security or governance.”

Available in March, the Language Weaver integration for iManage Work expands RWS’s ecosystem of connected content solutions.

Click here to learn more.

About us

RWS is a global AI solutions company empowering the world’s most trusted enterprise AI.

Our proprietary Cultural Intelligence Layer, powered by 250,000 data specialists, cultural and language experts and deep domain professionals, backed by 45+ patents, makes enterprise AI culturally fluent, contextually accurate and secure, ensuring every interaction reflects a brand’s tone, context and customer values.

Through our Generate, Transform and Protect segments, we deliver intelligent content, enterprise knowledge, large-scale localization and IP protection for global growth. Trusted by 80+ of the world’s top 100 brands, RWS provides the confidence, governance and expertise organizations need to deploy AI safely, responsibly and at scale.

Headquartered in the UK, RWS is listed on AIM.

More information: rws.com.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260310342959/en/

Contact

RWS

Denis Davies

Corporate Communications

ddavies@rws.com

+44 1628 410105

Octus Unveils a Unified CreditAI Experience: The First-Ever, Compliance-Ready Generative AI Search for Both Public and Private Data Targeted Specifically for the Global Credit Markets

OctusⓇ, the essential credit platform for the world’s leading buy-side firms, investment banks, law firms and advisory firms, today announces the next phase of its AI strategy with CreditAI by OctusⓇ (“CreditAI”). As tier-one global financial institutions, buy-side, law and advisory firms invest in and develop AI and AI-Agentic workflows for their employees, Octus is leading the industry by moving beyond commoditized, generic models and tools focused on publicly available information and content. CreditAI turns unstructured and complex data into the clear, accurate insights credit professionals need to accelerate decision-making.

The new CreditAI experience is transforming and leveraging the way credit professionals around the world consume and act on information by building a world-class generative AI search that combines Octus’ proprietary intelligence and data, as well as information not indexed by traditional LLMs, including private, permissioned data room documents, broadly syndicated loan and private credit agreements, and financials on non-publicly traded bond and loan issuers in an auditable, source-verified, compliant environment.

“The financial world needs to move beyond commoditized AI that produces too much ‘AI fluff’ and not enough detail and specifics that credit professionals rely on. Generic AI models are a risk for anyone advising a borrower or lender or investors managing billions in capital,” said Kent Collier, founder and CEO of Octus. “These broad-based AI models do not possess the underlying ingredients or the domain-specific and context-verified training, rendering results virtually meaningless. With CreditAI, we are giving firms the authoritative intelligence and hard-to-find data along with a model trained and built by credit experts that know the credit professionals’ workflow. As an example, our agentic AI model focused on covenant analysis has over a dozen agents working off of over 10,000 prompts finely tuned to meet the demands of anyone analyzing, in detail, a controversial credit agreement. Put that same credit agreement in a generic LLM and you will get an answer that would be negligent to rely upon.”

The Problem: Generic AI Models Are Not Trained on Verifiable Credit Industry or Legal Data

CreditAI establishes a new benchmark for accountable and accurate AI in leveraged finance, with the largest “non-public” vector store, trained on specified data and with expert, human-validated model training and output.

“While many firms have experimented with generic AI tools to improve productivity, generic models lack the domain-specific ingredients required to handle the complexities of the credit market,” says Vishal Saxena, CTO of Octus. “Ultimately, in this multi-trillion-dollar regulated industry, using generic AI models leads to burning inaccuracies in high-stakes deal-making. We’ve completely changed the game with CreditAI, with a credible, compliance-safe solution.”

CreditAI by Octus: Intelligence That Passes the Trust Test

Because Octus manages the largest library of leveraged finance data, the largest private document repository, expansive public and private datasets, and the deepest and most rigorous financial and legal analyses, it can demonstrate a validation trail and ensure citation accuracy in every AI query and response, back to the underlying source documentation.

The unified CreditAI now delivers four critical pillars of “accountable AI”:

- Public content (foundational output and context): Available to all Octus users, trained using generative AI and LLMs to surface insights across public-company and public Octus-validated intelligence.

- Data room content (the private-public nexus): Proprietary and permissioned data sets are directly searchable alongside Octus public intelligence, keeping sensitive deal documents strictly secured while users gain the advantage of market-wide context. By utilizing rigorous permissioning protocols, CreditAI directly addresses the industry’s compliance and fiduciary requirements for private data.

- Covenant content (lawyer-trained): An agentic AI brain, trained by Octus’ senior legal and financial analysts to generate insights from a “legal-nuanced” data set (ie, covenants, contracts and court filings). This deeper and very specific, permissioned use case helps credit professionals spot liability management vulnerabilities, such as uptiering and drop-downs, or specific covenants clauses or language that generic models routinely miss.

- Structured data (precision tuning): Validated credit and situation-specific data, including fundamental data, is incorporated into users’ search responses to improve output. CreditAI accesses credit details including the capital structure, transaction and financial details, sponsor, and as-reported and standardized financials.

Grounded in Human Acumen

CreditAI synthesizes the collective expertise of Octus’ financial, legal and data scientists to deliver precise insights from the underlying content sets. To ensure total transparency, every response links to source documents for instant verification.

“We designed CreditAI with compliance readiness as its core foundation, specifically addressing the stringent compliance and security requirements of the highly-regulated financial services industry,” stated Sreekanth Mallikarjun, Ph.D., Chief Scientist and Head of AI Innovation at Octus. “Our shift has been from AI as a ‘suggestive tool’ to a workflow essential. This agentic AI uses multiple domain-specific skills and chain-of-verification process, based on expert-in-loop validation, training and data sourcing, to bring us closer to achieving artificial general intelligence within the credit market.”

About Octus

Founded in 2013, Octus is the essential credit intelligence, data and workflow provider for the world’s leading buy-side firms, investment banks, law firms and advisory firms. By surrounding unparalleled human expertise with proven technology, data and AI tools, Octus unlocks powerful truths that fuel decisive action across financial markets. Visit octus.com to learn how Octus delivers rigorously verified intelligence at speed and creates a complete picture across the credit lifecycle. Follow Octus on LinkedIn and X.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260310334038/en/

Contact

Media Contacts

Drake Manning — drake.manning@octus.com

Mike Deleo — OctusPR@icrinc.com