Pension savers hoping for ’74 per cent of salary’ in retirement may face a shock

After a lifetime of saving, investors may be in for a shock when they come to retire, the results of a global study suggest.

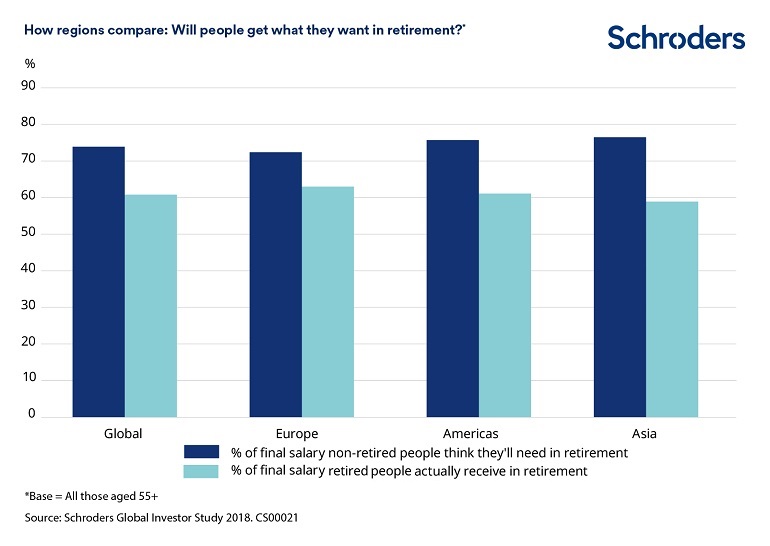

Investors close to retirement (aged 55 and over) expect they will need income equivalent to 73.9 per cent of their current salary to afford to live comfortably in retirement.

But those already retired say the average amount they actually receive is far less, at 60.8 per cent of their final salary. On average, 85 per cent said this was sufficient but 58 per cent also said they could use a little more money.

These were among the key findings of the Schroders Global Investor Study (GIS) 2018, which surveyed more than 22,000 investors across 30 countries.

Expectations for the income needed for retirement varied geographically with non-retired investors in some countries – Poland and Indonesia – believing that they will need more than 100 per cent of their salary for a comfortable retirement. Those already retired typically receive far less, as shown in the table below.

Across regions, investors in Asia and the Americas expect to need the highest replacement rate, believing they will need three-quarters of their current salary.

You can find a full comparison between all the countries we surveyed in the table below.

Global Investor Study: Read the full findings

Global Investor Study: Why 70 per cent of people keep investing after retirement

How much are savers putting away for retirement?

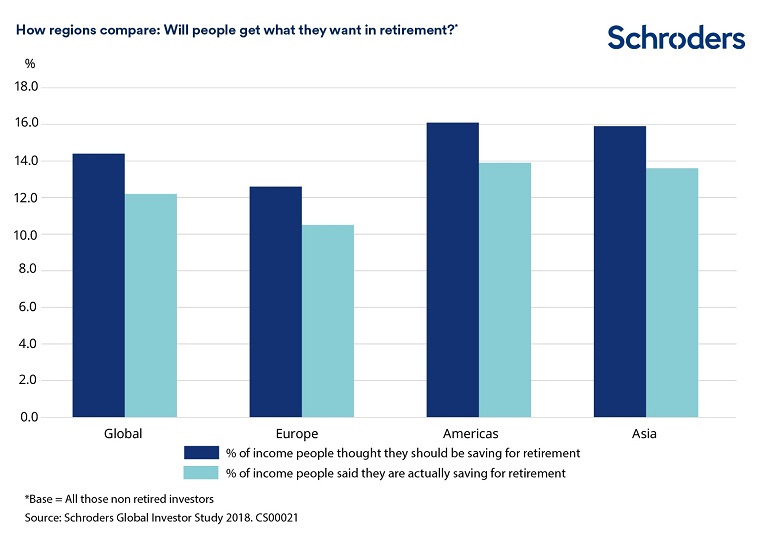

The amount of income investors can expect in retirement is dependent on a range of factors but one of the most important is the rate at which people put money away.

The average investor saves 12.2 per cent of their current salary for retirement. However, that is less than the 14.4 per cent they think should be saving to reach their target.

The rate varies regionally. In Europe, non-retired Belgians save the least (9.2 per cent) as a percentage of their current salary to fund retirement and the Danes say they save the most (12.5 per cent). In Asia, people in Hong Kong save just 10.9 per cent of their current salary for retirement compared with 15.3 per cent for Singaporeans. In the Americas, Canadians save the least (11.9 per cent), while the US saves the most (15.4 per cent).

The gap between what people are saving and what they think they should be saving was widest in developing economies. For example, people in Chile are currently saving 12.8 per cent of their current salary but think they should be saving 19.2 per cent, a difference of 6.4 per cent.

The only people currently saving more than they thought needed were the Danish, 12.5 per cent vs 12.3 per cent.

You can find a full comparison between all the countries we surveyed in the table below.

Lesley-Ann Morgan, Head of Retirement at Schroders, said: “There is a clear difference between the level of income retirees are receiving and what those nearing retirement are expecting to achieve. This gap could lead to disappointment if some over 55s do not have savings to support the lifestyle they would like in retirement.

“However, investors recognise the need to save more if they are going to achieve the standard of living they want in retirement. Saving more is particularly important in the current environment of low returns and increasing inflation, making it harder to both grow savings and produce income in retirement.

“To have the best chance of a comfortable retirement, the lesson for younger workers is start saving early. Leaving retirement saving until you are nearing your 50s and 60s is likely to be too late to make up a savings gap. As our analysis shows, a person in their 20s will likely need to save between 10 per cent and 14 per cent of their salary each year if they want to retire on a minimum of 50 per cent of their salary.”

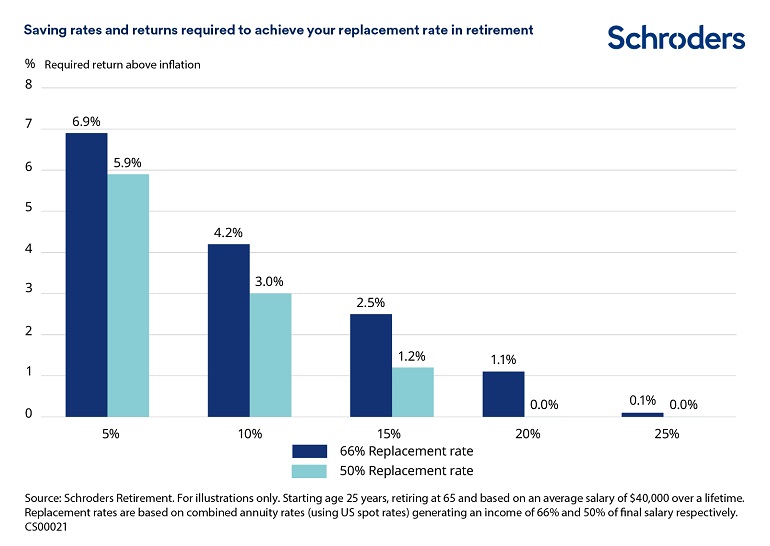

How much you need to save, depending on returns achieved

Calculating the right amount to save for retirement is a challenge for investors. The final savings total and the income it will provide, are affected by a range of factors. It is not just about how much you save but it is determined by the returns you achieve and the amount of time you’re invested.

You also need to consider how much you want your pension income to be compared to your working income. This largely comes down to the lifestyle you want in retirement and how much of this your country’s government pension will provide. Our study shows that globally investors are aiming for a 74 per cent replacement rate. This is relatively high against most financial planning modelling. For example, future net replacement rates (including government provision) average 63 per cent among OECD countries, according to OECD and G20 indicators.

The model developed by Schroders, below, shows the level of investment returns needed to achieve replacement rates of 66 per cent and 50 per cent, assuming this is being funded by private savings alone. It is based on the rates of retirement income available today from a guaranteed annuity. The scenarios will vary if you choose instead to keep the money invested or take it as a cash lump sum.

To explain one scenario, if someone saves 15 per cent of their salary from the age of 25 and wants to retire at 65, they would require an average annual return of 2.5 per cent above inflation (the middle column) to achieve a retirement income worth 66 per cent of their working income. If they contributed 10 per cent of their income, however, they would need a return of 4.2 per cent above inflation.

It’s worth noting that if you only save 5 per cent of your salary from age 25, you may need returns that exceed inflation by 7 per cent to create a retirement account large enough to replace 66 per cent of your salary, based on today’s rates of annuity income.

To put that into perspective, the Credit Suisse Investment Returns Yearbook shows that over the last 118 years, global equities have delivered annual real returns (taking inflation into account) of 5.2 per cent. While it is difficult to forecast future returns accurately, the Schroders Economics Group expects that, given the current environment and future growth prospects, lower average returns above inflation of 3.8 per cent a year are likely from global stockmarkets over the next 30 years.

- Global Investor Study: Read the full findings

- Global Investor Study: Why 70% of people keep investing after retirement

Schroders commissioned Research Plus Ltd to conduct, between 20th March and 23rd April 2018, an independent online study of over 22,000 people in 30 countries around the world, including Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, the Netherlands, Spain, UAE, the UK and the US. This research defines “people” as those who will be investing at least €10,000 (or the equivalent) in the next 12 months and who have made changes to their investments within the last 10 years.

Important Information: The views and opinions contained herein are of those named in the article and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.