Party like it’s 1999

Mergers and acquisitions are back and they’re almost as lucrative as they were during the last feverish round.

It’s a throwback to the turn of the century: multibillion pound mergers are announced by the day, the stock market is soaring, city pubs and wine bars are buzzing. All that’s missing is the sight of grown men tooling around town on micro scooters.

Astonishingly, four takeover bids were announced on Monday; the targets boast a combined stock market capitalisation of over £23bn. Leading the way was Telefonica, once Spain’s state-owned telephone company, bidding nearly £18bn for O2, spun off from BT. Ports company P&O admitted to an approach from the Dubai-based DP World, owned by the government of the United Arab Emirates. Japan’s Nippon Sheet Glass is negotiating to buy the 80 per cent of British glass manufacturer Pilkington that it doesn’t already own, while building firm Mowlem admitted to a £270m bid from a mystery suitor.

The resurgence of takeover fever sent the FTSE 100 index more than 100 points higher, its best one-day gain in more than two years. The buying continued yesterday, with the benchmark adding another 27 points to close at 5344.30.

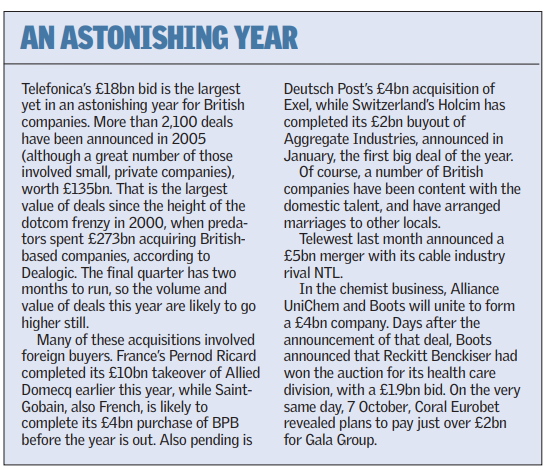

Deals totalling £40bn have been struck in the first month of the quarter, the most prolific three-month period since the third quarter of last year, according to M&A consultancy Dealogic.

With two months left to run before the end of the year and merger mania showing no sign of let up, this quarter could mark a return to the heady days of 2000. More than £100bn worth of deals involving British companies were announced in the first quarter of 2000, but merger and acquisition activity fell sharply over the following years. M&A deals involving a British company, totalled just under £11bn by the third quarter of 2003.

Of course, there are vast differences between 1999 and 2005, not least that the business suit has made a welcome return to the streets of the Square Mile. Experts believe that this latest wave of deals has been prompted by compelling commercial circumstances. “There is a strategic logic and rationale to the deals being done in 2005,” said an M&A expert at a large investment bank. For example, the Telefonica-O2 deal “is a good move. It’s fair to all concerned,” he added.

In fact, this wave of takeovers stems from the reorganisation plans implemented after the burst of the dotcom bubble in 2000. After the stock market collapsed, companies were forced to clean up balance sheets marred by assets acquired at vastly inflated prices. “Companies had to do a huge amount of de-leveraging,” the M&A expert said. That done, many bowed to the wishes of large institutional shareholders and returned cash to investors.

Now the institutions are pushing these more streamlined companies to expand their business; mergers are a way to do that in a hurry.

Furthermore, with nominal interest rates low throughout the developed world debt financing is cheap, say M&A analysts. The most attractive targets, mobile phone companies like O2, generate a large volume of cash. “The cash flow is terrific; (acquiring firms) can de-leverage pretty quickly,” said one.

And most recent deals have been for cash, rather than the over-inflated shares of the late 1990s. But even though a cash offer implies a degree of strength on the part of the buyer, cash deals can come unstuck. Had Marconi used its shares to pay for the string of disastrous acquisitions a few years back, it might not have fallen into the hands of Sweden’s Ericsson last week.

British firms are particularly attractive because regulators here are not concerned about protecting national champions, as are many governments in continental Europe.

Remember the fuss in France over the summer, when the markets were buzzing with talk that America’s Pepsi was possibly mulling a bid for yoghurt maker Danone? “Our regulatory authorities are a lot less strict than elsewhere,” said Michael Maclure, an analyst at Dealogic, asking rhetorically: “Would Deutsche Telekom come up for sale?”

With European companies cash rich, and debt financing easy to come by, more mega-mergers are on the horizon. “British success stories are up for sale,” Maclure said.