What ‘dividend cover’ says about the safety of stock market income

The income paid by stock market companies to investors could be about to come under pressure.

The twice yearly payments made to investors can be a vital income supplement for those in retirement. Others reinvest the dividends to boost long-term returns.

But research compiled by Schroders shows European and US companies are diverting a high proportion of their profits into dividends, raising questions about the sustainability of current levels of income.

Given this backdrop, income investors could benefit from watching a ratio known as “dividend cover”.

This a multiple by which a company’s earnings exceed its dividend payments. It can also be applied to an index.

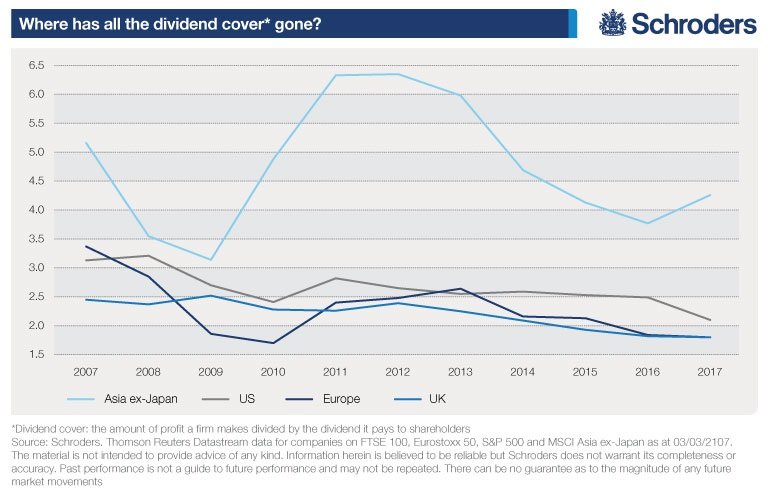

A decade ago, profits would cover dividends more than three times over in most regions. However, dividend cover has declined over the last 10 years, amid some ups and downs, to historically low levels.

In both the UK and Europe dividend cover has fallen to 1.8 times, according to data from Thomson Reuters Datastream. Ten years ago, it was at 2.5 and 3.4, respectively.

In the US, dividend cover has fallen from 3.1 to 2.1. In Asia, dividend cover has fallen from 5.2 to 4.3.

A company with a dividend cover below two has less room to manoeuvre on dividend payments. If profits fall the management is often faced with a choice of reinvesting less in the business, borrowing to pay a dividend, or they can simply cut the dividend.

In the UK, high profile cases of companies cutting or cancelling dividends as a result of a slump in profits include energy firm BP and insurer RSA. In Europe debt problems sealed the fate of Spanish telecoms group Telefonica’s dividend, which it was forced to cut.

A dividend cover below one should sound alarm bells. It means that companies are not making enough money to pay their dividend.

Why do dividends matter?

Increasingly dividends are becoming an essential part of an investor’s portfolio. They could be used to help pay school fees, supplement monthly wages in work or fund retirement.

Expectations are high. The latest Schroders Global Investor Study, which collected the views of 20,000 investors in 28 countries, found that investors, on average, would like an annual income of 9.1% from their investments.

Globally, interest rates are exceptionally low. Investors would be lucky to earn savings interest of 1% in most developed countries and many bond markets, traditionally a favoured way of earning income, pay very little.

- Test your investor psychology with our Income IQ test

These factors have helped drive income investors to stock markets. In the UK, the yield on 10-year government bonds was around 1.2% at the start of March, but the FTSE All-Share was yielding income of around 3.5%. In Germany, bonds were yielding 0.3% while the DAX offered 2.3%.

Arguably, dividends are the most important weapon.

For example, between 1900 and 2012 UK shares would have returned just 0.6% a year in the absence of dividends, according to a study by the London Business School. With dividends, the annual return was 5.2%. The figures also factor in the effects of inflation.

So, while headlines scream "stock markets at new all-time highs", it is the dividend payments you should pay more attention to.

Should I be worried about my dividend income?

In Europe, dividend cover has nearly halved to 1.8 over the past decade. In the US it has fallen 33% to 2.1 and by 26.4% to 1.8 for the UK. In Asia dividend cover is down 17.3% to 4.3.

Data is available for companies that were included in the indexes then and now.

In Europe dividend cover has fallen for 38 of the 48 companies the last 10 years. In the US it is 45 of 52, in Asia it is 295 out 465, while the UK shows dividend coverage has declined for 60 out of 78 companies.

Falling dividend coverage, however, does not necessarily mean that income investors should steer clear of a company. For instance, US bank Goldman Sachs’ dividend coverage has fallen 55% in the last decade but it can still cover its dividend 6.3 times.

It works the same the other way too. For example, Italian utility ENEL has improved its dividend cover 103%, but still has a dividend cover of less than two.

There can be a number of reasons for declines and rises in dividend cover and it is only one measure of many to consider when making investment decisions.

Fund managers will undertake comprehensive analysis of a wide range of factors. Individual investors should consider taking professional advice.

Important Information: The views and opinions contained herein are those of David Brett, Investment Writer and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.