Cash holdings: UK corporates’ £109bn warchest increasingly a rival to private equity in M&A

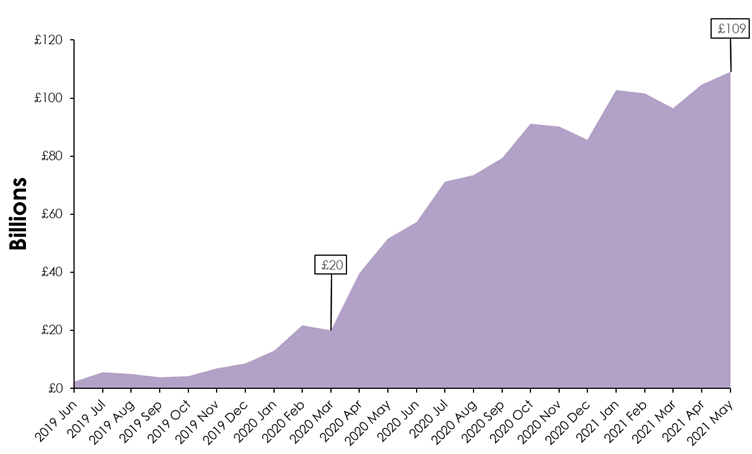

UK corporates have seen their aggregate net cash holdings rise from £20bn to £109bn since March 2020 and the start of the Covid pandemic, a jump of 500 per cent.

The build up in cash balances has been so dramatic that UK corporates are increasingly seen as a serious rival to private equity funds in targeting undervalued UK businesses, according to analysis from debt advisory ACP Altenburg Advisory, shared with City A.M. today.

While private equity firms are actively looking to acquire attractive British companies, privately owned and listed UK corporates have been much more cautious during the pandemic, with their core focus being on their existing businesses.

Total UK corporations net cash holdings (cash minus debt – excludes financial services businesses)

Private equity

Merger and acquisition (M&A) activity is at an all time high as private equity firms have had their busiest six months since records began over four decades ago.

There have been 366 bids for UK companies from buyout groups this year, the most for a comparable period since records began in the 1980s. Private Equity firms are looking to benefit from UK companies’ lower valuations resulting from the combined impacts of Brexit and Covid.

This comes as private investment groups have agreed a £9.5bn takeover of Morrisons – in what could be the country’s largest UK private equity buyout since KKR bought Boots in 2007.

Firepower

In addition to the private equity frenzy, among lenders there is a strong appetite to help corporates looking to acquire UK businesses.

By using a mix of balance sheet cash and debt funding, corporates can appropriately leverage a deal in order to compete with a private equity bidder, explained Will Senbanjo, partner at ACP Altenburg Advisory.

“We are in a period of intense M&A activity and corporates will be wondering if it is right to leave so many of these deals to the Private Equity funds,” Senbanjo told City A.M.

“Corporates could be making more use of the cash they are holding, as investing their own cash alongside debt increases the alignment between companies and their funding partners and thus the number of debt options available,” he continued.

“A bid from a corporate can be more suitable for certain businesses and more attractive to vendors, if they can obtain funding that allows them to compete with private equity on valuations.”

“Some owners may prefer to sell to other corporates , given the perception that they may offer more continuity and less organisational restructuring than other options,” Senbanjo noted.

This rise in corporate cash may provide opportunities for management teams considering a management buyout or moving to an employee ownership model to progress a deal.

The reserve of corporate cash can be used alongside funding from lenders to pay out existing owners and facilitate the sale.

“Lenders are busy at the moment given the heightened activity in the M&A market, but they are keen to diversify by funding non-PE owned corporates,” Senbanjo concluded.