Why companies that cut their dividend can be attractive income investments

An important part of income investing is receiving dividends. A dividend is the portion of a company’s profits that is returned to shareholders.

The payment of dividends is an incentive to own shares in stable companies. Often, companies paying attractive dividends will be those that no longer benefit from reinvesting their profits, whereas companies with significant growth opportunities tend to use their profits to grow the business.

The attraction for income investors is clear: the dividend payment is a consistent return on investment. But what happens if a company needs to cut its dividend?

Why do companies cut dividends?

Dividend cuts can happen for a variety of reasons. On some occasions, a company may see an opportunity to reinvest in its business – perhaps via an acquisition – rather than pay the dividend.

More often, it is due to declining profits. Companies may be able to maintain their dividends for a while, but if profits continue to decline then eventually their capacity to pay those dividends will be constrained.

Companies may decide to reduce their pay-out ratio (i.e. the proportion of profits paid in dividends) or pay in shares rather than cash (known as a scrip dividend). For example, Royal Dutch Shell introduced a scrip dividend after the oil price crash in 2014 in order to reduce cash outflows, and only restored it to cash in November 2017.

In a worst-case scenario companies may stop the dividend payment entirely.

Why might this be good news?

On the surface of it, a dividend cut is not good news at all for shareholders and a company’s share price will generally fall when a dividend cut is announced.

However, cutting the dividend can be a very sensible move. Trying to maintain dividend payments at an unsustainably high level can be much worse in the long-term for the company (and its shareholders) than temporarily suspending or cutting the dividend.

- Where to invest in Europe

- How stock markets react after big falls

- What will drive future stock market returns?

Indeed, if a company has to borrow in order to pay its dividend then it could be storing up serious problems for the future.

Cutting the dividend is often among the first steps a company might take in order to try and regain financial stability.

A decision over cutting the dividend can come down to whether company management is focusing on the long-term health of the business, or the short-term impact on the share price.

For long-term investors, it is preferable that a company cuts its dividend to protect its balance sheet, or to invest in the business, rather than paying an unsustainable dividend at all costs.

Dividend cutters can offer value

Short-term investors who are simply in search of the highest dividends often sell their shares once a company cuts its dividend. This can offer an opportunity for long-term, value-focused investors to buy shares at a price they deem attractive.

Then, in theory at least, the company management puts the business on a more sustainable footing, dividend payments restart and the share price recovers. Such a scenario can be an opportunity for investors to participate in both a growing dividend and a rising share price.

Even when already invested in a company that has cut its dividend, it can make sense to continue to hold the shares, if the dividend cut is in the best long-term interests of the company.

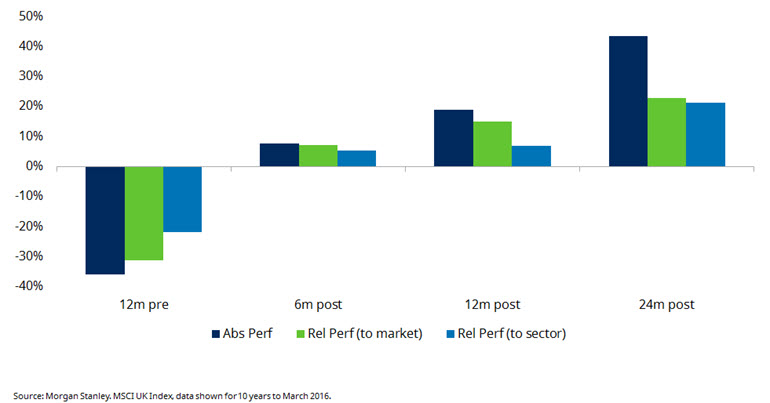

The chart below illustrates how share prices come under pressure when a company’s dividend is thought to be in danger, but also that share prices often swiftly recover once the cut has been made.

Dividend cuts: a threat, but also an opportunity

Past performance is not a guide to future performance and may not be repeated.

Simon Adler, an equity value fund manager at Schroders, said: “We would never tell a company what its dividend should or should not be. Instead, we prefer to afford the management teams of companies in which we invest the space and the confidence to cut their dividend if they feel it is unsustainable or the money is better spent elsewhere.

“Far better it take that approach than overstretch its balance sheet to pay a dividend it cannot afford.

“That, incidentally, is a situation in which many of the high-paying so-called ‘bond proxy’ businesses are in increasing danger of finding themselves. Many are currently terrified of what disappointed investors could do to their share price if they cut their dividends.”

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

Important Information: The views and opinions contained herein are those of Emma Stevenson, Investment Writer, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.