These six charts caught our attention in July

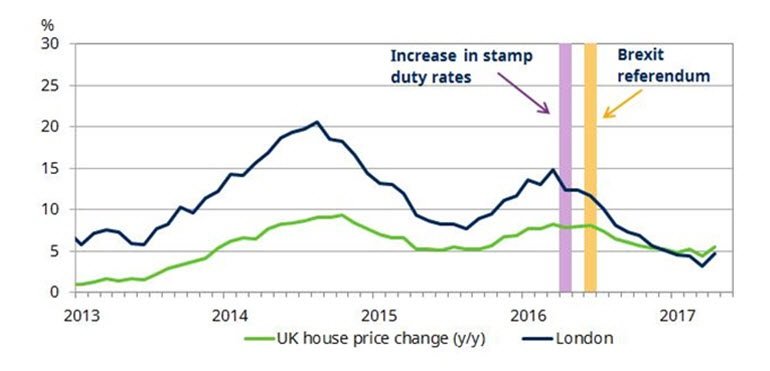

Safe as houses

In the UK, house price growth began to slow noticeably last year when stamp duty on buy-to-let and second homes increased. The slowdown continued after the announcement that the UK would be leaving the EU. Perhaps surprisingly, London has been hit harder than the rest of the UK.

- UK growth is sluggish but will it deter the Bank of England from hiking rates?

After the financial crisis, London property prices recovered more sharply than in the rest of the UK. But part of the reason property values in London are higher is due to the city’s status as a global financial hub; somewhat less certain now that Brexit negotiations have begun.

However, there is probably no need to worry yet. Demand still significantly outstrips supply in the UK. Schroders research indicates the country fell some 65,000 houses short in 2016, which should see prices supported.

Source: Schroders Economics Group, July 2017.

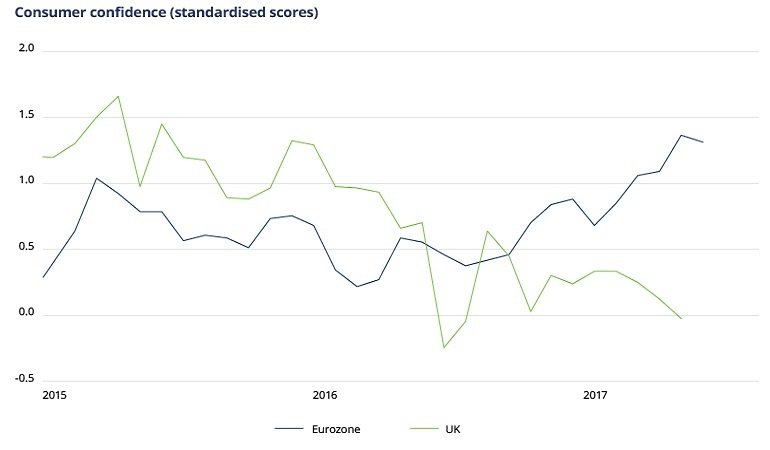

Feeling confident?

Consumer confidence readings in the UK and eurozone have diverged significantly since the start of this year. Confidence has been on the rise among eurozone consumers as economic data in the single currency area has been encouraging and unemployment is falling. Perhaps most importantly, political risk has eased considerably with Emmanuel Macron’s victory in the French elections.

By contrast, UK consumers have been facing slower nominal wage growth and higher inflation. Meanwhile, the political picture has been muddied by the ruling Conservative Party losing its parliamentary majority after calling a snap general election. And finally, there continues to be considerable uncertainty over how Brexit will play out.

Source: Schroders Economics Group, July 2017.

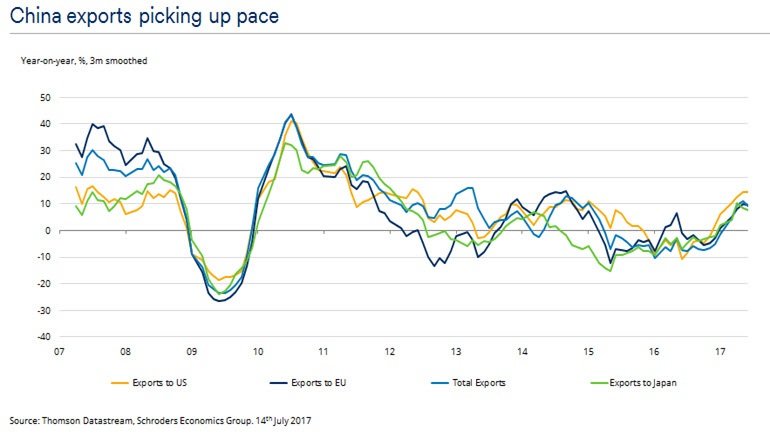

Trading up

China’s June trade numbers aptly illustrate that a globally-synchronised recovery is underway, with the country’s exports commonly seen as a barometer of global demand.

Exports to the US, Japan and Europe all accelerated in June (with a particularly strong pickup in the US). Although June exports to emerging markets were marginally softer, the overall growth trend for the global economy is encouraging.

This is because this most recent upturn in Chinese export growth, unlike the post-Global Financial Crisis spike, has not been driven by massive fiscal stimulus programmes or globally loose monetary policies. In fact, it has been quite the opposite. Recent growth has come amid rising interest rates in the US and the possibility of tightening in the eurozone – suggesting demand could be building up genuine momentum.

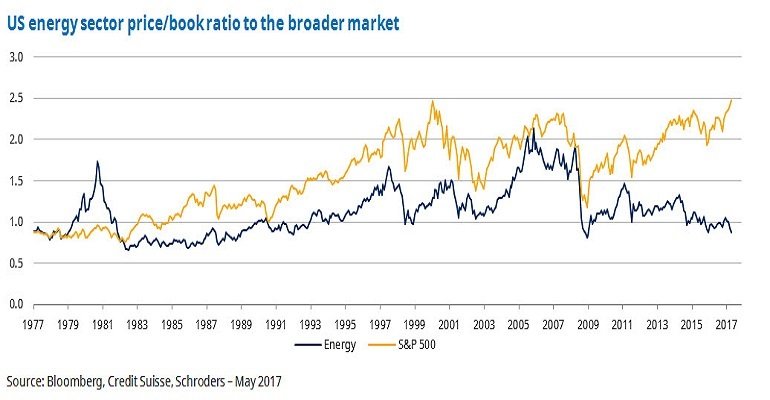

Is the US energy sector cheap?

The valuation of the US energy sector has been falling. The price-to-book (P/B) ratio used in the chart below compares the sector's share price with the value of its assets (minus its liabilities). If a company has a P/B less than one, it could be undervalued compared to its assets.

With the US oil sector currently valued so cheaply compared to the rest of the market, there may be a temptation to buy in the expectation that oil company share prices will recover. But what would drive such as recovery? Many investors look for an “inflection point”, such as cost-cuts, that could lead to improved returns and a higher share price. Unless such an inflection point can be identified, it could be that oil companies look cheap for good reason.

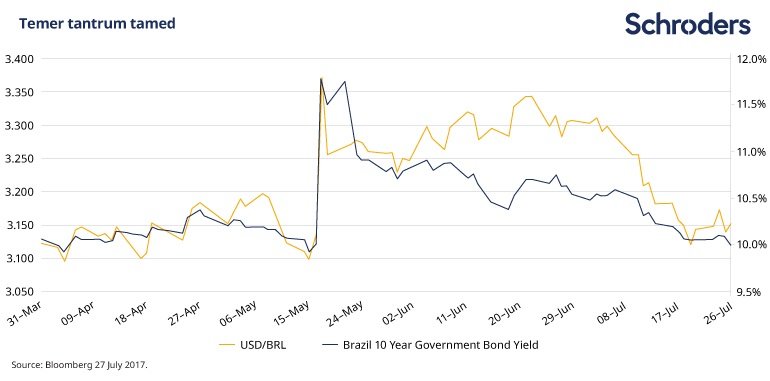

Temer tantrum tamed

Yields on Brazilian government bonds declined and the real recovered against the US dollar in July. It follows a sharp increase in political risk in May, as allegations of corruption were levelled at President Temer.

The government successfully passed labour reforms, easing concern that support for Temer’s reform agenda had waned. Meanwhile, former President Luiz Inácio Lula da Silva was convicted of corruption, likely prohibiting his participation in 2018 presidential elections. This dims the chances of a return to power for the leftist Workers Party. Further, inflation fell more than forecast to 3%, and the central bank cut rates another 1%.

A congressional vote on whether to send the President’s corruption case to the Supreme Court is expected in early August. Although markets have taken the view that this is unlikely to pass, Brazilian assets may see some volatility as we get closer to the vote. Meanwhile, the outlook for the key pension reform remains uncertain.

Dollar decline gathers pace

The year-to-date decline in the US dollar took on added momentum in late June. Central bank chiefs in the US, UK and Europe each made comments taken as signalling increased hawkishness. Government bond yields were jolted higher, particularly in Europe, and the US dollar hit turbulence (see the chart of the DXY index: measuring the US dollar against a basket of currencies). The greenback’s decline was most pronounced against the euro, which comprises about half of the DXY index, suggesting the market was failing to price the tapering of quantitative easing in Europe.

The past six months had seen a gradual erosion of confidence in the dollar amid a growing disillusionment with the prospect of President Trump enacting his pro-growth policies. July has seen further downward pressure as Federal Reserve Chair Janet Yellen expressed surprise at continued weakness in inflation, which indeed continues to puzzle given employment levels.

For more from Schroders visit their website and follow them on twitter

Important Information: The views and opinions contained herein are those of Schroders Investment Communications Team, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.