Marcus Brookes: How we’ve prepared for the return of inflation

Inflation was already on the rise. Now I expect the policies likely to follow in Donald Trump’s presidency will pile on further price pressure.

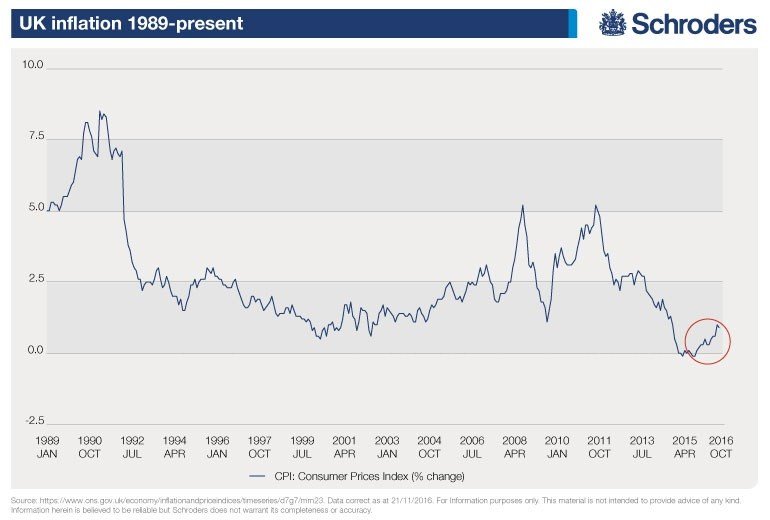

The deflating effect of QE

We have been changing our portfolios over the last year to reflect our view that inflation may be returning to the financial system.

Yes, quantitative easing, designed to encourage inflation, had largely failed. Adding money to the system was designed to encourage borrowing, but everyone still had problems paying off debts from the financial crisis, so they were not interested in borrowing even more money at any cost. Inflation, as a result has remained exceptionally low.

However, after eight years of healing the global economy is showing signs of stability, even in areas that had been hardest hit, such as Europe.

Is the story changing?

While our view has shifted, the “lower for longer” stance remains entrenched in the mind of other investors. The phrase encapsulates the view that economic growth will remain weak and therefore inflation and interest rates will stay lower for a far longer spell than is usual. It’s been the correct view so far.

The change that we have begun to observe, though, is that some areas are seeing better-than-expected trends. It leads to the conclusion that economic growth may be about to tick up, not by a lot, but enough to change the story on inflation.

Consider employment data. In both the US and UK we are seeing unemployment of around 5%, which may seem high to non-economists but actually represents very close to full employment in the view of central banks and policymakers.

Why might this impact inflation?

Consider the situation of a small pick-up in economic activity; the entrepreneur is able to sell more goods and services, which necessitates expanding the business to be able to meet customer demand, which might require hiring more staff, but the pool of freely available labour is empty, so it becomes necessary to poach someone from an existing job.

This will only be achieved if the entrepreneur is willing to offer a higher salary to tempt the employee to join, so the price of labour has just risen.

We are seeing data that suggests average hourly earnings are picking up. This implies that employees are finally seeing some above inflation pay rises, which has historically led to a pick-up in inflation.

What role does oil play?

Oil offers another area where price rises might be observed. Prior to the financial crisis, the price of a barrel of oil topped $140 but then spent seven years declining to a low of $26 in February 2016.

Oil is an important commodity as it is an essential part of most people’s lives, helping to transport them but also generating electricity and heat. It is not something that can be avoided as the alternatives, such as wind and solar, are expensive.

For more Schroders content visit our website and follow us on twitter

When the price of oil is falling it keeps inflation low, but we would argue the lowest price has now been achieved. Since February 2016 oil has been contributing to inflation.

How have inflation expectations affected your investments?

Our portfolios have already begun to benefit from an emerging trend of higher-than-expected inflation.

We have invested in areas that typically benefit from a generalised rise in prices, such as commodities, financials and cyclical companies – those that are more profitable as the economy picks up.

We have also moved away from the areas that have benefited from low inflation such as bonds, property and “non-cyclicals” – companies that deliver low but consistent growth irrespective of the economy. In the UK, these have included consumer staple stocks, such as Unilever.

Instead we believe it could be time for “value” parts of the market, undervalued stocks, to perform well. [Read more about value investing on The Value Perspective.]

We put more of the portfolio into gold over the course of this year, which has worked well. Gold has recently undergone a period of consolidation after delivering tremendous returns over the first half of this year. As an asset that typically does well when inflation is on the rise, it remains an important part of our portfolios.

What about the Trump effect?

And of course now, we also have the possibility of a Trumpflation effect.

The exact policies to be enacted by the next president of the US are unknown. If the new administration follows through on promises for tighter immigration, it will introduce new wage pressures.

If new trade tariffs are introduced, it effectively creates price rises in both the US and abroad by adding to the cost of goods. If Trump launches a huge programme of infrastructure improvements, as indicated in his victory speech, then this also could also feed in to higher inflation.

“Lower for longer” may have been correct for seven years, but are we moving towards “a bit higher, a bit sooner”? If so, the portfolio of the last seven years will need to change, something we have already done.

Further reading

Important Information: The views and opinions contained herein are those of Marcus Brookes, Head of Multi-manager at Schroders, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.