Bitcoin marks a significant step forward in trust for all of us

by Michael Haynes and Jason Carpenter of Etherbridge

“Bitcoin has no fundamental value” has long been the war cry for many traditional financial participants. This week we thought we could shed some light on this short-sighted mantra.

To highlight the clear value that Bitcoin affords, we first need to define what it is we are talking about.

So, what is Bitcoin?

Bitcoin is both a network and an asset. The Bitcoin network is a real-time gross settlement system comparable to Fedwire and Target. Settlement systems are the base layer of any financial system, and they leverage net settlement systems built on top to scale and provide utility to the day-to-day user.

The Bitcoin network requires participants called miners to contribute resources in order to process, execute and settle transactions. The process of performing these actions is costly, and miners are rewarded with bitcoin, the asset, for their participation.

Bitcoin, the asset, is a commodity on the Bitcoin network, it can be sent across the world, and you require it to pay the network’s fees. It is fungible, divisible, durable, portable, verifiable, scarce and has the additional properties of being censorship and seizure resistant.

Bitcoin also provides the user with high levels of certainty over its future dilution. Unlike fiat money, the issuance of bitcoin is codified and enforced by changes in the difficulty adjustment. This codified approach means bitcoins supply is impervious to changes in its demand.

Market Selected Forms of Money vs Fiat

No one reading this article has witnessed the rise of a market selected form of money; the money we use today is imposed on us and enforced by governments. A leader snapped his fingers and decided – “let it be done” (fiat’s direct translation) – that this paper we issue is now money and has value, backed by the promise of our government. It automatically served the role of being a medium of exchange, store of value and unit of account within that economy.

Market selected forms of money are different. They experience an evolution that challenges people’s perceptions of the money/asset. Historically, market selected forms of money have been commodities.

Gold is our best example. It initially started as a collectible, became a store of wealth, then widely adopted enough to be a medium of exchange and eventually became the very thing (or unit) we price everything in.

Bitcoin in its early days was merely a collectible that miners earnt for providing work to the Bitcoin network. The reason people wanted this collectible in its early days is different from why they demand it today. Initially, people would mine it or acquire it due to its perceived rarity and uniqueness; some, however, had incredible foresight and realised it may serve the role of money in the distant future.

The reasons people want it now are very different. Demand for Bitcoin today is driven by a market need for a non-discretionary, apolitical form of money. The price of Bitcoin is merely a lagging indicator of changing assumptions around money’s role in society. Market participants and institutions are buying bitcoin because it is superior to alternative monetary assets.

Even though market participants choose to store their wealth in Bitcoin, it doesn’t mean that Bitcoin is currently a safe or store of value asset. People are just voting (with their money) that Bitcoin will continue to succeed if demand for a non-discretionary apolitical monetary system continues to grow.

Will this demand continue?

The great financial crisis was a turning point for fiat money. This event — driven by the actions of irresponsible institutions caused an earthquake in financial markets. More importantly, the event caused interest rates all over the developed world to hit a zero bound.

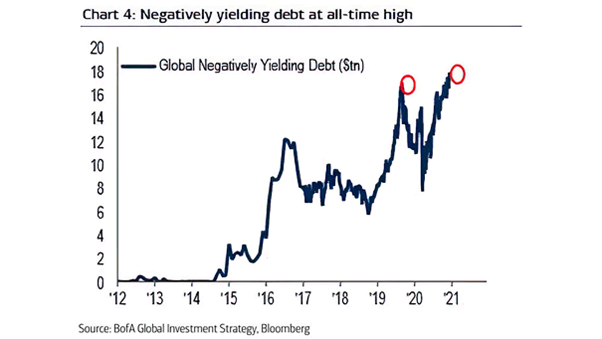

When interest rates hit zero, monetary policy loses its effectiveness and even worse, the cost of money becomes zero. We have seen interest rates continue lower, and in some countries, even go negative. This transforms what is meant to be an asset for the buyer of a bond into a liability. The bond market is breaking in front of our eyes.

Total negative yielding debt is $18 trillion and growing. According to Bloomberg this means that 27% of the world’s investment grade debt is now sub-zero. Governments simply can’t afford to let rates go up.

Add quantitative easing to the mix, and the storm becomes that much harder to weather. Not only are bonds becoming liabilities, but governments are rapidly debasing the value of their currencies.

All these countries clearly believe that they can extend their debt obligations further than their productive capabilities with no repercussions. There is no historical reference for this working over the long run, not one. This is what the Romans, Dutch and English did toward the end of their own empires. But don’t worry, Jerome Powell and Janet Yellen say that this time is different.

This irresponsible discretionary monetary policy has caused the political normalisation of concepts such as Modern Monetary Theory (MMT). It’s basically the idea that governments cannot default on their obligations because they are the sole issuer of their money. And through experiments like floating taxation rates, we can curb the inflationary pressures of printing and giving away money without increasing our productive capacities.

Were all of those who came before our current Federal incumbents just too stupid to engineer a financial system where no one needs to go bankrupt, and everyone could be given money in return for no productive contribution to society?

Money is stored time. Stored time is energy, and energy can’t just be created or destroyed; it must be transferred. Policymakers and central bankers are now engaged in an experiment of transferring wealth or otherwise abusing their citizens’ property rights.

This doesn’t mean that fiat needs to fail for bitcoin to succeed. However, Bitcoin introduces a discipline check on our current form of money. If governments continue down this path, they build the case for Bitcoin. They can force me to pay for my obligations and taxes in my local fiat currency, but they cannot force me to value that money.

Policy decisions, MMT, universal basic income, yield curve control are all drivers for the demand of a non-discretionary apolitical form of money. Bitcoin’s biggest threat is a return to sound monetary decisions by central banks.

Is Bitcoin growing?

Apparently, the Bitcoin network has no fundamentals, and there is no way to assess whether it is functioning correctly, being adopted or used. These are the uninformed comments; they are blatant lies used as an excuse for not doing one’s homework.

Being an open-source network with a transparent and auditable ledger has its perks. It allows participants to assess, in real-time, the state of the Bitcoin network. It’s so transparent that I can follow each and every coin from its genesis to where it sits today. I can map coins based on how long they have been in a specific wallet and identify and monitor accounts with large balances. The transparency is genuinely refreshing.

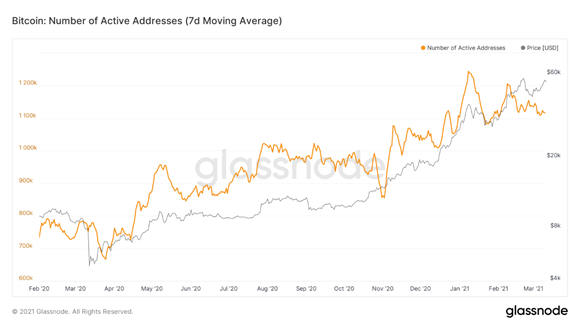

Metric 1: Are the Number of Users of the Bitcoin Network Increasing?

The key to bitcoins adoption is the growth of its user base. This speaks to bitcoin’s network effect, for every additional user that joins the utility of the network expands.

A year ago, there were more than 700,000 daily active users of the Bitcoin network. This has grown by 52% over the course of a year to just over 1.1 million daily active users.

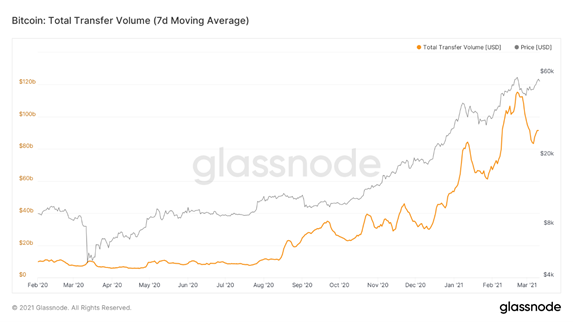

Metric 2: Is the volume transacted on the Bitcoin network increasing?

Bitcoin the network is a real-time gross settlement system comparable to that of Fedwire. A year ago, the Bitcoin network’s average daily transfer volume was just under $10 billion. This has skyrocketed to over $90 billion in transfer volume per day over the course of the past year. An 800% increase in total value settled on Bitcoin per day.

Over the last five years, the Bitcoin network has settled more than $22 trillion in transfers – an amazing feat for a 12-year-old software and no central coordinating entity.

Metric 3: Are miners making or losing money?

Miners are integral to the Bitcoin network as they process, execute, and settle transactions. For providing this work to the Bitcoin network, they are paid in Bitcoin. This reward is split into a block subsidy (inflation) and transaction fees.

A year ago, total miner revenue per day was $17 million and has grown to a staggering $51 million per day. Growing by 200% over the last year.

Metric 4: Bitcoin is an open network. Are companies investing in growing the network?

Bitcoin’s open network means anyone can invest in making it better. We have seen this happening rapidly, both at a code level as well as in infrastructure that will significantly increase the utility of the network.

At the helm, we have seen Jack Dorsey. Through his company Square, he launched a Bitcoin developer grant, open to anyone worldwide who intends to work on the Lightning Network and Bitcoin Core.

These grants are valued at around $ 100,000 each. We also saw Jack team up with Jay-Z to start a development fund that will offer grants to a total value of 500 BTC initially to developers in Africa and India. The only rule is that it has to improve the network and cannot be profit-motivated. Other companies that are actively funding the development of bitcoin include Blockstream, Lightning Labs, MIT, Chaincode, DG Lab, Acinq, Bitfinex and several more.

We have also seen companies building on the network, allowing it to scale and provide greater utility to the end-user. One of the most notable entering the space recently was PayPal.

In October last year, they announced that they would provide their 300 million clients with the ability to buy, hold and sell crypto. They could also then use this crypto to pay any one of their 26 million merchant partners (PayPal will convert the crypto before it lands in the merchant’s account).

We have also seen companies like BitPay partner with AT&T, BMW, Amazon, Microsoft, Google, Twitch, Adidas, Yum! Brands and many others to facilitate bitcoin payments and the purchase of gift cards. Coinbase, a company listing on the NYSE and currently valued at around $100 billion, supports payments plugins for e-commerce giants like Shopify and WooCommerce.

Or you have companies like Flexa, which have partnered with more than 41,336 locations in the US, including The Home Depot and Whole Food Markets. All these make the day-to-day use and, therefore, adoption of Bitcoin as a medium of exchange that much easier.

Companies are rapidly increasing their investments into cryptoasset infrastructure and benefitting the industry as a whole.

Metric 5: Proponents of Bitcoin claim it is a store of value. Is the market storing value in Bitcoin?

The last year has represented a seismic shift in how investor’s view bitcoin. We have seen public companies like Tesla, Microstrategy and Square building Bitcoin into their treasury reserve policies.

Investors such as Stanley Druckenmiller, Paul Tudor Jones, Cathie Wood and Bill Miller have been adding Bitcoin to client portfolios.

Even insurance companies like 169-year-old MassMutual have invested $100 million in Bitcoin in an effort to protect themselves and their clients from the actions of central banks around the world.

Banks have also joined the party; whether it be starting a trading desk or offering Bitcoin custody, they seem eager to get in on the action. JP Morgan has announced a Bitcoin exposure basket of companies who participate in the Bitcoin network. Clearly, they are past the “bitcoin is a fraud” argument.

At Etherbridge, we monitor HODL waves to understand the savings behaviour of the Bitcoin community. Currently, over 55% of Bitcoin’s total supply hasn’t moved in more than a year, and 45% haven’t moved in more than two years.

Even with the high price volatility we have experienced over the last year, people are still willing to hold onto their Bitcoin as if it’s a savings account. This really speaks to the Bitcoin community’s conviction and shows that people and institutions are choosing to store their wealth in bitcoin.

Metric 6: Is Bitcoin working as it was programmed to?

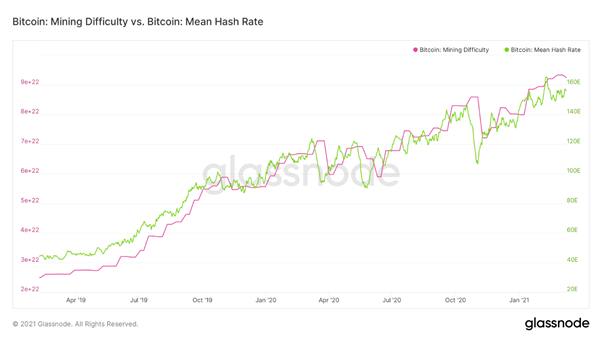

The real innovation behind Bitcoin comes from the difficulty adjustment. Unlike other market selected forms of money, Bitcoin’s supply is impervious to changes in demand. Every other commodity that could serve a role as sound money doesn’t possess this feature. If the demand for gold increased dramatically, every gold miner would be incentivised to increase their production and dilute existing holders.

Bitcoin’s issuance, however, is secured by the difficulty adjustment. The Bitcoin network is programmed to ensure that a new block is added to the chain of blocks every ten minutes on average.

If there is too much computational power and blocks are being added too quickly – every eight minutes, for example – that means Bitcoin is inflating faster than its predetermined codified issuance schedule.

The difficulty adjustment, which happens programmatically every two weeks, aims to bring block times back to 10 minutes by increasing the difficulty of the problem miners are to solve.

Look how the difficulty adjustment has tracked changes in computational power (hash rate). Bitcoin has replaced the Feds mandate of stable inflation with a couple lines of code.

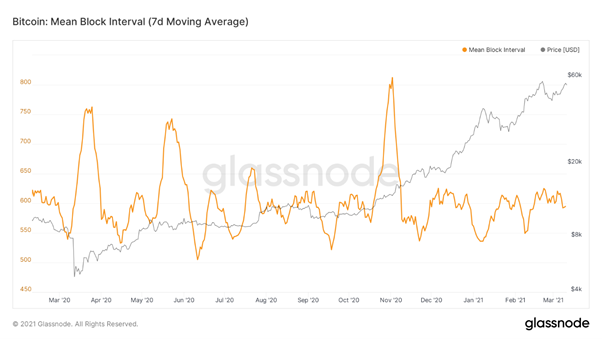

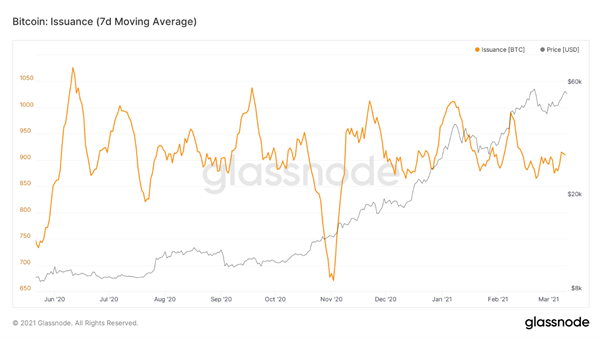

Metric 7: Has Bitcoin deviated from its predetermined codified issuance schedule?

Building on the difficulty adjustment, we can examine block times to see if the difficulty adjustment has been doing its job.

As you can see, block times fluctuate around an average of ten minutes each (600 seconds). Additionally, we can look at the issuance of Bitcoin. Currently, miners are competing to earn their share of 900 Bitcoin a day, 6,25 Bitcoin per block for 144 blocks a day.

Similar to how block times fluctuate around an average of 10 mins, you can see how issuance fluctuates around 900 Bitcoin per day. This is clear evidence that the Bitcoin network is working as it was programmed to do.

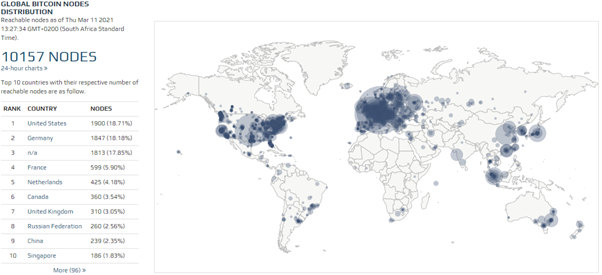

Metric 8: How many nodes does the Bitcoin network have?

Currently, more than 10 000 computers are running a full Bitcoin node. This means that there are 10,000 computers spread across the globe, keeping a record of and updating the Bitcoin Ledger in real-time.

No one country will be the sole owner of the ledger. Even if the whole Northern Hemisphere experienced an extended power outage, they could switch on their computers and start downloading the ledger from all their peers in the Southern Hemisphere once they got power again. This significantly contributes to Bitcoin’s resilience and censorship resistance. As long as there are people running Bitcoin nodes, the network cannot be stopped. Below is a map of the current countries running full Bitcoin nodes:

In reality, Bitcoin has fundamentals. We can monitor the network’s overall health by assessing miner revenues, block times, issuance rate, number of nodes, hash rate, and difficulty. We can determine whether the Bitcoin network is growing by checking metrics such as daily active addresses, total addresses with more than 0,01 Bitcoin, transaction volume and transaction counts.

We can see the investments in infrastructure that companies are making to improve the utility that Bitcoin provides. All these factors contribute to a robust economy that will allow Bitcoin and the network to flourish as we go forward.

Historically, open networks have always won out over closed, centralised systems. Just how the advent of the printing press ushered in the golden age of science by making information freely available and double-entry bookkeeping created a system where trust and cooperation could be established between distrusting parties.

Bitcoin and its network will provide a platform for open innovation on a global scale and mark a significant step forward for our societies’ trust and information.

“Value is not intrinsic. It is not in things. It is within us; it is the way in which man reacts to the conditions of his environment. Neither is value in words and doctrines, it is reflected in human conduct. It is not what a man or groups of men say about value that counts, but how they act.”

Ludwig von Mises