The greater a market’s valuation, the smaller the likely future returns

The growing willingness for investors to pay higher and higher prices for stocks is a real cause for concern.

For instance, US index, the S&P 500, has only ever been more expensive on two previous occasions – just before the dotcom bubble burst in 2000 and in the build-up to the Great Crash of 1929 – but does that mean markets are due a fall?

However, a far more important consideration than the absolute level of a stock market is its underlying valuation.

That is why one of our favourite metrics is the cyclically adjusted price/earnings ratio. Known for short as the ‘CAPE’, this encapsulates the average earnings generated by a market over the last 10 years, adjusted for inflation.

- Be prudent and give yourself a margin of investment safety

- How to value stock markets: five key tests

Over time, like so much else in investment – and indeed in life – any CAPE will tend to head back towards its longer-term average.

Looking at the S&P 500’s elevated headline figure of a little over 31x today, therefore, some would conclude this ‘mean reversion’ implies an imminent correction to asset prices – and, of course, this remains a very real possibility.

Historically, though, a significant amount of a CAPE's mean reversion comes from earnings catching up with stock prices, rather than the other way around.

With global profit margins nudging all-time highs we may question the likelihood of this. But what we can say with confidence is that with valuations so much higher than average returns are likely to be lower than the long-term average over meaningful time periods.

US is no longer cheap

Moving closer to home, it is fair to say that, while in aggregate the UK market is not as expensive as the US, it is no longer cheap.

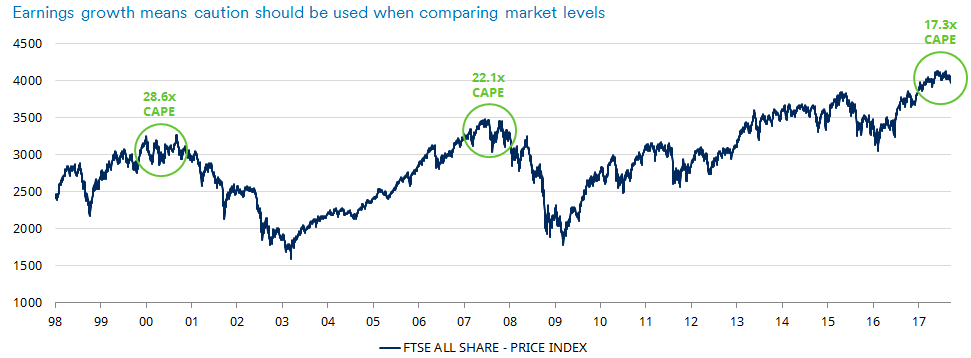

The following chart shows the FTSE All-Share price index from 1998 to today with the CAPE’s of the market peaks marked in green.

Almost two decades of earnings growth do mean that, despite today’s index level being higher, valuations are not as overextended as they were in 2000 or 2007.

At those two earlier peaks, the FTSE All-Share traded on a CAPE of 28.6x and 22.1x respectively whereas, despite the higher index level, its CAPE today is closer to 17x.

That is still well above the long-term average of 11.4x – UK stockmarket data goes back to 1927 – and history suggests that, from today’s valuation level, the wider UK market will deliver inflation plus 3 per cent to 4 per cent a year for equity investors over the next decade.

And while history of course makes no promises about the future, it is worth noting that that growth rate compares with inflation plus 7 per cent or 8 per cent a year over the very long term.

Equally, it is important to bear in mind any market valuation is simply an average of the value of the individual stocks within it and, among those individual stocks, there remain some attractive opportunities for value-oriented stock-picking investors.

The effect these opportunities have on us

It is these opportunities that give us confidence in our ability to continue to extract the 2 per cent or so premium return offered to value investors over and above the market itself, through focusing on the cheapest parts of the market.

Relative to some competitors, who are increasingly overly exposed to expensive companies, we believe the outperformance from our own portfolios should be significant.

- Why ‘winter is coming’ for overvalued growth stocks

- More value investing ideas: @thevalueteam

The dislocation between the current market trajectory and the whole of the rest of history has become extreme and so, when it comes, the market’s eventual snap-back to its typical function as an arbitrator of value will be profound.

At that point value investors will be grateful for the margin of safety that is part and parcel of the discipline.

- Andrew Williams is an author on The Value Perspective, a blog about value investing. It is a long-term investing approach which focuses on exploiting swings in stock market sentiment, targeting companies which are valued at less than their true worth and waiting for a correction.

Important Information: The views and opinions contained herein are those of Andrew Williams, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.