Mark Carney’s first year: Bank governor enjoys roaring recovery – but he can’t take credit

Mark Carney has had a spectacularly good first 365 days at Threadneedle Street.

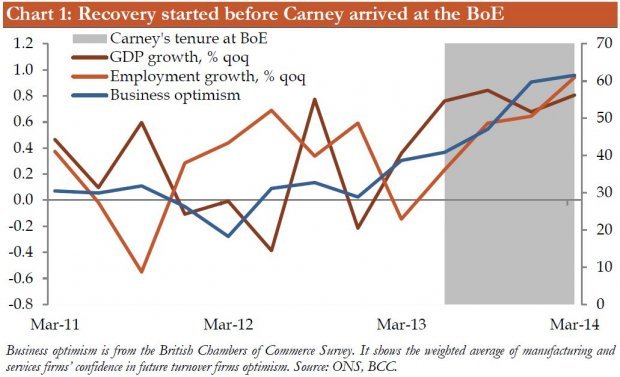

Since he's arrived at the Bank of England the UK economy has busted analyst growth expectations.

Unemployment has fallen faster than almost anyone had predicted, and inflation is now back below the Bank's two per cent target.

Judged by cold hard results, Berenberg's chief UK economist, Rob Wood, says that Carney's first year "has been a roaring success". The strength of the economy is "a big change from the previous few years".

His predecessor, former governor Sir Mervyn King, couldn't be blamed for feeling a little bit jealous. While Carney may take much of the glory, he probably didn't have much to do with it. Wood says that monetary policy instruments such as interest rates have a lag of around a year, so only now could Carney be expected to affect output. In fact, as far as Berenberg is concerned, "the recovery has nothing to do with any action he [Carney] has taken".

(Source: Berenberg)

But while monetary policy announcements have long and variable lags, it can also have long and variable leads. Is it possible that markets, being aware of Carney's arrival, assumed that he would steer the Bank in a more dovish direction, and investors adapted their expectations accordingly?

Carney's appointment was announced on 26 November 2012 by chancellor George Osborne. The Canadian had previously ruled himself out of the running, so the news was a surprise. If investors were overwhelmingly positive, we'd expect to see stocks appreciate as a result.

So what happened? Ben Southwood, head of policy at the Adam Smith Institute, says that the FTSE 350 barely rose that day, nor when he came into office last year, or even when Carney introduced forward guidance in August.

And since Carney's arrival was announced the pound has strengthened against the dollar, while inflation has declined. Taken together these three facts imply that Bank policy "has been a relatively small factor in the nascent recovery," says Southwood, "just as inflation spikes were out of the Bank's hands in 2011, real GDP improvements are also likely coming from supply-side improvements now".

Southwood highlights Japan as a comparison. There Bank of Japan governor Haruhiko Kuroda and Prime Minister Shinzo Abe "really have made the difference" through monetary policy. Stocks are way up, the yen is way down, and inflation has risen.

Wood says that the real catalyst for the UK's economic revival was another central banker: the European Central Bank president Mario Draghi. His commitment in July 2012 "to do whatever it takes" to keep the Eurozone together likely did the work that some now credit Carney for.

Berenberg cites a recent Bank paper on the impact of world and domestic factors on growth. Bank staffers found that much of the turnaround was due to an easing drag from the rest of the world, which Draghi's comments helped to achieve.

(Source: Berenberg)