Oil prices rally to seven year highs amid rising fears Russia will invade Ukraine

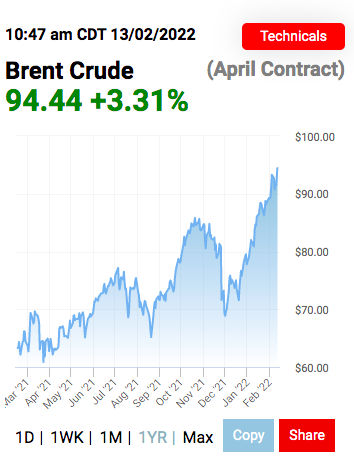

Oil prices rallied on Friday to fresh seven-year highs, with both benchmarks revived by escalating fears of a Russian invasion of Ukraine.

Brent Crude prices settled at $94.44 per barrel – a 3.3 per cent hike in half a day – while WTI Crude rose 3.6 per cent to $93.10.

Both benchmarks passed Monday’s peaks, and have now recorded eighth consecutive week of gains.

Trading volumes spiked in the last hour of trading, with volumes for global benchmark Brent climbing to their highest in more than two months.

Conflict in Ukraine could see severe disruption to both oil supplies and supply chains as a consequence of potential Western sanctions and disruption.

Russia has massed over 100,000 troops near Ukraine over the past two months, and Washington has now warned an attack on Kyiv could be imminent.

The US, UK, Australia and New Zealand have all advised their citizens to leave Ukraine.

Prime Minister Boris Johnson has said NATO allies need to make it absolutely clear that there will be a heavy package of economic sanctions ready to go, should Russia invade Ukraine.

The latest developments will renew speculation that oil prices will pass the $100 milestone during this quarter.

Edward Moya, senior market analyst at OANDA said: “Crude prices surged after reports that the US is expecting the Russians to move forward with invading Ukraine. This was not expected considering some constructive comments during the week. If PBS reporting is correct and troop movement happens, Brent crude won’t have any trouble rallying above the $100 level.”

Alongside fears of reduced supplies from Ukraine-Russia tensions, OPEC+ has failed to hit raised output targets amid rebounding demand from the coronavirus pandemic.

(Source: OilPrice.com)

OPEC has recently outlined that demand will rise more steeply than initially anticipated, while the International Energy Agency raised its 2022 demand forecast and expects global demand to expand by 3.2m barrels per day (bpd) this year: an all-time record 100.6m bpd.

The IEA added that Saudi Arabia and the United Arab Emirates could help to calm volatile oil markets if they pumped more crude, adding that the OPEC+ alliance produced 900,000 bpd below target in January.

The Biden administration has responded to high prices with confirmation it has been holding more talks large producers about increasing output, as well as the possibility of additional strategic releases from large consumers.

With the mid-terms coming up in November, and threadbare majorities in the Senate and House of Representatives, reducing cost-of-living pressures from US citizens is increasingly important for Biden.

Meanwhile, indirect talks between US and Iran nuclear talks also resumed this week after a 10-day break.

A deal could see the lifting of sanctions on Iranian oil and ease supply tightness.