Carbon credits and the reshaping power of blockchain

Blockchain technology is being used to help create a more transparent and efficient carbon credits market. The demand for carbon credits has grown significantly with the increasing focus on mitigating climate change and reducing carbon emissions.

However, the existing carbon credits market is fragmented and lacks perspicuity, making it difficult for buyers and sellers to navigate. Can blockchain technology be used to create a more transparent and efficient carbon credits market?

Also known as carbon offsets, carbon credits permit the owner to emit an equivalent amount of tons of carbon dioxide or other greenhouse gases.

According to Coherent Market Insights, the global carbon credit market is expected to reach US$ 2,407.8 billion by 2027, a CAGR of 30.7% between 2020 and 2027.

The last time the world saw a significant decrease in carbon emissions was during the Covid-19 pandemic global lockdown. Emissions in 2021 increased to 36.3 gigatonnes. Global energy-related carbon dioxide emissions rose 6% in 2021 to 36.3 billion tons, their highest-ever level, and to combat this the UN has created carbon credits as a temporary measure until the end of 2023.

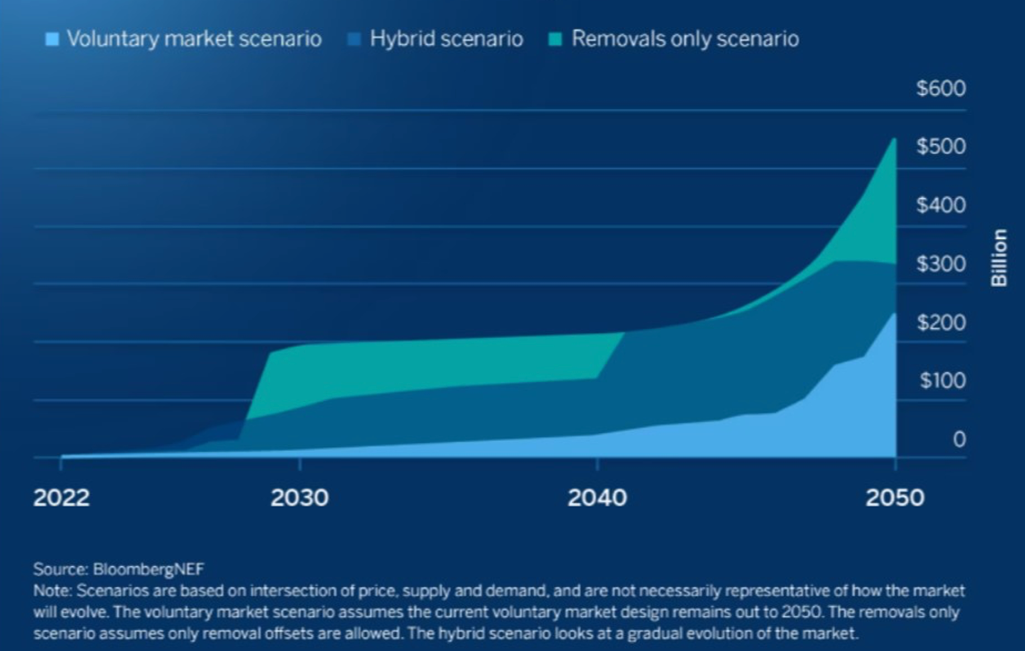

The value of the carbon offset market projected to exceed $500billion by 2050

Source: Bloomberg

Two carbon credits markets exist: voluntary and compliance – the latter being enforced by world governments.

The value of the global carbon credit market reached $850 billion in 2021 (a 164% increase from 2020) and the current top compliance market players are Europe, the US and China. Notably, risks and challenges in the compliance carbon credits market are mostly tied to policy change and error and geopolitical tension; interestingly, the voluntary carbon market reached $2 billion in 2021, having already quadrupled its size in 2020.

However, trust is an issue with the voluntary carbon market, given a general lack of transparency in MRV (measurement, reporting and verification), potency for fraud and low-quality carbon offset credits. Considering blockchain-powered platforms provide greater transparency, and therefore trust, it is hardly surprising that blockchains are being used more and more in this market.

UK-blockchain carbon offset platform, Carbonplace, has raised $45M and uses distributed ledger technology (DLT) to provide a settlement network for carbon credits, so ensuring the simultaneous transfer of ownership of credits and payment.

Furthermore, by turning credits into tokens, the World Bank’s International Finance Corporation (IFC) division is looking to create a fund and so encourage more capital to trade carbon credits. Subsequently, as the carbon credits are turned into digital assets on the Chai blockchain, they will be tracked by the

World Bank’s ‘Climate Warehouse’.

Nevertheless, whilst there are many other players in the industry, blockchain adoption (as a solution to different carbon credits problems) has limitations.

Blockchains are little more than Excel spreadsheets on steroids – holding and enabling data to be shared cryptographically.

Blockchains cannot ascertain how true the emission reductions that come with carbon credits are. They are also unable to verify the claims of credit sellers as regards the longevity of credits, although a firm that is looking to tackle such challenges is Sunified, as it records the creation of energy every 30 seconds.

Thus, offering proof that the electrons were generated via solar or wind turbines. Sunified’s blockchain-powered platform also keeps a record of the time and location of when and where the power was created. Another example is a company called Wis@key, which is using NFTs to record the planting of trees, creating a token for each tree planted (geolocated and monitored using satellites) – such information being vital when it comes to having the ability to receive carbon credits.

In Australia, a firm called TYMLEZ offers organisations a step-by-step breakdown of the creation of a tokenised carbon credit using its blockchain-powered platform.

However, there is the opportunity of zombie projects finding their way to blockchains. This comes with the migration of carbon offset registries using blockchains.

One of the largest registries of conventional carbon credits is held by an organisation called Verra and it has allowed the transfer of carbon credits onto a blockchain via the Toucan protocol, creating Base Carbon Tokens (BCTs). Unfortunately, as CarbonPlan.org explains, two problems have been identified:

“…a suite of what we call ‘zombie’ projects that were inactive until the economic incentive to generate BCTs came along, a striking finding that nearly all bridged credits come from projects that have been excluded from major segments of the conventional offset market due to quality concerns.”

The worry is, is that there are a number of projects unable to attract buyers in the voluntary carbon marketplace due to their questionable claims as to whether they do, indeed, have any positive impact on reducing carbon. Once these projects convert into BTCs, there is a market which places doubt as to whether BTCs do actually have the same beneficial impact to help reduce the impact of carbon emissions. So, once again, the thorny issue of trust is raised.

Resultant from this is that some feel the creation of digital carbon credits using blockchains has caused more harm than good because some carbon credits represent emissions reductions that are questionable at best. However, many of these problems could have been avoided if more in-depth due diligence had been carried out on projects that have been allowed to use the Toucon protocol.

Yet the concerns around BTCs which use blockchain technology has not prevented every organisation from embracing blockchain carbon solutions. Indonesia incentivised blockchain- fuelled carbon trading by signing an agreement with Singaporean digital exchange start-up, Metaverse Green Exchange. And another application can be seen in the partnership between WWF and BCG Digital Ventures which, out of many functions, “helps people and business to avoid illegal, environmentally-damaging or unethical goods.” Furthermore, McKinsey has estimated that “global demand for carbon credits could increase by a factor of 15 or more by 2030 and by a factor of up to 100 by 2050. Overall, the market for carbon credits could be worth upward of $50 billion in 2030.”

Meanwhile, the voluntary carbon credit is an important source of finance for projects designed to reduce carbon emissions and also helps those firms looking for ways to improve their ESG credentials and meet their climate change commitments.

Paul Brody, EY’s global blockchain leader believes: “In a blockchain-based ecosystem, you can have a very liquid, digital interaction, where you can pick from a dozen different vendors, and you can evaluate them all on a digital basis.”

Therefore, what is required are agreed worldwide standards as to which projects qualify to receive carbon credits based on their impact on reducing carbon emissions. In essence, the carbon credit market needs greater transparency in order to generate greater trust and confidence, and thus create an active market of buyers and sellers of carbon credits.

In theory at least, blockchain technology offers a promising solution but, regardless of what technology is used, the success of any new carbon credit trading platform/marketplace will undoubtedly be dependent on the quality of the data that is used.