Why investors should beware the latest fairytale story

Once upon a time there lived a little pixie, who went to see a wise old wizard to ask him a question (humour me and read on…).

“Why was the Fairyland stock market down today?” asked the pixie. “Because there were more sellers than buyers,” shrugged the wizard. “And if the market should rise tomorrow, it will be because there are more buyers than sellers.” “Oh,” said the pixie. “To be honest, I was hoping for a more exciting explanation.”

And that is just one reason why, on our Value Perspective blog, we leave writing bedtime stories to others.

Another thing we try and avoid with stories is introducing them into our day jobs as a way of imposing order or logic on a particular investment or market situation.

This very human instinct, which boils down to the idea that people do like a bit of a story, is known by behavioural scientists as ‘narrative fallacy’.

What is 'narrative fallacy'?

The snag with adding any kind of narrative gloss to an investment scenario is that this can cloud an objective analysis of the available facts.

As an example, highlighting one particular version of a future that can of course play out in any number of unpredictable ways introduces the risk that we become psychologically attached to our one pet view.

As with many potential pitfalls in the world of behavioural finance, the twist here is your brain is hardwired not to act in your best investment interests – in other words, investors make these mistakes instinctively.

In the case of narrative fallacy, this is strikingly illustrated by a series of experiments conducted through the second half of the 20th Century on so-called ‘split-brain’ patients.

Between the 1940s and the 1980s, neuroscientists developed a drastic treatment for people exhibiting certain neurological symptoms that involved severing the ‘corpus callosum’ – the bundle of neuronal fibres that links the left and right hemispheres of the brain.

While helping to control one of a patient’s symptoms, this surgical ‘firebreak’ also meant the left side of their brain quite literally no longer knew what the right side was doing – and vice versa.

This article from Nature journal covers the whole subject in a lot more detail. In short, the experiments mentioned above originated from tasks where US neuroscientist Michael Gazzaniga would ask a split-brain person to explain in words, which uses the left hemisphere of the brain, an action that had been directed to and carried out only by the right side.

Gazzaniga found that the left side of the brain would make up an off-the-cuff answer that fitted the situation.

In one experiment, for example, he flashed the word ‘smile’ to a patient’s right hemisphere and the word ‘face’ to the left hemisphere, and asked the patient to draw what he had seen.

When the patient drew a smiling face with his right hand, Gazzaniga asked why he had done so.

The patient replied: “'What do you want – a sad face? Who wants a sad face around?”

According to Gazzaniga, this left-brain interpretation is what everyone uses to seek explanations for events – as a way of imposing some sort of order on the constant stream of incoming information the world throws at us and constructing narratives that help make sense of it all.

The split-brain experiments may be an extreme illustration of narrative fallacy but, as human beings, investors risk falling into the trap every day.

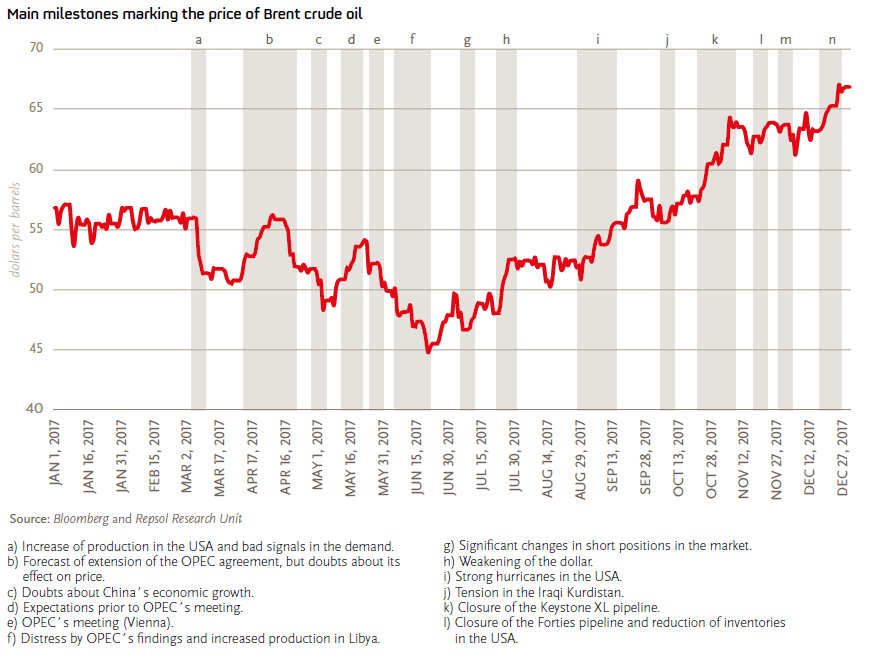

Take the following example, which comes from the most recent annual report of global energy company Repsol and shows the movements in the oil price over the course of 2017 – along with its research unit’s explanations for the dozen most significant ups and downs.

Past performance is not a guide to future performance and may not be repeated.

Such commitment to the idea every aspect of finance and markets needs to be accompanied by a story would probably have been more exciting for our little pixie but – as the wise old wizard said, and dull as it may be – the oil price really only moved because sometimes buyers outnumbered sellers and sometimes it was the other way round.

- Andrew Evans is an author on The Value Perspective, a blog about value investing. It is a long-term investing approach which focuses on exploiting swings in stock market sentiment, targeting companies which are valued at less than their true worth and waiting for a correction.

Important Information: The views and opinions contained herein are of those named in the article and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This communication is marketing material.

This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schrodersdoes not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.