Is inflation a bigger concern than bond markets?

Rising bond yields have been cited as the reason behind the sell-off in the equity markets but should investors be just as concerned about a spike in inflation?

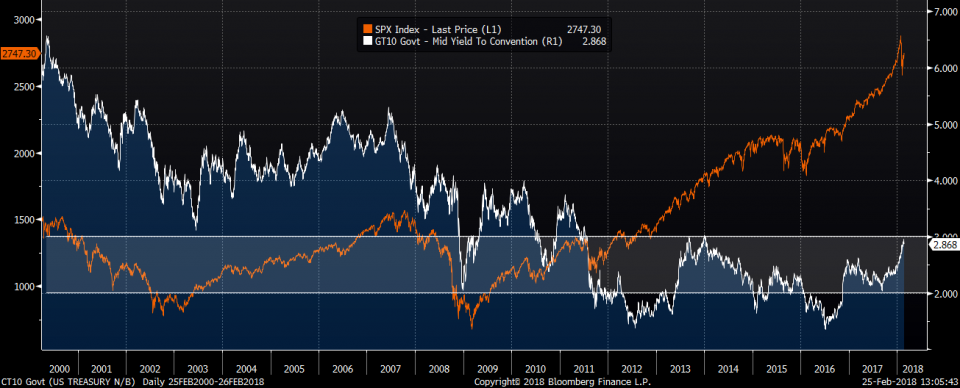

The 10-year US Treasury yield has been moving ever closer to 3 per cent, a level that could start to concern some equity market investors. While the whole of the US Treasury curve has been shifting upward, it is the 10-year rate that is most widely watched by investors as it is the benchmark for a whole range of business and consumer loans, including mortgages.

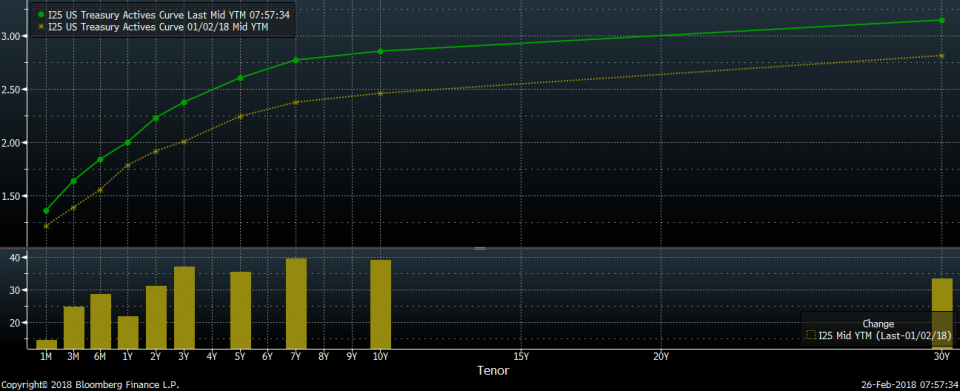

Almost parallel shift in the US Treasury yield curve since the beginning of the year:

Past performance is not a reliable indicator of future results

On 21st February the yield on the 10-year US Treasury closed at 2.951 per cent, a multi-year high and a level that saw a rally in the S&P turn into a rout, with the index ending the day around down. The 3 per cent level for the 10-year yield does not necessarily have to stop the bull run in the equity markets but it is a level where the probability for losses in the S&P starts to increase. A higher discount rate means lower valuations but this is not the only variable to consider. Correlations between bond yields and equity performance are not set in stone and there is no level for the 10-year yield that is necessarily ‘bad’ for the equity markets if growth rates are high. Some consider the 2-3 per cent level for the 10-year yield a ‘sweet spot’ for equity markets but strong US and global growth makes it more likely that this time around that equity markets can withstand a yield above the 3 per cent level.

It has been pointed out that equities had a record year in 2013 during what was described as the ‘taper tantrum’ in the bond markets on expectations of Fed policy tightening, whilst the 10-year yield jumped higher by around 1 per cent, the S&P had a total return of over 29 per cent that year. Rising rates could obviously impact upon corporate margins but this impact should be gradual since large-cap debt is mostly fixed rate and long-term.

It is likely that the 10-year will hit the 3 per cent level as the market sees some more positive macro data and further hawkish rhetoric out of the Fed. The Fed did not really tip its hand at its January meeting as to whether it would raise rates more than the three times forecast. However, comments in the minutes of the meeting were viewed as the committee being more confident about the upward path for interest rates. Following its meeting in March, the Fed will release new projections for the economy and outlne potential rate hikes. Equity markets should become used to the 10-year trading around the 3% level if the Fed sticks to its projections.

Rather than just watching bond yields, inflation expectations are probably just as important for the equity investor, if not more so. In the US the latest reading for headline CPI was 2.1 per cent annualised, and forward expectations have increased since the beginning of January from 2.27 per cent to 2.40 per cent (USD Inflation Swap Forward).

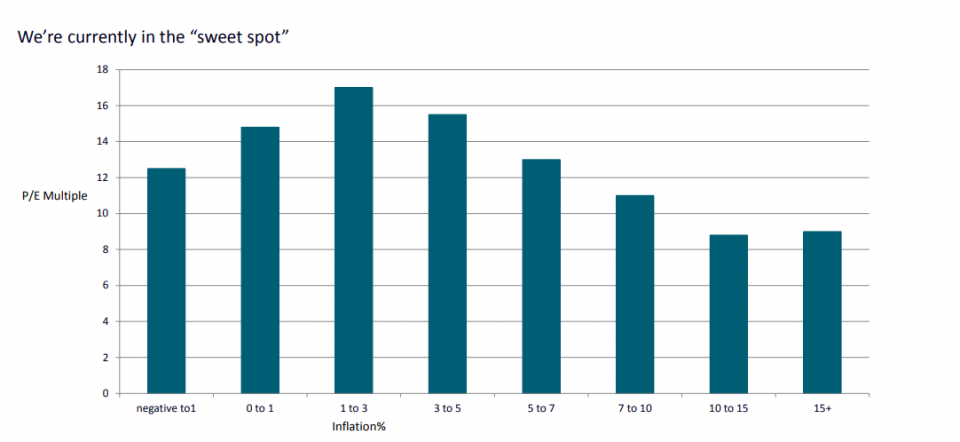

A large spike higher in inflation expectations could imply that the Fed is behind the curve in its tightening cycle, and this could lead to a concerted move higher in the Fed Funds rate. However, we are currently in the ‘sweet spot’ of 1-3 per cent inflation as can be see in the chart below that plots inflation versus P/E multiples.

So rather than viewing the rise in bond yields as a monetary policy mis-step or concerns over sovereign credit-risk, it should be viewed as reflecting central bank’s comfort with the global growth outlook. In the US this growth story has been given a further boost by the implementation of new corporate-friendly fiscal measures and financial market deregulation, which overall should be equity market positive. It can therefore be argued that equity investors should not really be concerned about a healthy rise in bond yields but be be more concerned about an unhealthy rise in inflation.

Nothing on this website should be construed as personal advice based on your circumstances. No news or research item is a personal recommendation to deal