14 years of investment returns: history’s lesson for investors

The stockmarket has provided the best returns among the major asset classes over the last 14 years. But the total profits belie wild fluctuations year by year.

Such volatility can cause problems for those who need to draw down money from their investments at certain points of their lives. A sudden drop in the stock market just before university fees are due or before retirement can derail best laid plans.

That is where diversification can help. Spreading your money around can potentially help reduce risk, smooth out those highs and lows, and may even improve the long-term performance of your overall portfolio.

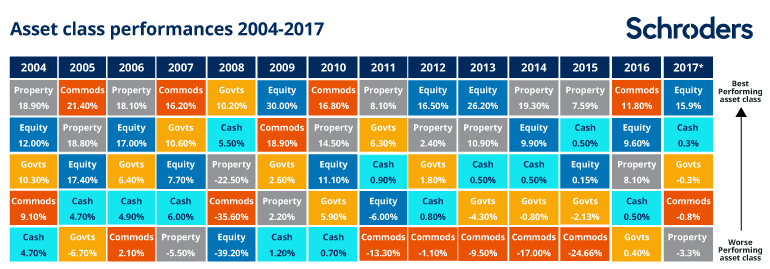

The table below shows the performance of some of the main asset classes in each year.

Of course it’s important to note that past performance is not a guide to future performance and may not be repeated.

Equities relates to world stock markets as measured by the MSCI AC World Total Return index. “Govts” relates to the performance of government bonds around the world and property relates to returns from UK commercial property. More detail on the indices used for each asset can be found at the foot of the table.

14 years of asset returns

Source: Schroders, Datastream as of 31 October 2017. Equity: MSCI AC World Total Return Index (local currencies); Property: UK IPD Index (sterling); Cash: 3 month Sterling LIBOR (sterling); Government bonds: Barclays Global Treasury Index (dollars); Commodities: Bloomberg Commodity index (dollars). All show total return either in local currency or currency of denomination. Please remember past performance is not a guide to future performance and may not be repeated.

It is possible to map events to some of the good and bad years for different assets. Perhaps the most iconic was the boom in the price of nearly every asset, particularly property, in the mid-Noughties. It famously ended in disaster in 2007 when the sub-prime mortgage crisis caused a global recession.

In the year that followed, UK commercial property lost 22.5 per cent while global stock markets registered a near 40 per cent loss. Portfolios that contained government bonds, which returned more than 10 per cent that year, will have seen losses somewhat offset.

- The global financial crisis 10 years on: six charts that tell the story

- Pound devaluation: how the lessons of 1967 apply today

The price of mainstream assets rallied after the global financial crisis. In part, it was a reaction to the extreme measures taken by central banks to boost economies. But even in this period, not all investments moved in the same direction.

Commodities, which had surged in value with shares and property before the crisis, languished in the first half of this decade.

- Take a quick investment test: investIQ

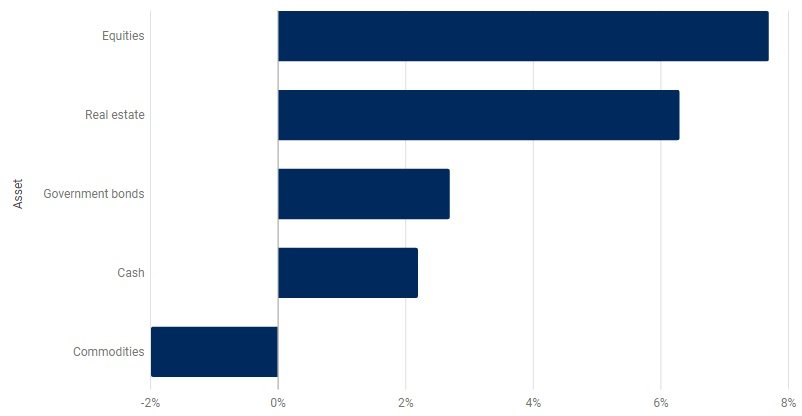

Equities returned the most, commodities the least

Over the whole period, it’s possible to calculate average returns from these assets. Equities returned an average of 7.7 per cent annually between 2004 and 2017, according to data compiled by Schroders.

The next best performer of the assets analysed was real estate, or commercial property, which returned an average of 6.3 per cent. It was followed by government bonds and cash.

Commodities have been the worst performing investment and the only one to produce a loss, of 2 per cent a year, during that period.

Annual asset returns since 2004

Source: Schroders, Datastream as of 31 October 2017. Equity: MSCI AC World Total Return Index (local currencies); Property: UK IPD Index (sterling); Cash: 3 month Sterling LIBOR (sterling); Government bonds: Barclays Global Treasury Index (dollars); Commodities: Bloomberg Commodity index (dollars).Please remember past performance is not a guide to future performance and may not be repeated.

In terms of total returns over the 14 years, the commercial property index rose 135 per cent. For sterling investors, £1,000 invested in 2004 would be worth £2,355 today (31 October, 2017).

It should be noted that some of the indices mentioned above are priced in various currencies. The actual returns would be determined by your local rate of exchange.

Currency movements can provide further diversification. By investing in assets overseas, it’s not just the performance of the asset that determines the return, but also the strength and weakness of the currencies of the investor and the location of the investments.

The benefits of diversification

Reducing risk: A crucial imperative for most investors is not to lose money. This is always a risk with investing, but diversifying may mitigate that risk.

Retaining access to the money you need: In times of stress the ease in which you can buy and sell an asset is critical. This varies between assets, known as liquidity. For instance, property can be more illiquid than equities. Diversification can help.

Smoothing the ups and downs: The frequency and extremity with which your investments rise and fall determines your portfolio’s volatility. Diversifying your investments can give a greater chance of smoothing out those peaks and troughs.

Too much diversification?

There is no fixed rule as to how many assets a diversified portfolio should hold: too few can add risk, but so can holding too many. Hundreds of holdings across many different assets can be hard to manage, and diversification for the sake of it runs the risk of poorer performance, sometimes called “diworsification”.

Important Information: The views and opinions contained herein are those of David Brett, Investment Writer, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.