How tobacco stocks could now be damaging to your wealth

A month has now passed since tobacco businesses – and their share prices – were sent reeling by a US regulatory announcement.

So what was the news that, for example, wiped out all the gains British American Tobacco had made in the first half of this year? Was it perhaps about to become illegal to smoke in US homes? Or was a prohibition-style ban on selling cigarettes maybe on the cards?

Well, if you remember, what actually caused tobacco companies and their investors such a fright was the revelation by the US Food and Drug Administration that it was planning to “begin a public dialogue” on the subject of lowering nicotine levels in cigarettes to non-addictive levels.

Not the end of the world, you might think – but markets are hardly renowned for their measured response to unexpected news.

Bad news can leave investors exposed

The thing is, as we have discussed in articles such as Calm before the storm, the ever-higher prices the wider market has been willing to pay for the perceived safety of many traditionally defensive assets – for example, food, beverage and, yes, tobacco stocks – means, when any bad news comes, it is taken very badly indeed.

When a stock is ‘priced for perfection’, in other words, its investors can find themselves very exposed.

That has not stopped a lot of equity income portfolios becoming overloaded with food, beverage, tobacco and other assets characterised as ‘bond proxies’ on account of the elevated dividends they pay – especially in the context of the current ultra-low interest rate environment.

On our Value Perspective blog, however, our unwavering focus on valuation means our own income portfolios are positioned very differently.

A good illustration of this is our preference for banks – a sector where many investors still fear to tread.

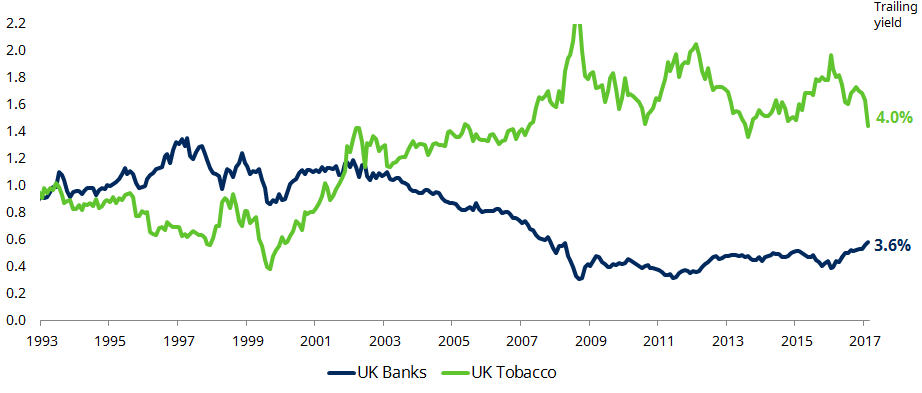

And yet consider the following chart, which compares the valuations of UK banking and tobacco stocks – more specifically, their cyclically-adjusted price/earnings or ‘CAPE’ ratios (which encapsulate a sector’s average earnings over the last 10 years, adjusted for inflation) relative to the wider UK market.

UK Banks vs UK Tobacco Stocks Valuation. CAPE Premium/(Discount) to Market.

Source: Schroders, Thomson Datastream, as at 31 July 2017.

As you can see, UK tobacco stocks are trading on a significant premium to the wider market – and, even after last month’s fall, are towards the upper end of their historic valuation range.

For their part, UK banks are trading at a significant discount to the wider market – and yet, as a sector, are paying an average 3.6% dividend, which is near the 4% average on offer from tobacco stocks.

Back in 2011, a Value Perspective piece called Smoke and mirrors drew comparisons between the then out-of-favour pharmaceuticals sector and the deeply unloved tobacco industry of the 1990s.

We argued investors were, in each instance, so concerned by the sectors’ respective negatives they had become blind to how they in fact boasted well-run businesses with attractive dynamics and sensible amounts of debt.

In the six years since that piece was written, pharmaceuticals have done so well the comparison is no longer appropriate – though we would argue investors could benefit from thinking about banks in a similar light.

Over that time, tobacco stocks have also thrived – to the point, as we mentioned above, that even a fairly mundane regulatory pronouncement on nicotine levels can lead to a 10% slide in share prices.

Focusing on yield leaves no margin for error

The suspicion must be that any number of pieces of negative news – for example, something relating to the emerging markets, where the hopes for so much of the sector’s profits now rest – could have had a similar effect on tobacco share prices.

Indeed, they still could – and yet when investors focus on yield to the exclusion of considerations such as valuation or total return, they leave themselves no margin for error.

It is a point we made this time last year, in Dia, oh Dia, when we argued: “Investors’ thinking appears to be being muddled by ultra-low interest rates and now it is almost as if they have convinced themselves they can buy consumer staples stocks no matter their cost.

"But they cannot – and the reality is many are buying these stocks not for their underlying quality but for the simple reason they are going up in price.

“In essence, they are not buying what they think they are buying – high-quality businesses with stable earnings – but very sensitive and increasingly expensive assets.”

- Andrew Williams is an author on The Value Perspective, a blog about value investing. It is a long-term investing approach which focuses on exploiting swings in stock market sentiment, targeting companies which are valued at less than their true worth and waiting for a correction.

Important Information: The views and opinions contained herein are those of Andrew Williams, investment specialist, equity value, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.